The AI Build-Out: Who's Paying, Who's Profiting

.png&w=3840&q=75)

Two sides of the AI Build-Out. The picks and shovels remain dependable; the platforms become worthy of a second look

The Magnificent 7's leadership has faded .— The seven make up roughly a third of the S&P 500 (about 32.7% in mid June), so their moves swing the whole index. They peaked on 29 October 2025, when their combined value crossed $20 trillion, and have since fallen more than 10% while the rest of the market held broadly steady. The cause isn't weak businesses — 2026 earnings forecasts have largely held up — but growing investor doubt over whether the group's enormous AI capex will earn an adequate return.

Meanwhile, the suppliers to the build-out have kept compounding. The picks and shovels of this cycle sit in specific subsectors: foundry (TSMC), memory and storage (Micron, SK Hynix, WesternDigital), equipment (Applied Materials, Lam Research, ASML), networking and custom silicon (Broadcom, Arista), and optical components (Lumentum, Coherent). The Philadelphia Semiconductor Index has surged over 65% year-to-date, and Broadcom has overtaken Meta and Tesla by market value.

The two sides are connected. The spending testing investors' patience with the Mag 7 is the suppliers' revenue. The group put an estimated $320 billion into AI last year, and budgets keep rising — Amazon alone is guiding capex up 56% to $200 billion in 2026. Every dollar flows down the chain: to the foundries, memory makers, equipment firms and networking suppliers that build and connect the data centers.

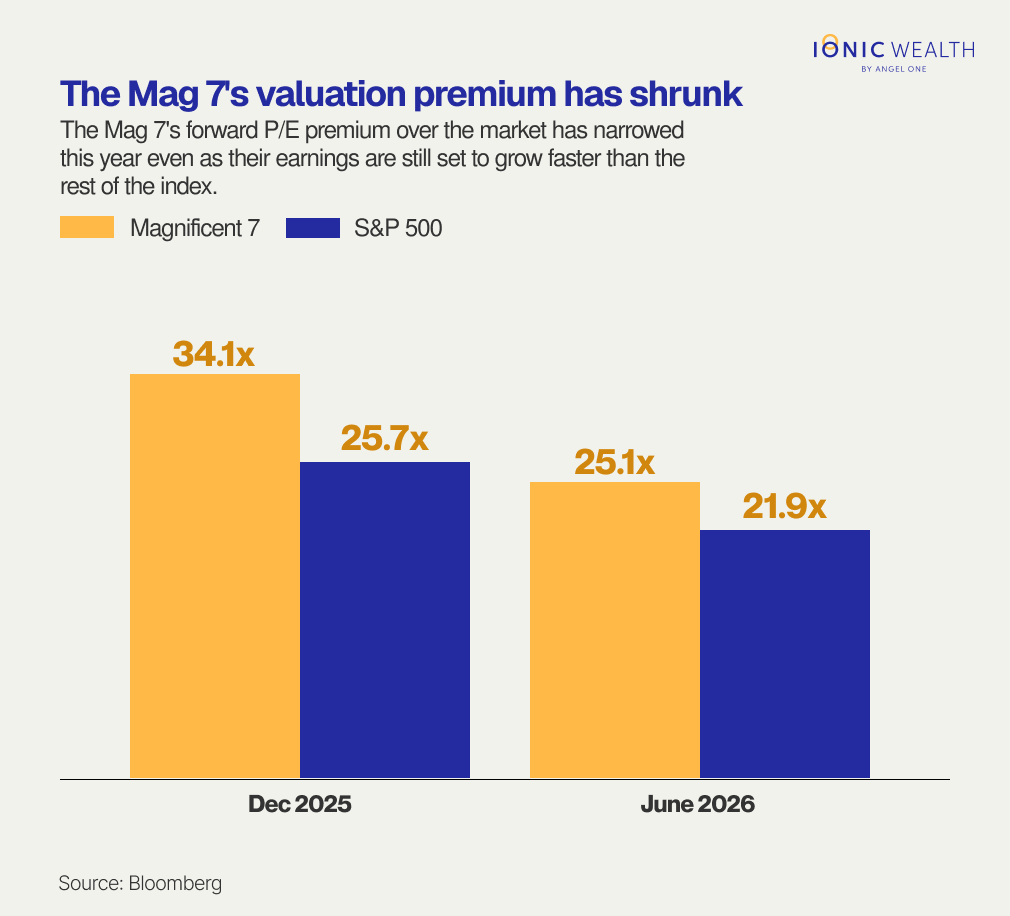

The pullback has left the Mag 7 at a rare valuation. They trade near 25x forward earnings versus ~22x for the S&P 500 — the lowest premium to the rest of the market in a decade — while profits are still set to grow about 18% in 2026 versus ~13% for the rest. Meta now trades below the index itself, at ~18.3x forward. Faster grow that a shrinking premium is a combination this group has rarely offered.

Ionic View

Our approach through the AI cycle has been to own the layer that gets paid for the build-out — the foundries, memory makers, equipment firms and networking and optical suppliers — rather than the platforms funding it. We continue to see this picks-and-shovels layer as the most dependable expression of the AI theme. At the same time, the Mag 7's derating to its smallest premium in a decade — faster growth for a shrinking multiple — has restored genuine selective value in the platforms, and we see the two as complements: the enablers for the build-out, and the platforms for the payoff.

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

Asset X | July 2026: Key Signals Across Asset Classes

Ionic Wealth Macro Desk on 6 Jul 2026

AssetX's July 2026 edition tracks a market shift from volatility to stabilization: Indian equities move to lumpsum deployment on easing geopolitical risk, while global equities show broad...

When AI Agents Start Doing the Shopping

Ionic Global Research on 30 Jun 2026

AI agents are starting to handle online shopping end-to-end, from product discovery to payment to delivery. Visa, Mastercard, Stripe, and Adyen are all building the payment infrastructure...

Tax Planning for CTC Above ₹1 Crore: Salary Restructuring & ...

Ionic Wealth Tax Team on 25 Jun 2026

Crossing ₹1 crore in taxable income triggers a surcharge jump from 10% to 15% on your entire tax liability — a cliff most high earners don't see coming. This guide breaks down how to rest...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved