Tax Planning for CTC Above ₹1 Crore: Salary Restructuring & Investment Strategy

Key Takeaways

• Crossing the ₹1 crore threshold triggers a jump in surcharge from 10% to 15% on your entire tax liability, though Marginal Relief acts as a critical safety net to ensure the extra tax paid doesn't exceed the incremental income earned.

• High earners can significantly lower their Effective Tax Rate by shifting fully taxable "Special Allowances" into tax-leveraged components, such as the National Pension System (NPS), which allows employer contributions up to 14% of basic salary to be tax-exempt under the new regime.

• RSUs and ESOPs are taxed as perquisites at your peak slab rate upon vesting, making it essential to time exercises and monitor cumulative income to prevent a large equity "tax bomb" from pushing you into a higher surcharge bracket.

• Beyond basic tax savings, individuals in this bracket should utilise tax-efficient strategies like income-splitting with parents, tax-loss harvesting to offset capital gains, and utilising car leases to pay for vehicles with pre-tax income.

For many corporate leaders in India, the journey to a ₹1 Crore Cost to Company (CTC) is a multi-decade-long climb. For Amita, a software architect who recently crossed this milestone, the view from the top was unexpectedly expensive.

Her CTC letter read ₹1.2 crore. When her first annualised pay projection landed a week later, she noticed her net take-home had not grown nearly in proportion to the gross. Her finance team pointed to a familiar culprit: Amita had walked into the surcharge cliff. Crossing ₹1 crore in taxable income had pushed her from a 10% surcharge bracket to 15%. The higher rate applied to her entire tax liability, not just the extra rupee that put her over the line.

Once you cross the 1 crore threshold, tax planning is no longer a year-end chore of maximising Section 80C.

Why is the ₹1 Crore CTC Threshold a "Tax Cliff" in India?

Imagine walking up a flight of stairs where the last step is twice as high as the others. That is the ₹1 Crore threshold for you. In India, once a tax slab threshold is crossed, a "surcharge", which is a tax on the tax, kicks in.

When Amita earned ₹99 Lakhs, she paid a 10% surcharge on her total tax. The moment her income crossed ₹1,00,00,001, the surcharge jumped to 15%, and that higher rate applied to the entire tax liability — not merely the marginal rupee that tipped her over.

To prevent a scenario where earning one extra rupee costs you two in taxes, the Income Tax Act provides Marginal Relief. This acts as a safety net. The additional tax Amita pays (including the higher surcharge) cannot exceed the additional income she earned above the threshold.

If we assume Amita's income to be ₹1.02 crore instead, then the tax department effectively calculates her liability in two ways.

1. The "surcharge" calculation applies the full 15% surcharge on tax computed on ₹1.02 crore.

2. The "marginal relief" calculation caps her tax at what she would have paid on exactly ₹1 crore (with 10% surcharge) plus the extra ₹2 lakh she earned.

She pays whichever is lower. For anyone crossing the ₹1 crore mark, understanding marginal relief is the first step in financial defence, but it is only a defence. Restructuring is where the offence begins.

Marginal Relief is a protective mechanism that operates when income is close to the ₹1 crore threshold. The restructuring example below addresses a different challenge of reducing tax liability for someone already comfortably above that threshold. Both are important, but they solve different problems.

How Should You Restructure Your Salary Components to Lower Taxable Income?

Amita's existing salary structure was dominated by a single line item: Special Allowance. For someone earning over ₹1 crore, this is the biggest tax bill on the payslip. It is fully taxable at the highest slab. To lower the taxable base, one needs to move away from cash allowances and toward components that carry tax leverage.

National Pension System (NPS)

Under Section 80CCD(2), your employer can contribute up to 14% of your Basic salary directly into your National Pension System (NPS) account. This is as per the New Regime (under the Old Regime, the limit is 10%). For a ₹1.2 Crore CTC with a ₹40 Lakh Basic salary, this move alone can reduce Amita’s taxable income by ₹5.6 Lakhs.

Retirals vs. Take-home

There is a strategic tension between maximising your Provident Fund (PF) versus taking that cash as a taxable allowance. While PF offers tax-free compounding, any employer contribution exceeding ₹7.5 Lakhs (combined across PF, NPS, and Superannuation) is taxable. Finding the "sweet spot" just below this threshold is important.

Flexi-Benefits

While the New Tax Regime has phased out many perks, those sticking to the Old Tax Regime should still maximise Leave Travel Allowance (LTA), food coupons, and particularly car leases. A car lease allows you to pay for a vehicle using "pre-tax" income, effectively reducing your taxable salary by the EMI amount.

How Do RSUs and ESOPs Impact Your Surcharge Calculation?

For Amita, the real danger wasn't her monthly salary. It was her Restricted Stock Units (RSUs). These equity grants are taxed as perquisites, as part of salary when they vest, at the employee's slab rate on the full fair market value.

A large RSU vest can be a significant tax event. If Amita’s base salary is ₹90 Lakhs and a ₹15 Lakh equity vest hits her account in March, she is suddenly pushed from a 10% surcharge bracket into the 15% bracket.

By failing to time her Employee Stock Ownership Plan (ESOP) exercises or RSU sales carefully, she could lose a massive chunk of her "wealth" to a higher surcharge bracket that applies to her entire income.

The practical discipline here is to map out, at the start of each financial year, when vests are expected and what the cumulative income trajectory looks like. If a vest is going to push her across a surcharge threshold, she can talk to her advisor about whether any component of the overall remuneration can be deferred, or whether the exercise timing on any optional equity can be shifted.

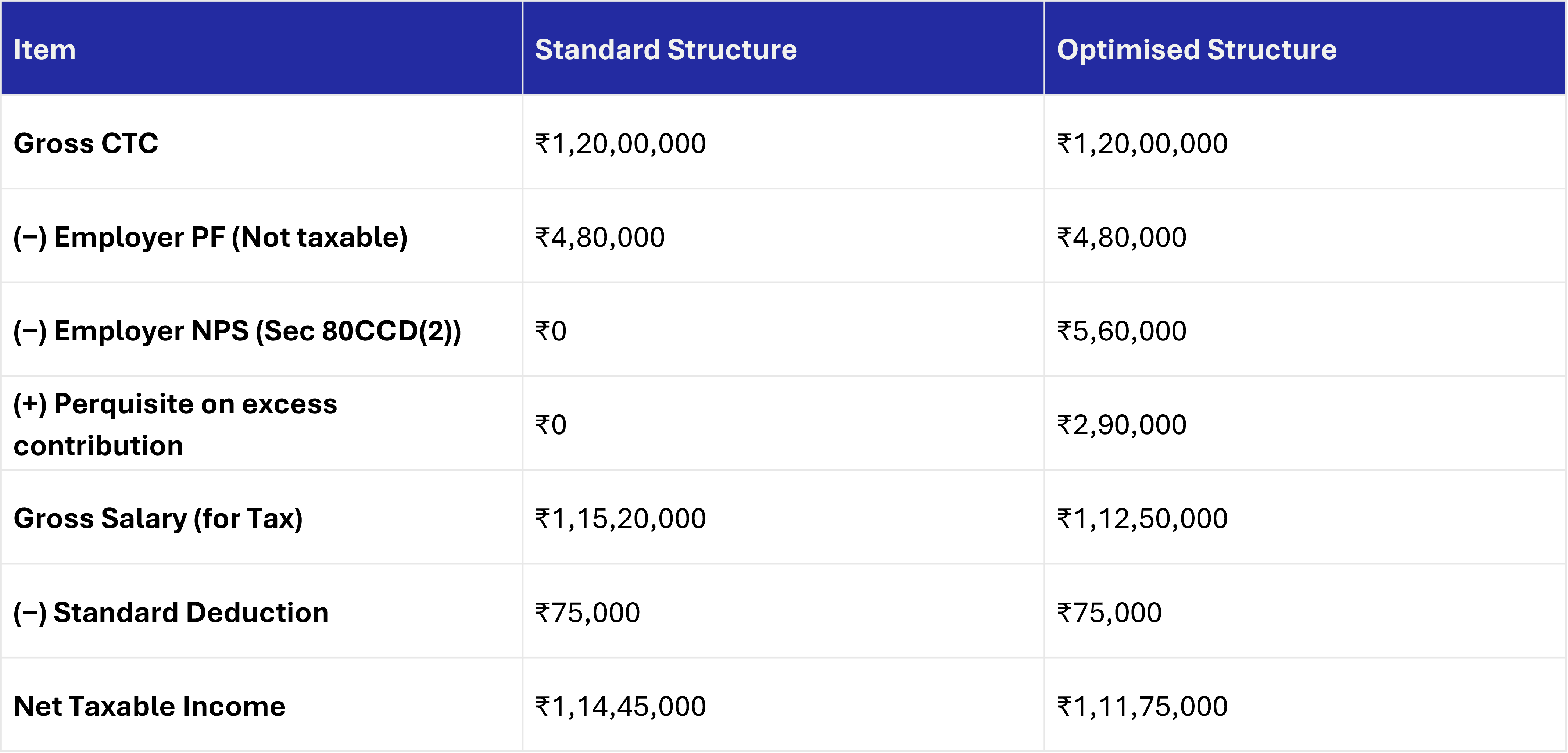

Real-World Example: Tax Impact of Restructuring a ₹1.2 Crore CTC

To see the math in action, Amita compared her old "High Basic" structure against a new "Optimised" version. By shifting funds from taxable allowances to tax-exempt contributions, the results were startling. But to come up with the final figures, we will need to go through a 4-step calculation process.

Step 1: Arriving at Taxable Income

The combined employer contribution to PF (₹4.80L) and NPS (₹5.60L) totals ₹10.40L, which exceeds the ₹7.50L threshold under Section 17(2)(vii). The excess of ₹2.90L is therefore taxed as a perquisite in the employee's hands and gets added back to taxable income in the optimised structure. (Note: All calculations are based on the new tax regime)

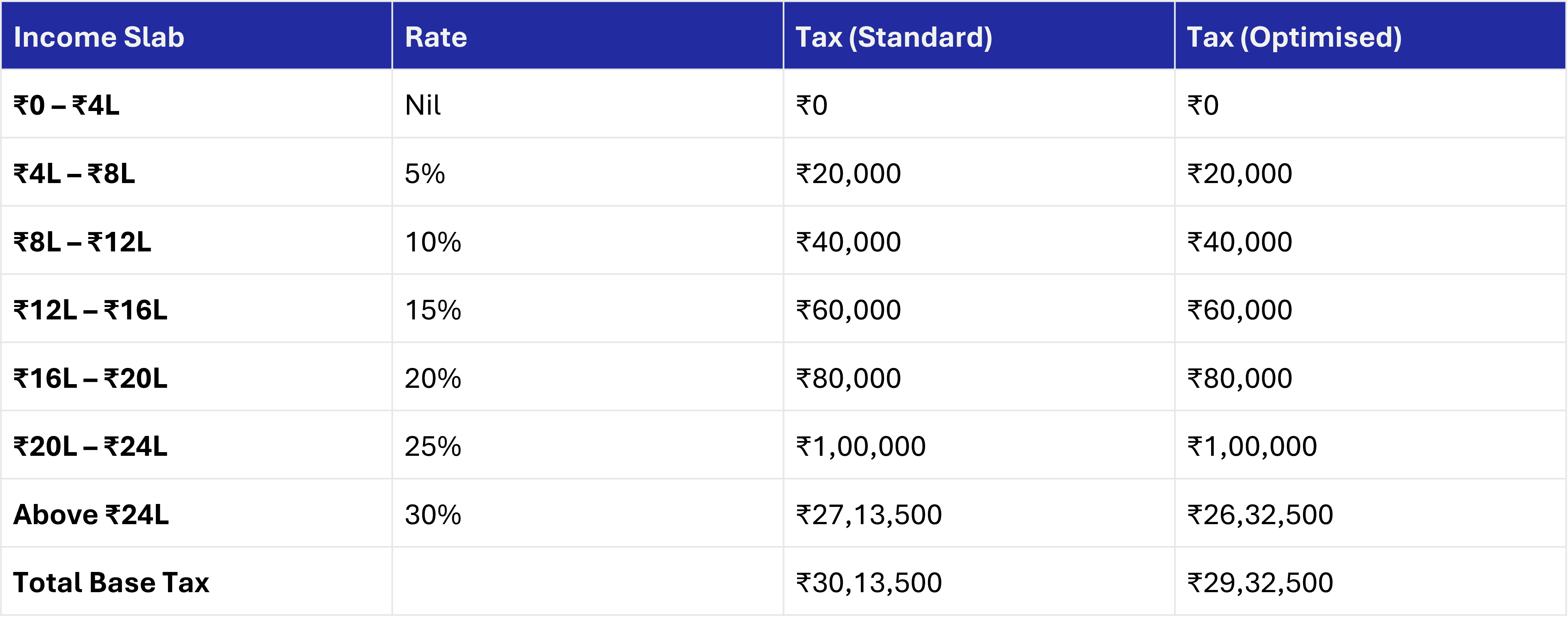

Step 2: Slabwise tax

(Above ₹24L for Optimised: ₹1,11,75,000 − ₹24,00,000 = ₹87,75,000 × 30% = ₹26,32,500)

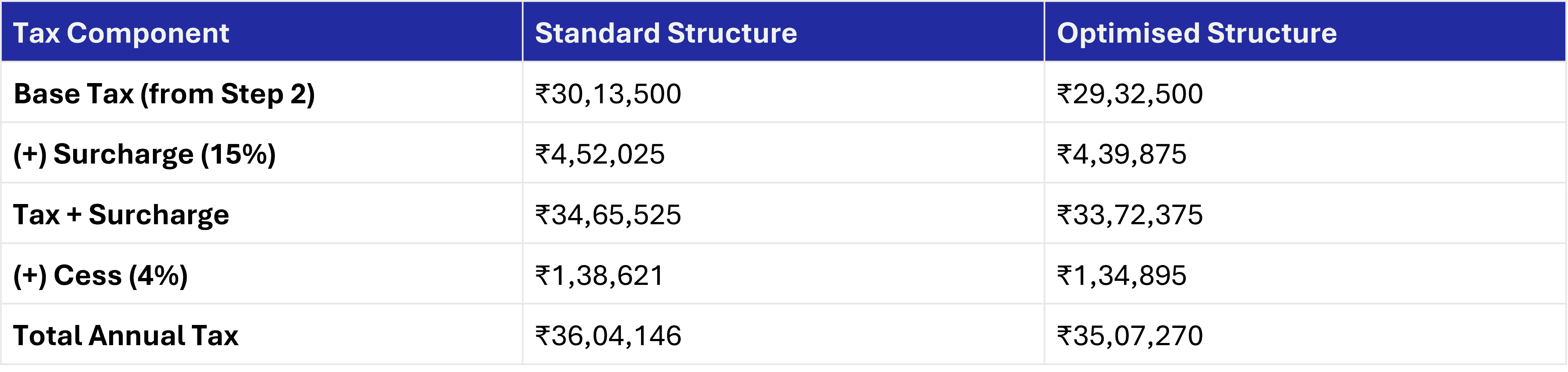

Step 3: Adding the Surcharge & Cess

Step 4: Net Take-Home Math

"Take-Home" is what hits Amita’s bank account after Tax and Employee contributions (PF/NPS) are deducted.

Standard Post-Tax Income: ₹1,15,20,000 − ₹36,04,146 − ₹4,80,000 = ₹74.36 Lakhs

Optimised Post-Tax Income: ₹1,12,50,000 − ₹35,07,270 − ₹4,80,000 = ₹72.63 Lakhs

Because of the optimised structure, ₹5.60 Lakhs is being deposited into Amita's NPS account rather than her bank account. After accounting for the perquisite tax on the excess employer contribution, she pays approximately ₹96,876 less in tax and that saving is growing in a retirement fund rather than being spent today.

(Note: The savings figure is illustrative and will vary with exact employer policy, regime choice, and the employee's other deductions. But the principle holds: at her income level, the salary structure itself is a lever.)

What Changes at the ₹2 Crore and ₹5 Crore Income Thresholds?

The ₹1 crore threshold is just the first step. India's surcharge structure has two more steps above it, each with meaningfully different implications.

At a taxable income of ₹ 2 crore, the surcharge jumps to 25% under both new and old tax regimes. For someone earning between ₹1 crore and ₹2 crore, the strategies outlined in this article — NPS contributions, structured allowances, RSU timing — are sufficient levers. But as income approaches ₹2 crore, the focus must shift to ensuring that equity vests, bonuses, and year-end variable pay do not inadvertently push total income over this second cliff. The mathematics of surcharge on tax at 25% vs 15% are stark enough that even a short-term deferral of a discretionary bonus is worth modelling.

Under the old tax regime, at ₹5 crore, the surcharge reaches its highest rate of 37%, pushing the effective tax rate on salary and interest income to close to 42.74%. This is the bracket where the regime choice becomes the single most important decision. Under the new tax regime, surcharge on all income is capped at 25%, regardless of how much the total income exceeds ₹5 crore. For most professionals at this level who do not have very large HRA, home loan interest, or legacy 80C investments, the new regime with its 25% surcharge cap will outperform the old regime at 37%. The breakeven calculation no longer favours the old regime unless the total deductions pool is exceptionally large.

One structural point that applies across all three thresholds is that long-term capital gains on listed equity are subject to a 15% surcharge cap, regardless of total income. So even if you are in the 37% surcharge bracket on your salary, your equity investment gains do not carry that same surcharge burden. This asymmetry is one more reason why, at higher income levels, shifting savings into equity mutual funds and direct stocks (rather than interest-bearing instruments) is not just a return decision; it is a tax decision.

What Investment Strategy Best Complements a ₹1 Crore+ Salary?

Once the salary structure was in place, Amita had to adjust her investment strategy. At her level, she doesn’t need "tax-saving" products. She needs tax-efficient strategies that help her enhance post tax returns and preserve more of her wealth. It is advisable for a person in this salary bracket to follow these investment steps to make the best out of their capital.

• Specialised Investment Funds (SIFs): Amita can explore Specialised Investment Funds (SIFs) for her investments where she can get started with a minimum contribution of ₹10 Lakh. Unlike traditional Mutual Funds (MFs), SIFs allow tactical moves such as long-short strategies and hedging. Most importantly, SIFs are more tax-efficient than many Alternative Investment Funds (AIFs) because gains are taxed as capital gains at the investor level rather than as business income.

• The Family Portfolio Strategy: Amita can use income-splitting to shift interest income from her own 39% effective tax bracket to family members in lower brackets. A gift from an individual to a parent is tax-exempt under Section 56. Because Section 64 clubbing provisions apply to gifts to a spouse or minor child but not to parents, the income generated on those invested funds is taxed in the parents' hands at their slab (which may be zero up to their basic exemption limit). The saving compounds year over year.

• Tax-Loss Harvesting: Every quarter, Amita can review her portfolio for "underperformers." By selling assets at a loss, she can create a tax loss that offsets her Long-Term Capital Gains (LTCG). Under the current rules, where LTCG is taxed at 12.5%, this strategy is essential for protecting net returns.

Frequently Asked Questions (FAQs)

Does my employer-provided car lease really save tax at my bracket?

Yes. Because the lease EMI is deducted from your pre-tax salary, you pay for the car, saving the 30% tax and 15% surcharge you would have otherwise paid on that income.

Can I use Section 80G donations to stay below a surcharge threshold?

While Section 80G deductions can reduce taxable income, their practical utility is limited. Most donations made under Section 80G attract only a 50% deduction, and some are further subject to a 10% ceiling on adjusted gross total income. That said, with careful planning, they can still help reduce your surcharge bracket if they bring total income below a threshold.

How is the surcharge calculated if I have large capital gains?

The government provides a "Surcharge Cap" of 15% on Long-Term Capital Gains (LTCG) and Short-Term Capital Gains (STCG) for listed equities, ensuring you aren't unfairly penalised for investment success.

Is the ₹50,000 Standard Deduction available in both regimes for my income level?

The standard deduction differs depending on the tax regime you have chosen. The standard deduction limit is ₹75,000 under the new income tax regime and ₹50,000 under the old income tax regime. Both apply regardless of CTC, but the new regime amount is higher and is now the default.

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

.png&w=3840&q=75)

The AI Build-Out: Who's Paying, Who's Profiting

Ionic Global Research on 7 Jul 2026

The Magnificent 7 has poured hundreds of billions into AI, yet its stock market leadership has faded and its valuation premium over the rest of the market has narrowed to the smallest gap...

Asset X | July 2026: Key Signals Across Asset Classes

Ionic Wealth Macro Desk on 6 Jul 2026

AssetX's July 2026 edition tracks a market shift from volatility to stabilization: Indian equities move to lumpsum deployment on easing geopolitical risk, while global equities show broad...

When AI Agents Start Doing the Shopping

Ionic Global Research on 30 Jun 2026

AI agents are starting to handle online shopping end-to-end, from product discovery to payment to delivery. Visa, Mastercard, Stripe, and Adyen are all building the payment infrastructure...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved