When to Sell RSUs: Tax-Optimal Strategies for Maximising Net Wealth

Key Takeaways

• Vested Restricted Stock Units (RSUs) are essentially a cash bonus that has already been converted into shares on your behalf.

• Residents in India can face a total perquisite tax of upto 39% at the time of vesting, regardless of whether they sell or hold.

• Failure to report foreign shares correctly in your ITR can attract severe consequences under the Black Money Act, including a ₹10 lakh penalty in relevant cases, even if the shares were sold the same day they vested.

Introduction

Today, equity compensation is no longer a peripheral perk for Indian tech professionals and multinational executives. For many, it has become a primary driver of personal net worth.

Restricted Stock Units (RSUs) are a form of equity-based compensation where employers award employees company shares. These shares convert to actual stock upon meeting specific vesting conditions, which may be based on performance milestones or tenure.

Managing RSUs often presents a psychological hurdle rather than a technical one. A common pitfall is the endowment effect, in which shareholders overvalue vested stock simply because they own it. A more strategic approach removes this emotional loyalty, prioritising objective factors such as tax liability, portfolio concentration, and immediate liquidity needs.

In practice, the most tax-efficient time to sell your RSUs is when they vest. Once you are taxed on the Fair Market Value (FMV) at vesting, holding the stock does not defer the primary tax event. It simply increases your exposure to market volatility, single-stock concentration risk, and future capital gains if you decide to hold the shares.

Is Holding Vested RSUs Mathematically Equivalent to Buying the Stock with Cash?

Many employees mentally separate salary from RSUs. They view the two as different buckets of wealth.

Think of it this way: Once your shares vest and the perquisite tax (which can hit ~39% for high earners) is accounted for, the remaining shares have a clear cash value.

Holding these shares is the same as receiving a cash bonus and immediately using all that cash to buy your company’s stock at the current market price.

An easy way to get out of that trap is to ask yourself, “If my employer gave me a cash bonus today, would I use all of it to buy company stock?”

If the answer is no (because you would rather diversify, preserve liquidity, or fund another priority), then holding the RSUs is a suboptimal use of your capital.

It would be rather wise to invest the amount in something you deem more productive and in line with your financial goals.

Should I Use "Sell-to-Cover" or Pay the Vesting Tax with Outside Cash?

On the vesting day, you have to decide how you want to fund the tax bill.

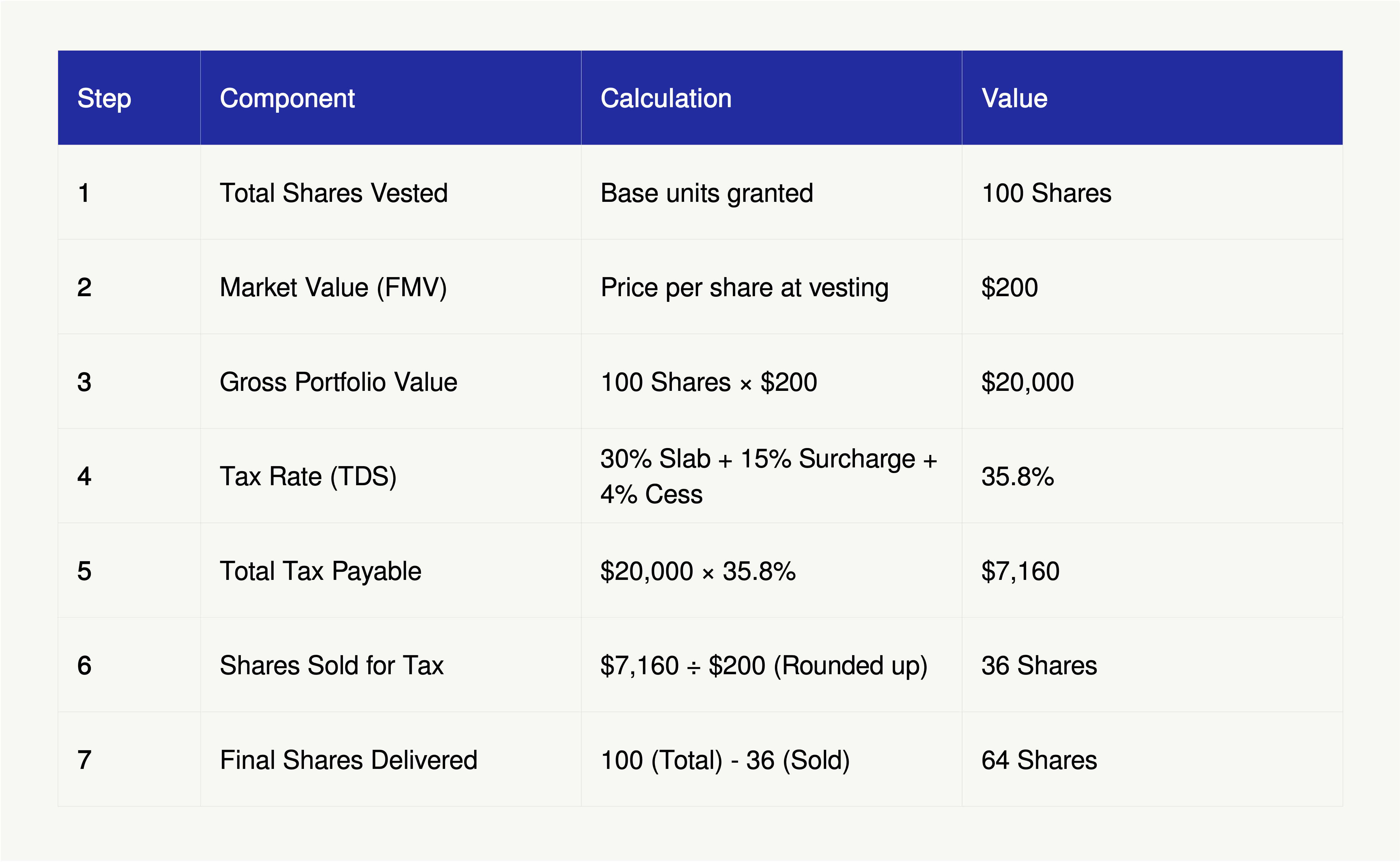

Option A (Sell-to-Cover): This is the most common route. Your broker liquidates roughly 31.2% to 35.8% of your shares to cover the Indian TDS. This requires zero out-of-pocket cash but reduces your equity immediately.

Let’s take the example of Mr Arjun, a senior engineer at a Bengaluru-based MNC, who opens his broker's dashboard and sees a notification he's been waiting months for: 100 shares have vested. At today's price of $200 a share, that's $20,000 sitting in his account.

For a moment, it feels like a windfall. But it isn't. What Arjun is really looking at is a salary payment that his employer decided to make in stock rather than cash.

If Arjun chooses the “Sell-to-Cover” option, then his broker will liquidate 36 of his 100 shares (worth ~$7,160) to cover TDS. Arjun walks away with 64 shares and zero out-of-pocket expense. It's clean, simple, and the most common route.

This example assumes Mr Arjun's total income is between ₹1 crore and ₹2 crore, where a 15% surcharge applies.

Option B (Cash Funding): You pay the tax using personal savings to keep 100% of the shares. This is essentially a "buy" decision and only makes sense if you have high conviction that the stock is currently undervalued, and you have ample liquidity.

Under this option, Mr Arjun would need to pay $7160 in taxes to the income tax department out of his own pocket. It only makes financial sense if Arjun has a high conviction that the stock is currently undervalued and if he has liquidity to spare.

For most employees, increasing exposure to the same company that already funds their salary is rarely prudent. By the time vested RSUs are added to unvested grants and future compensation, many executives are already far more concentrated than they realise.

Does Selling RSUs Immediately Upon Vesting Trigger Additional Capital Gains Tax?

Selling immediately or within a few days of vesting generally results in near-zero capital gains.

The perquisite value is calculated as:

(Perquisite Value) = (FMV on Vesting Date) * (Number of Shares)

Unlike ESOPs, RSUs carry no exercise price, so the entire FMV on the vesting date is treated as salary income. Since the FMV on the vesting date becomes your Cost of Acquisition for tax purposes, a sale at or near that same price usually leaves little or no gain to tax.

Minor gains or losses may still occur due to slight stock price movements or USD-INR exchange rate fluctuations between the vest and settlement dates, but these are generally negligible.

What Happens to My Tax Liability if the Stock Price Crashes After Vesting?

The biggest risk of holding RSUs is the "Phantom Income" trap.

Imagine your RSUs vest when the stock is at $200. Your perquisite tax is computed on that $200 value. If the stock subsequently falls to $100, your tax liability is locked at the original $200 valuation.

The Indian Income Tax Department does not offer refunds for lost market value. While selling at $100 results in a Short-Term Capital Loss (STCL), it cannot be offset against your salary income. It can only be used against other capital gains. You might just end up paying more in taxes than the actual cash you’ll get from the sale.

How Long Must I Hold Foreign RSUs to Benefit from LTCG Rates?

If you choose to hold after vesting, the post-Budget 2024 framework is broadly as follows:

The Tax Impact of Holding Periods

How Do Blackout Periods and Insider Trading Windows Dictate My Sell Strategy?

Publicly listed MNC employees are often restricted by company trading windows and blackout periods. Where U.S. securities rules apply, a Rule 10b5-1 Trading Plan can enable automated, prearranged sales within a defined framework. It offers an affirmative defence against insider-trading allegations and, just as importantly, imposes discipline on what is often an emotionally charged decision.

For the European Union, employees can use pre-set discretionary trading plans or "closely associated persons" arrangements to schedule sales outside closed periods, under the Market Abuse Regulation (MAR). In Canada, the Automatic Securities Disposition Plans (ASDPs) are equivalent to 10b5-1 plans.

How Can I Use Tax-Loss Harvesting to Offset RSU Capital Gains?

If your RSUs have appreciated significantly, tax-loss harvesting can soften the tax impact. The idea is simple: selling underperforming assets in the portfolio to offset gains from the RSU sale.

STCL (Short Term Capital Loss) can offset both STCG (Short Term Capital Gains) and LTCG (Long Term Capital gains). However, LTCL (Long Term Capital Loss) can be offset only against LTCG (Long Term Capital gains).

The Impact of Holding vs. Selling in a Volatile Market

Consider two strategies for an employee with ₹50 Lakh in vested RSUs:

Strategy A (Sell & Diversify): The employee sells immediately, paying ₹0 in capital gains. They reinvest the net proceeds into a diversified index fund. They have eliminated single-stock risk and protected their gains.

Strategy B (Hold Company Stock): The employee holds for 24 months. For this to be mathematically superior, the company stock must not only outperform the diversified index but also grow enough to cover the 12.5% LTCG tax due on the back end.

As Hardik Mehta, Lead Tax Consultant at Ionic, notes: “By keeping the sale proceeds of U.S. assets in an offshore or GIFT City account, investors can preserve their annual $250,000 LRS headroom and potentially avoid a fresh TCS friction that may arise if the money is first brought into India and later remitted outward.”

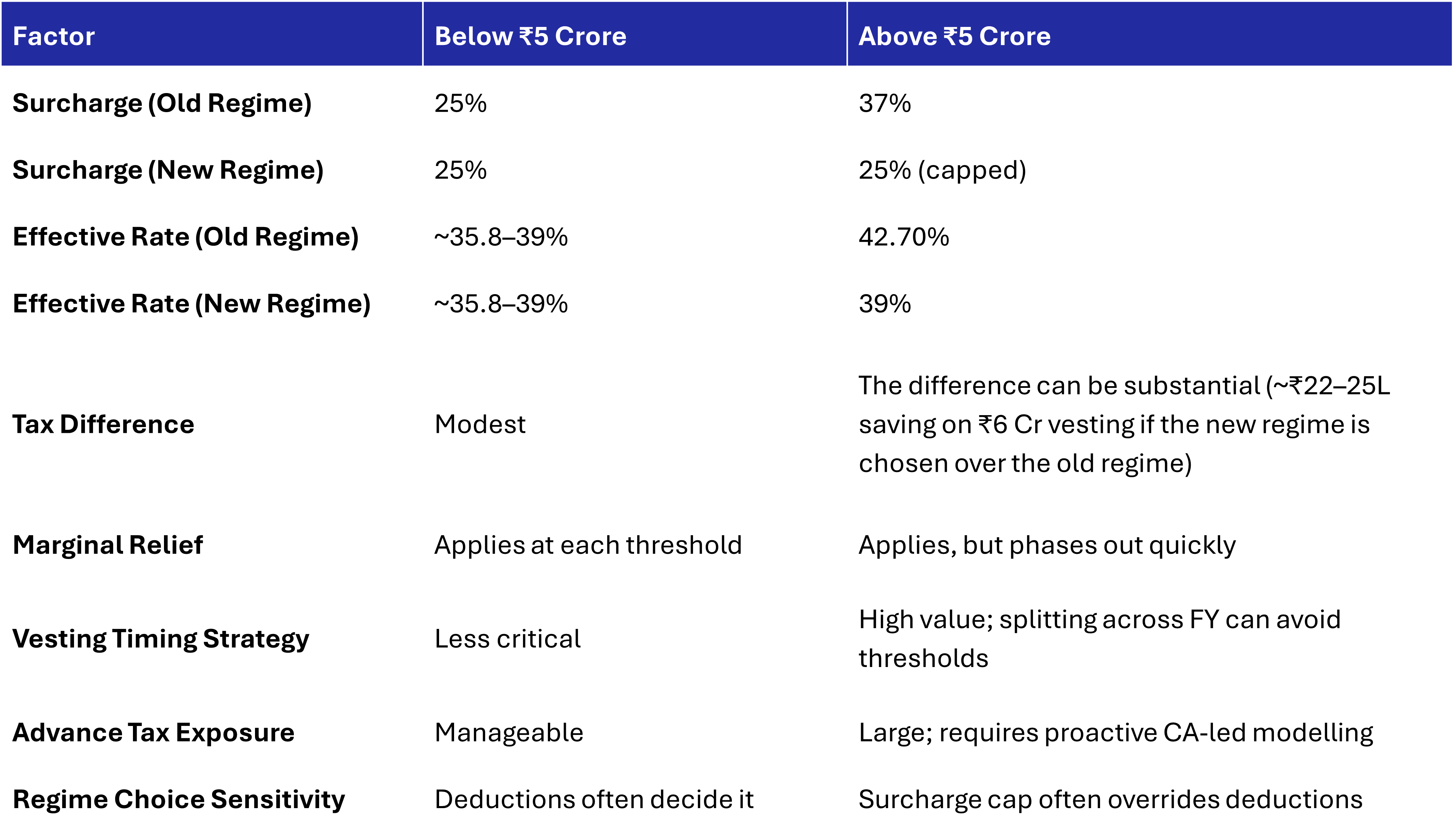

What changes when the RSU pool crosses ₹5 crore?

If we assume Mr Arjun from our previous example was instead a CTO whose total income (Salary + Vested RSUs) exceeded ₹5 Crore, the decision to sell RSUs and diversify would have involved a new layer of tax surcharge.

See, once total income crosses ₹5 crore in a financial year, RSU taxation enters a new surcharge tier that meaningfully changes the math. At this level, Arjun’s tax regime choice also acts as a "Liquidity Multiplier" for him.

By choosing the right regime, he can effectively lower the cost of diversification by several lakhs, leaving him with more capital to reinvest in other assets.

This happens because the Old Tax Regime penalises high-value sale of vested RSUs with a 37% surcharge. The New Regime, however, caps this at 25%. This 12% difference in surcharge translates to a ~3.7% difference in your take-home cash.

If you are planning a large sell-to-cover or a full liquidation of a vested block, this would effectively put a ceiling on your tax liability and also provide you with more money to reinvest.

Also, at these income levels, the value of the surcharge cap almost always outweighs any personal deductions (like HRA or Home Loan interest) available under the Old Regime.

Ionic Insight: If your vesting schedule is flexible, one of the most effective diversification strategies is to split a large vest across the March 31st boundary. By keeping your total income just below the ₹5 Crore threshold in two separate financial years, you avoid the 37% surcharge trap entirely, regardless of which regime you choose.

How Does the USD-INR Exchange Rate Impact My Net Wealth from RSUs?

Holding US-listed RSUs is also a bet on the USD-INR exchange rate. Per Rule 115, taxes are calculated using the SBI Telegraphic Transfer (TT) Buying Rate. If the Rupee depreciates, you gain in INR terms even if the stock stays flat. If the Rupee strengthens, your net wealth shrinks even if the stock price goes up.

How Do I Manage the Advance Tax Trap When Liquidating Large RSU Blocks?

Foreign brokers do not deduct Indian TDS on capital gains. If your total tax liability on a sale exceeds ₹10,000, you must pay Advance Tax in quarterly instalments:

• June 15 (15%)

• Sept 15 (45%)

• Dec 15 (75%)

• March 15 (100%)

Failure to comply results in penal interest of 1% per month, which can significantly erode your net gains.

Conclusion

Managing RSUs is a journey that begins with the technical hurdle of understanding the tax code but ultimately ends with a strategic one of building a resilient portfolio. For executives like Mr Arjun, the goal isn't just to "pay less tax," but to ensure that the wealth built through years of hard work isn't eroded by a single bad quarter or a sudden regulatory shift. Hence, diversification, tax planning, and addressing psychological hurdles like the endowment effect are key to true financial independence.

Frequently Asked Questions (FAQs)

Do I still need to file Schedule FA if I sell my RSUs the same day they vest?

Yes. Holding a foreign asset for even one day requires mandatory reporting in Schedule FA to avoid a penalty of ₹10 lakh under the Black Money Act.

Can I transfer my RSUs to my spouse to lower the capital gains tax?

No. Under the clubbing provisions of Section 64, gains arising from assets gifted to a spouse are added back to your taxable income.

Should I use my RSUs to fund my child’s foreign education?

This can be highly efficient. Paying a U.S. university directly from a USD pool may reduce the need for a fresh outward remittance from India and, depending on the route and thresholds involved, may also reduce TCS friction under the LRS framework.

What happens if my company is acquired?

In a cash buyout, unvested units may accelerate, potentially triggering perquisite tax, while vested shares may be liquidated, potentially triggering capital gains.

How do I manage the Advance Tax trap?

Foreign brokers do not deduct Indian TDS on capital gains. If your liability exceeds ₹10,000, review your advance-tax position carefully and pay the required instalments on time to avoid interest exposure.

Disclaimer: This guide is for informational purposes and based on tax laws as of 2026. Consult a qualified tax professional for personalized advice.

Note: This guide walks through scenarios across multiple income brackets. Mr Arjun's worked example assumes a total income between ₹1 crore and ₹2 crore, where the effective tax rate at vesting is approximately 35.88% (30% slab + 15% surcharge + 4% cess). The "Above ₹5 Crore" section addresses the highest bracket separately, where effective rates rise to 39% (new regime) or 42.74% (old regime). Readers should map the framework to their own income bracket.

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

How to Evaluate a PMS Fund Manager: 10 Due Diligence Questio...

Ionic Wealth Tax Team on 3 Aug 2026

Selecting a PMS manager demands scrutiny beyond trailing returns—covering active share, style drift, skin in the game, capacity limits, and tax-adjusted alpha. With SEBI's proposed MF-PMS...

BOJ Holds Rates At 1.0%, Future Policy Tightening Likely

Ionic Wealth Macro Desk on 3 Aug 2026

BOJ held rates at 1.0% (8:1 vote) while upgrading growth forecasts and flagging inflation above 2% in H2 FY26. Persistent yen weakness, not inflation, remains the stronger catalyst for fu...

Post-Vesting Holding Period: Tax Impact of Holding vs Sellin...

Ionic Wealth Tax Team on 31 Jul 2026

Holding foreign RSUs past vesting means navigating FIFO-based capital gains, Budget 2024's flat 12.5% LTCG rate, and DRIP-fractured holding periods. Executives must also track OPI/FEMA di...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved