RSU Taxation in India

Key Takeaways

• RSUs are taxed twice in India. First, as Salary Income (Perquisites) upon vesting based on the Fair Market Value (FMV), and second, as Capital Gains when the shares are eventually sold.

• Following recent changes, Long-Term Capital Gains (LTCG) on foreign RSUs (held for >24 months) are now taxed at a flat 12.5% without indexation, while Short-Term gains are taxed at the applicable income tax slab.

• Even if you don't sell your Foreign RSU shares, you must disclose them in Schedule FA of your ITR. [TD1.1]Failure to do so can trigger a penalty of ₹10 lakh per year of omission under the Black Money Act.

• Under FEMA guidelines, proceeds from the sale of foreign RSUs must generally be brought back to an Indian bank account within 180 days unless reinvested in permissible overseas investments.

RSU Taxation in India: Complete Guide for Tech Employees

If you are an Indian working for a global tech company, chances are a portion of your employee compensation is in the form of Restricted Stock Units (RSUs). Fundamentally, an RSU is a company’s commitment to give you shares at a future date, provided that you meet certain conditions, which are related to your tenure or performance.

Since most tech employees receive RSUs from their foreign parent company, factors like foreign asset reporting, advance tax, and exchange rates come into play.

When you file your taxes in India, you must declare and pay tax on these RSUs at two distinct stages: first, as salary income (perquisite) at vesting, and later as capital gains at sale.

How Are RSUs Taxed When They Vest in India?

An RSU grant itself does not trigger a tax event since the transfer of shares hasn’t occurred. The tax friction begins at vesting, when the employer transfers actual ownership of the shares to you.

Section 17(2)(vi) of the Income Tax Act 1961 (applicable for FY 2025-26) and Section 17(1)(d) (applicable for FY 2026-27) taxes such shares as a perquisite to employees. Tax is paid on the RSU's Fair Market Value (FMV) on the vesting day. For shares not listed in India, the FMV is determined by a Category 1 merchant banker registered with SEBI.

For foreign RSUs, the employee must convert the FMV into INR using the SBI Telegraphic Transfer (TT) Buying Rate on the vesting date, as per Rule 26 of the Income Tax Rules, 1962.

The FMV of RSUs is reported as “Income From Salary” and taxed as per the applicable tax slabs.

What is "Sell-to-Cover" and How Does TDS Work for RSUs?

The defining advantage of RSUs is the absence of a painful "cash trap" during the acquisition phase. Most global employers manage the tax liability through a "sell-to-cover" mechanism, where the company automatically liquidates a portion of your vested shares to fund the Tax Deducted at Source (TDS) obligation. This ensures that you aren't forced to invest your own liquid cash just to receive your shares.

Generally, if you are in the 30% tax bracket, your employer might sell roughly 30-40% of your grant to satisfy the government's requirements, and transfer the balance, 60-70% of the shares to your account. This TDS amount is reflected in your Form 16 as a perquisite. While this is convenient, it also means you have no choice regarding the timing of this initial sale, which can be a consideration if you were hoping to hold a more concentrated position for future appreciation.

Are RSU Dividends Taxed Before You Sell Them?

Many employees hold vested shares and receive dividends, which are taxable as "Income from Other Sources" as per the Income Tax Act. If the dividend is from a foreign RSU, a withholding tax is deducted.

The Indian government has double taxation avoidance agreements (DTAAs) with several countries to prevent Indian investors from paying full tax in both countries on the same income. In many cases, the tax amount is reduced if proper documentation is provided.

For example, India has signed a DTAA with the US government. Under Article 10 of this agreement, Indian employees can reduce the withholding tax on US dividend income from 30% to 25%. For this, they must submit the W-8BEN form with their foreign broker holding their vested shares before the dividend is credited.

In India, employees can claim the Foreign Tax Credit (FTC) on that dividend income by filing Form 67 before submitting their ITR.

What is the Capital Gains Tax on Selling Foreign RSUs?

While your employer handles the tax at vesting, the second tax event, i.e., the sale of the shares, is entirely your responsibility. Any appreciation in the stock's value between the vesting date and the sale date is considered a capital gain. It is important to remember that for capital gains purposes, your "cost of acquisition" is the FMV on which you already paid perquisite tax. This prevents double taxation of the grant's original value.

Following the changes in Budget 2024, the rates for these gains have been streamlined. Because foreign shares are not listed on Indian exchanges, they are classified as unlisted assets under Indian law. This means they do not qualify for the ₹1.25 lakh LTCG exemption for domestic stocks. The tax rate you pay depends solely on how long you've held the shares after they've vested.

The Impact of Stock Splits on your RSUs

A split is not a taxable event in the eyes of the government. Since it is simply a recalibration of your holdings, while the number of shares you own might increase (e.g., a 10-for-1 split), the per-share cost of acquisition is proportionally reduced by the same factor.

When you eventually decide to sell these split shares, the tax department looks back to your original vesting date to determine your holding period. This is a crucial distinction, as it ensures that a corporate action, such as a split, doesn't reset the clock on your transition from short-term to long-term capital gains status.

How Do You Calculate RSU Taxes?

Let’s understand the above tax implications of foreign RSUs with an example.

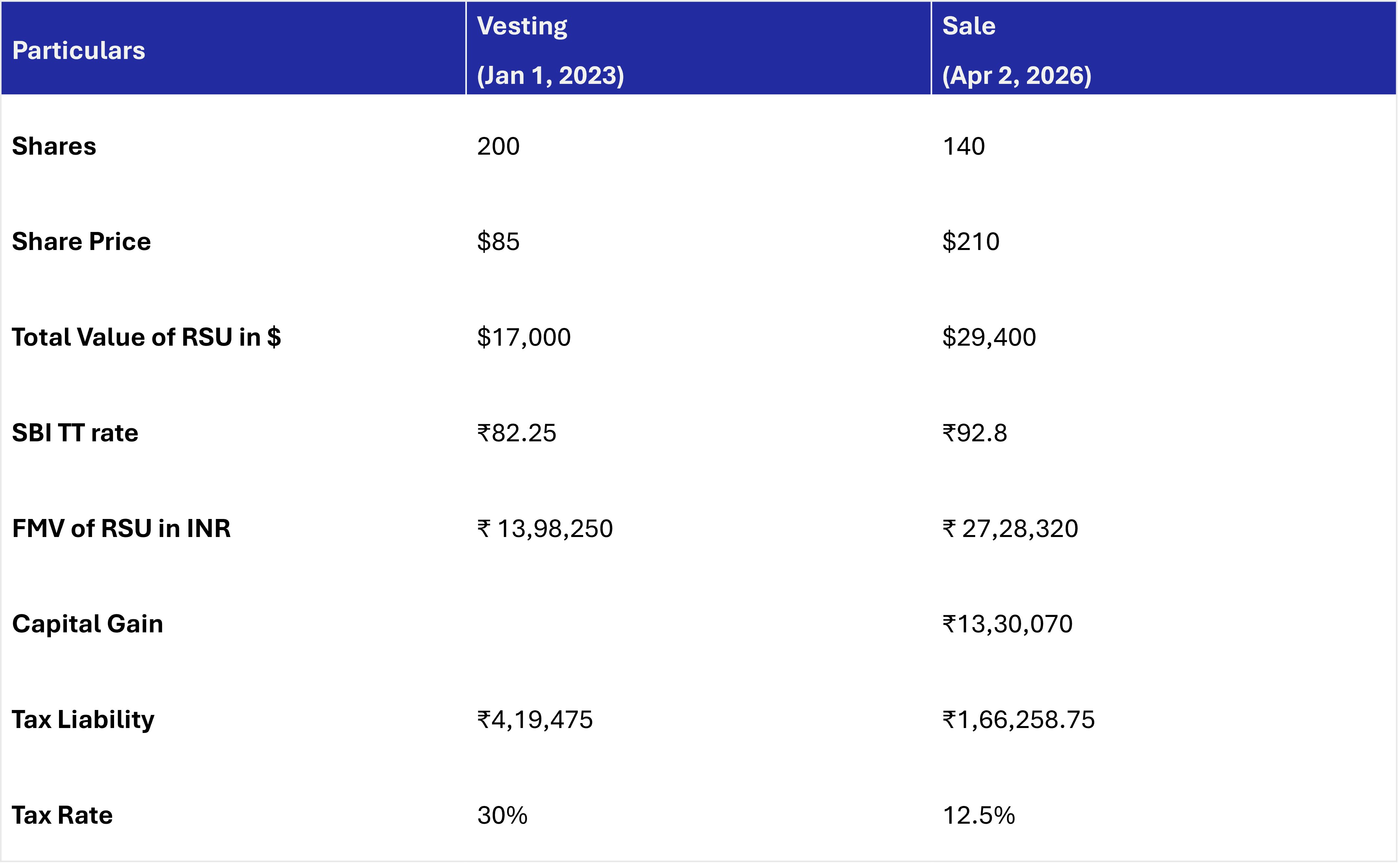

An Indian employee X joins Amazon in January 2020 and is granted 10 shares. Amazon announced a 20-for-1 stock split on June 6, 2022. X vested 200 shares (after split) at $85/share on January 1, 2023, and later sold them on April 2, 2026, at $210/share. No dividends or stock split were announced during the holding period.

Step 1: Vesting – Salary Income – Tax Slab

Total value of RSU: 200 x $85 = $17,000

Converted into INR at SBI TT rate of ₹82.25 = ₹13,98,250

This amount is added to Income from Salary. If the employee is in the highest tax slab of 30%.

Tax liability on vested shares = ₹4,19,475 (₹13,98,250 x 30%)

The employer pays this tax by selling 60 RSU shares and transferring the remaining 140 shares to X.

Step 2: Sale – Capital Gain tax

FMV = 140 x $210 = $29,400

Converted into INR at SBI TT rate of ₹92.8 = ₹27,28,320

Capital gain = ₹13,30,070 (₹27,28,320 - ₹13,98,250)

Since the holding period was more than 24 months, LTCG of 12.5% will apply.

Tax liability on share sale = ₹1,66,258.75 (₹13,30,070 x 12.5%)

This amount is paid by the employee.

When Are Advance Tax Provisions Applicable For RSU Holdings, and What Are The Penalties?

While your employer covers the "income" portion of the tax through TDS, you are responsible for the "growth" portion. If your realised capital gains from a share sale create a tax liability exceeding ₹10,000, you must pay this in quarterly advance tax instalments. Failure to do so can result in a significant tax when you file your ITR, as the government levies penal interest under Sections 234B and 234C of Income Tax Act 1961 and Section 424 and Section 425 of the new Income Tax Act 2025 applicable for filings in FY26-27.

Managing this liquidity is a critical part of financial planning for RSU holders. High-net-worth individuals must track their sales throughout the year and ensure that 15% of the tax is paid by 15th June, 45% by 15th September, 75% by 15th December, and 100% by 15th March. If you miss these windows, you'll be charged 1% interest per month, which can quickly erode the gains you've worked hard to accumulate.

Do I need to bring the Sale Proceeds from RSUs back to India under FEMA rules?

Holding your wealth in a foreign brokerage account after a sale might feel like a smart diversification strategy, but you must remain compliant with the RBI's FEMA guidelines. Indian residents are generally required to repatriate proceeds from the sale of foreign RSUs into an Indian bank account within 180 days. This rule ensures that foreign exchange earned by residents is brought back into the domestic economy. The only common exception is if you utilise a permissible Resident Foreign Currency (RFC) account or reinvest the proceeds in permissible overseas investments.

Hardik Mehta, Lead Tax Consultant at Ionic, says, “By keeping the sales proceeds from US assets in an offshore bank account or a GIFT City account, investors can preserve their annual $250,000 LRS allowance and avoid the 20% TCS that would apply if the funds entered India and had to be remitted outward again.”

Do I Need to Declare RSUs in My ITR Schedule FA?

The most critical reporting obligation for RSU holders is the mandatory disclosure in Schedule FA (Foreign Assets). Regardless of whether you have sold any shares or earned a single rupee in gains, you must disclose every foreign share you hold or vested during the relevant period. This reporting follows the calendar year (January to December), which often catches taxpayers off guard as it differs from the Indian financial year.

The consequences of non-disclosure are severe. Under the Black Money (Undisclosed Foreign Income and Assets) Act, 2015, failure to report these assets can attract a flat penalty of ₹10 lakh per year of omission, even if the money was earned through a legitimate salary. Treating Schedule FA as an afterthought is a dangerous mistake; it is a mandatory transparency requirement that carries more weight than the tax liability itself.

FAQs

Are unvested RSUs taxed in India?

No, unvested RSUs do not trigger any tax liability because they represent a future commitment rather than a current asset you control. Taxation in India is strictly performance-based at the point of vesting, which is when the company actually transfers the shares to your name at zero out-of-pocket cost. Until that specific date passes and you meet the employment terms, you aren't "earning" the income in the eyes of the tax department.

How do I avoid double taxation if the US withholds tax on my RSUs?

You can effectively eliminate double taxation by utilising the Foreign Tax Credit (FTC) mechanism under Section 90 of the Income Tax Act 1961 and Section 159 of the Income Tax Act 2025. When your US broker withholds tax on dividends or vesting, you must file Form 67 on the Indian income tax portal to declare these foreign taxes paid.

What happens to my RSUs if I resign?

Unvested RSUs are typically forfeited the moment you resign, as they are designed to incentivise your stay in the organisation. However, any RSUs that have already vested are your legal property. You are free to keep them in your foreign brokerage account or sell them, though you must remember that your reporting obligations for these foreign assets in Schedule FA continue as long as you hold them.

Can I carry forward losses if I sell my RSUs at a lower price?

Yes, the Indian tax system allows you to turn a market dip into a future tax shield. If you sell your RSUs for less than their FMV at vesting, you incur a capital loss that can be carried forward for 8 assessment years. Short-term capital losses (from shares held less than 24 months) can offset both short-term and long-term gains, while long-term capital losses can only offset long-term gains, providing a way to manage your overall portfolio tax liability during volatile years.

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

How to Evaluate a PMS Fund Manager: 10 Due Diligence Questio...

Ionic Wealth Tax Team on 3 Aug 2026

Selecting a PMS manager demands scrutiny beyond trailing returns—covering active share, style drift, skin in the game, capacity limits, and tax-adjusted alpha. With SEBI's proposed MF-PMS...

BOJ Holds Rates At 1.0%, Future Policy Tightening Likely

Ionic Wealth Macro Desk on 3 Aug 2026

BOJ held rates at 1.0% (8:1 vote) while upgrading growth forecasts and flagging inflation above 2% in H2 FY26. Persistent yen weakness, not inflation, remains the stronger catalyst for fu...

Post-Vesting Holding Period: Tax Impact of Holding vs Sellin...

Ionic Wealth Tax Team on 31 Jul 2026

Holding foreign RSUs past vesting means navigating FIFO-based capital gains, Budget 2024's flat 12.5% LTCG rate, and DRIP-fractured holding periods. Executives must also track OPI/FEMA di...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved