Why are FIIs making bold bets on India’s smaller banks and NBFCs?

Foreign Institutional Investors (FIIs) are making significant strategic bets on India's smaller banks and NBFCs, signaling strong long-term conviction in the sector's structural growth.

Key Takeaways

- Over ₹1.25 lakh crore in foreign capital flowed into India’s financial services sector in 2025, primarily targeting NBFCs and mid-sized banks.

- Key drivers include favorable regulatory easing from RBI, attractive valuations (many trade below 2x P/B), improved lending flexibility, and robust balance sheet leverage headroom.

- This strategic capital infusion is poised to transform profitability, scalability, and governance for these institutions, offering global investors significant growth potential and operational expertise.

India’s financial sector is undergoing a structural shift. Over ₹1.25 lakh crore in foreign capital, a step jump from previous years, has flowed into India’s financial services sector in 2025. This strategic foreign capital, largely directed toward NBFCs and mid-sized banks, signals strong long-term conviction in the sector. These aren’t just cyclical trading bets but strategic investments aimed at capturing India’s next phase of credit growth. Backed by stronger balance sheets, and regulatory easing of capital flows and improving governance, foreign institutions are viewing India’s credit story not as a trade, but as a transformation.

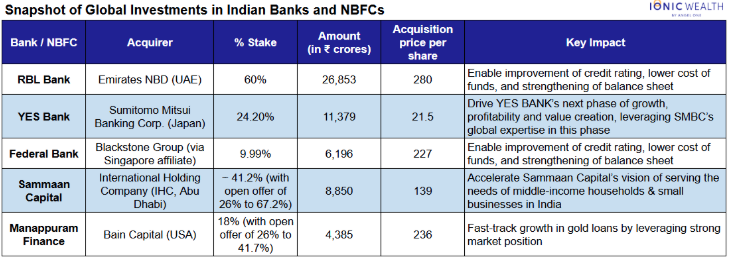

In a series of landmark moves, foreign investors have made significant bets on India’s financial services sector:

- Dubai-based Emirates NBD announced a ₹26,853 crore acquisition for a 60% stake in RBL Bank, marking one of the largest foreign takeovers in the sector.

- Japan’s SMBC invested over ₹11,379 crore to acquire approximately 25% in YES Bank.

- Abu Dhabi’s International Holding Company (IHC) committed nearly ₹8,850 crore to acquire a controlling stake in Sammaan Capital, signalling confidence in the NBFC revival story.

- Blackstone Inc. took a 9.99% stake in Federal Bank for ₹6,196 crore

- Bain Capital is set to invest ₹4,385 crore for an 18% stake in Manappuram Finance

Separately, the RBI granted special approval to Canada’s Fairfax to retain a majority stake in CSB Bank for five years – an exception to the standard 40% cap on foreign ownership – recognising it as a strategic revival investment. This highlights the RBI’s positive stance on allowing foreign investment.While each of these deals is significant on its own, they signal something larger, like a global relook at India’s financial sector and growth potential.

While each of these deals is significant on its own, they signal something larger, like a global relook at India’s financial sector and growth potential.

Why Foreign Investors are making bold bets on Indian smaller banks and NBFCs

Favourable regulatory changes: Recent regulatory measures by RBI - including risk-weight cuts across microfinance, MSME, housing, and corporate loans, a 100 bps CRR reduction, and relaxed norms for infra and offshore lending, are expected to free up nearly 2% of banking capital for additional lending, providing a broad-based boost to both banks and NBFCs.

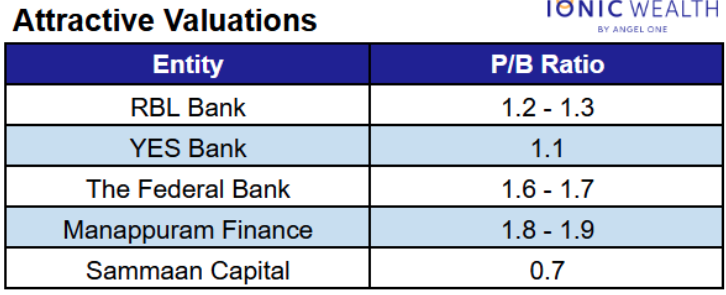

Attractive Valuations, Weak Promoter Backing: Many mid-sized NBFCs and banks trade below 2x P/B and lack strategic ownership - offering scalable platforms at a discount. Strategic investors see potential for value creation through capital, tech, and governance upgrades.

Improved Lending Flexibility: From allowing banks and NBFCs to fund M&As and easing infra lending norms, to liberalising co-lending across all loan types with lower risk retention (20% → 10%), the door is now open for large-ticket, higher-yield, tech-driven credit plays - perfectly aligned with global investors’ mandates.

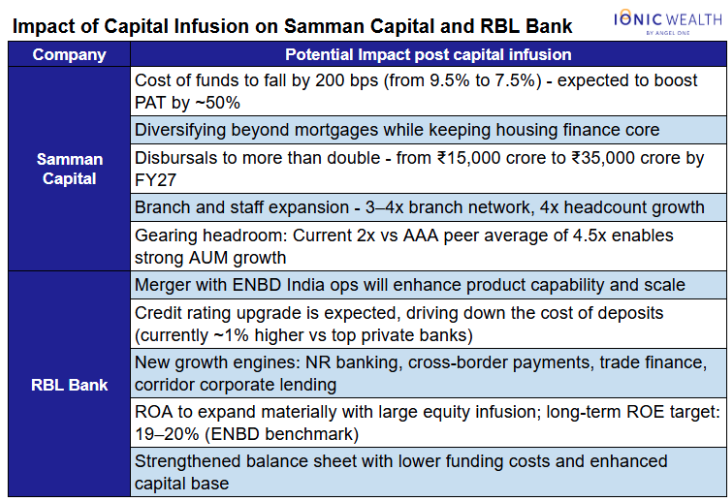

Balance Sheet Leverage Headroom: Many of the NBFCs attracting FII interest have a conservative gearing ratio (Ex Samman Capital has a gearing ratio of 2x compared to its peers at 4.5x). This provides significant AUM growth potential without diluting credit quality or straining capital buffers.

All of this is underpinned by India’s macro resilience amid global uncertainty. Structural reforms, rising consumption, and a renewed capex cycle make India a compelling destination. At Ionic Wealth, we believe this transformation marks a structural shift-India’s banking and NBFC sector is not just resilient; it is primed for cyclical and structural growth. We have discussed this aspect here in detail.

The Impact of Foreign Capital Infusion

Recent foreign capital infusions into NBFCs and mid-sized banks are poised to be transformational, enabling shifts across profitability, scalability, and governance. These are not passive financial investments - they bring operational leverage, strategic clarity, and global best practices. Key potential outcomes would be:

- Credit rating upgrades, lowering the cost of funds

- Stronger balance sheets, enabling entry into higher-yield segments

- Improved Return on Assets (RoA) through more efficient capital deployment

- Product diversification across infra, co-lending, M&A, other high risk products

- Technology and governance upgrades, aligning with global standards

Below is a snapshot of how these infusions are translating into strategic change, as guided by recent management commentaries:

“Emirates NBD brings not only the capital, but also the deep global banking expertise, digital innovation capabilities and access to the vibrant trade corridor between India and the Middle East. This partnership marks the beginning of a new chapter for RBL Bank. We have transitioned from stability to sustained growth from selective participation to the leadership in chosen segments and from being a midsized Indian bank to being a future-ready institution backed by one of the most respected financial groups in the region.” ~ R. Subramaniakumar, CEO, RBL Bank

Why Now – And Not Before?

While India liberalised FDI norms for NBFCs in 2016-allowing 100% foreign ownership under the automatic route-strategic foreign investment into smaller banks and NBFCs remained limited for years.

Investor confidence was constrained by persistent stress in the financial system. The collapses of IL&FS and DHFL, combined with elevated NPAs and weak governance frameworks, led global capital to take a cautious stance toward the sector.

Post-COVID-19, smaller banks and NBFCs saw a structural re-rating driven by

- Stronger, deleveraged balance sheets

- Improved governance and regulatory compliance

- More disciplined and aligned risk frameworks

- Broad-based, accelerating credit demand across retail, MSME, and housing segments

Earlier this month, S&P Global Ratings noted that Indian banks are well-equipped to weather global volatility-from interest rate shocks to currency fluctuations.This is not short-term capital chasing a rebound - it’s a structural re-rating of India’s financial system. Governance has strengthened, balance sheets are healthier, credit demand is rising, and with a robust digital payments backbone, the runway for deeper financial penetration is significant..

Risks: What could go wrong?

Offshore control risks: As foreign investors take majority stakes, strategic decision-making may shift offshore, which might not be aligned with India’s dynamic lending markets

Vulnerability to global shocks: Rising foreign ownership increases exposure to external risks-rate hikes, liquidity crunches, or geopolitical tensions could disrupt domestic credit flows.

Regulatory oversight imperative: While RBI and SEBI have enforced fit-and-proper norms, larger, complex deals now require clearer limits on foreign control to preserve financial sovereignty.

Conclusion

With supportive regulations, robust macro fundamentals, and a resilient economy, India offers a compelling backdrop for strategic foreign capital in its financial sector. For mid-sized banks and NBFCs, this capital is not just funding - it’s permanent growth equity backed by institutional-grade governance and long-term strategic vision.

It brings in more than money: foreign investors offer operational expertise, digital infrastructure capabilities, and product innovation - effectively acting as institutional promoters.

For global investors, these transactions represent strategic entry points into India’s financial services at attractive valuations, with significant headroom for growth.

The outcomes are already visible - lower borrowing costs, improved credit ratings, stronger balance sheets, and RoA expansion. As RBL Bank puts it: foreign partners bring “not only capital, but deep global banking expertise and digital innovation capabilities.” This marks the beginning of a new phase of scale and institutional maturity for India’s emerging financial institutions. Disclaimer

This content is intended for informational purposes only and does not constitute an offer or solicitation for investing in any products distributed by or services made available by Angel One Wealth Limited and Angel One Investment Services Private Limited (collectively referred to as “Ionic Wealth”) or any of their affiliates. It is not intended to be, and should not be construed as, advertising or promotional material. The information provided does not constitute investment advice or a recommendation. You are advised to conduct your own due diligence and consult with its legal, tax and financial advisors before making any investment decisions.

Angel One Investment Services Private Limited is an AMFI-registered Mutual Fund Distributor (ARN 306165). Note that investments in mutual funds and in the securities market are subject to market risks. Read all the investment-related documents carefully before investing.

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

How to Evaluate a PMS Fund Manager: 10 Due Diligence Questio...

Ionic Wealth Tax Team on 3 Aug 2026

Selecting a PMS manager demands scrutiny beyond trailing returns—covering active share, style drift, skin in the game, capacity limits, and tax-adjusted alpha. With SEBI's proposed MF-PMS...

BOJ Holds Rates At 1.0%, Future Policy Tightening Likely

Ionic Wealth Macro Desk on 3 Aug 2026

BOJ held rates at 1.0% (8:1 vote) while upgrading growth forecasts and flagging inflation above 2% in H2 FY26. Persistent yen weakness, not inflation, remains the stronger catalyst for fu...

Post-Vesting Holding Period: Tax Impact of Holding vs Sellin...

Ionic Wealth Tax Team on 31 Jul 2026

Holding foreign RSUs past vesting means navigating FIFO-based capital gains, Budget 2024's flat 12.5% LTCG rate, and DRIP-fractured holding periods. Executives must also track OPI/FEMA di...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved