How to file a loved one’s tax after they die

This guide clarifies the essential steps and responsibilities for filing the final tax returns of a deceased loved one, ensuring compliance and smooth estate settlement.

Key Takeaways

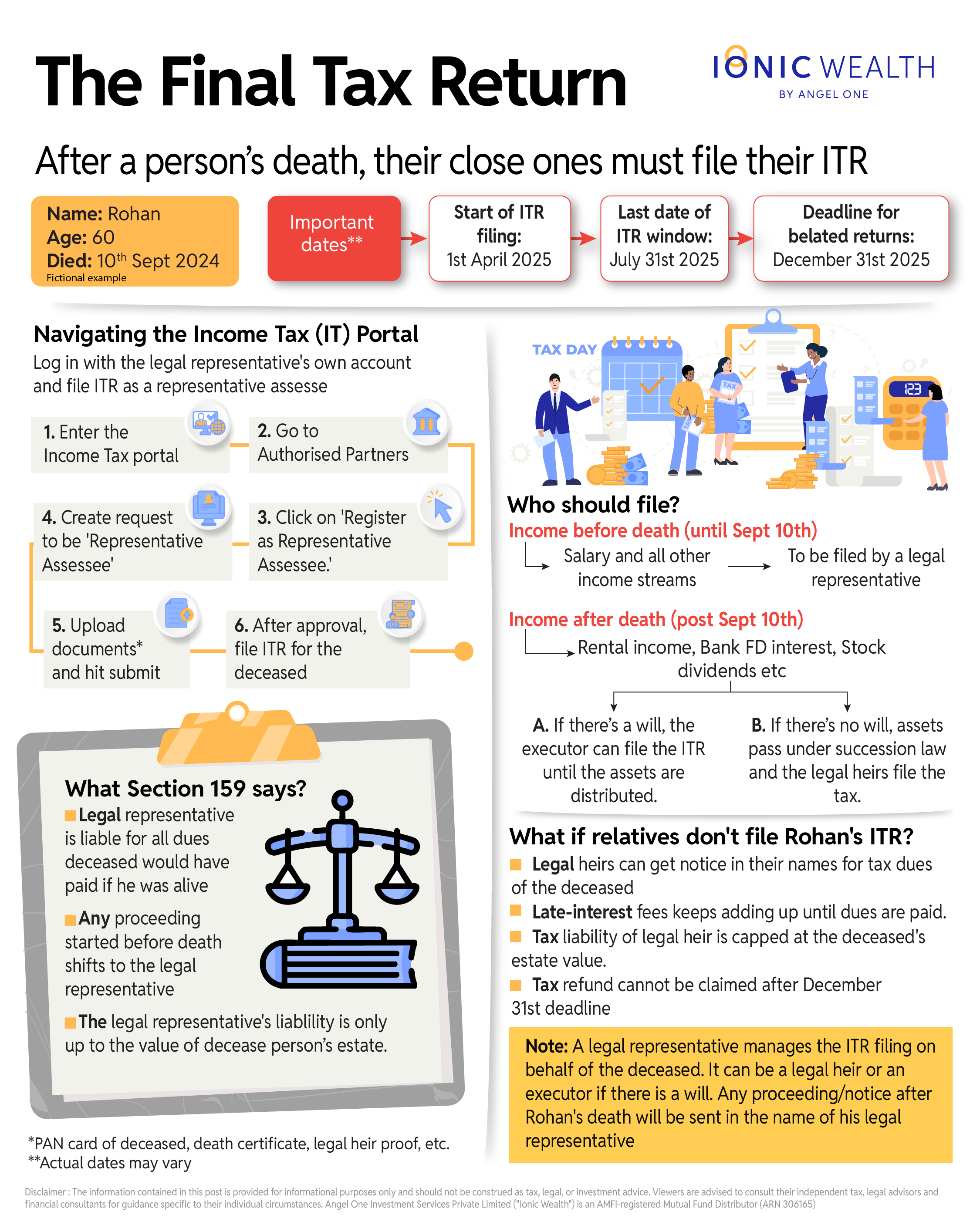

- As per Section 159 of the Income Tax Act, 1961, tax obligations do not cease upon death; a designated legal representative is responsible for filing the deceased's final tax return for income earned until their passing.

- A legal representative (spouse, child, executor) must register on the IT portal to file, managing income up to the date of death, while ongoing income (e.g., rent) after death is handled by the executor or inheriting heirs depending on the existence of a will.

- Failing to file within deadlines results in penalties, lost tax refunds, and potential tax department notices, underscoring the importance of timely action to prevent disputes and efficiently settle the deceased's financial affairs.

‘Nothing is certain except death and taxes’ - Benjamin Franklin, 1789

For many, this sentence rings a bell only after the tax department sends them a notice for failing to file tax returns on behalf of a family member who recently passed away.

As ironic as it sounds, Rohan’s family realised that it made perfect sense. He was earning a salary while he was alive, and the law clearly stated that his tax obligations don’t just disappear with his passing.

It’s a fair way of looking at things. Rohan might also have been eligible for a tax refund, and death shouldn’t stop his family from getting back that money.

So, here’s what we have today: A simple guide to filing a loved one’s final ITR. And what happened when Rohan’s family missed filing it!

Illustration

Let’s help Rohan’s family by breaking it down, step by step.

- What income must be reported in Rohan’s year end ITR?

- Who should be filing the ITR on his behalf?

- Who files tax on ongoing income (like rent) after his death?

The first part is straightforward. Section 159 of the Income Tax Act, 1961 says that there’s no running away from taxes.

In short, when a person dies, their legal representative becomes responsible for paying any tax, interest, or penalty that the deceased would have had to pay if they were still alive.

It also mentions that “any proceeding which could have been taken against the deceased if he had survived, may be taken against the legal representative.”

How to report

Before jumping in, let’s first divide Rohan’s income into two buckets: the income that he was earning until his death and the other part: rental and other income that continues even after his death.

For the income earned before passing, a legal representative must file the ITR on behalf of Rohan.

Relax — Rohan’s IT portal login isn’t required.

For starters, a legal representative is a person who represents the assets of the deceased in his absence. They can be his spouse, children, close relative or executor of the will.

They are responsible for managing things like tax filing and other tax matters for the deceased. Note that it’s not the same as a legal heir who inherits the property of the deceased although a person can be both a legal representative and a legal heir.

One can apply to be a legal representative through the Income Tax (IT) portal. They can do this by logging to their own IT portal and submitting an application.

You can follow the steps here.

After submitting the request, it takes around 7 days for the Centralized Processing Centre (CPC) to approve it.

Once that’s done, the legal representative of the deceased can file the tax return on behalf of the deceased. It’s same as filing a normal IT return, just that you’re filing on behalf of the deceased.

The legal representative must file two separate returns that year — one for the deceased and one for themselves.

But you might be thinking: What happens to the income that continues even after death? Things like rental income from a real estate property or interest from bank fixed deposits.

Two things can happen here. If Rohan left behind a will, the executor is responsible for filing the tax returns until the assets are eventually distributed to the legal heirs.

On the other hand, if Rohan died interstate i.e. without a will, then his assets will first be divided as per the applicable succession law. Whoever inherits the property will report and pay tax on it using their own PAN.

Forgot to file. What happens?

Let’s say our imaginary character Rohan died in a car crash on 10th September 2024. Ideally, his ITR should have been filed in the normal tax window i.e. from 1st April 2025 to 31st July 2025.

If that wasn’t done, the last date for filing belated returns is 31st December 2025 albeit with a penalty and interest for late filing.

We should not be missing this deadline.

After December 31st, 2025:

- The IT portal will no longer have the option of filing ITR.

- Tax refund cannot be claimed even if Rohan has paid excess TDS.

- The assessing officer can send notice to inquire on the non-filing of the ITR.

To be sure, while the notice can be served to the legal representative on behalf of the deceased, the total tax liability is limited to the estate of the deceased.

For instance, if the deceased had a tax liability of one crore rupees but left behind Rs 80 lakh in assets, then only Rs 80 lakh can recovered.

Beware: Interest keeps accumulating every month until the outstanding tax is fully paid.

What should you do?

Handling tax matters after someone’s death is sensitive but essential. Timely action ensures that the deceased’s affairs are settled smoothly and without future disputes.

The first step is identifying who will take responsibility - the legal representative or executor and registering them so that they can act on behalf of the deceased.

Next, the income up to the date of death must be reported in the final return, filed within the applicable timelines to avoid any loss of eligible tax benefits.

Where income continues to accrue from the estate, the person in charge must ensure taxes are correctly handled until the assets are transferred to the rightful beneficiaries.

And finally, responding promptly to any communication from the tax department safeguards the family from avoidable disputes later.

While the tax rules may seem complex, a little preparation can ensure that fulfilling these obligations becomes just another way of honouring the legacy of those we love.

***

Rohan’s example is hypothetical.

With inputs from Hardik Mehta, Lead Tax at Ionic Wealth

Disclaimer

This material is for general information and guidance only. While efforts have been made to present accurate and useful information, it may not be complete or reflect the most current developments. Readers are advised to consult a qualified tax or legal advisor before relying on this information. Any examples or illustrations are purely for explanation, and any persons referenced are fictitious. We are not responsible for any decisions made based on this publication.

Angel One Investment Services Private Limited (“Ionic Wealth”) is an AMFI - Registered Mutual Fund Distributors with ARN – 306165 and a SEBI Registered Research Analyst with Reg. no. INH000020305. Mutual Funds are subject to market risk. Read all the scheme related documents carefully before investing.

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

How to Evaluate a PMS Fund Manager: 10 Due Diligence Questio...

Ionic Wealth Tax Team on 3 Aug 2026

Selecting a PMS manager demands scrutiny beyond trailing returns—covering active share, style drift, skin in the game, capacity limits, and tax-adjusted alpha. With SEBI's proposed MF-PMS...

BOJ Holds Rates At 1.0%, Future Policy Tightening Likely

Ionic Wealth Macro Desk on 3 Aug 2026

BOJ held rates at 1.0% (8:1 vote) while upgrading growth forecasts and flagging inflation above 2% in H2 FY26. Persistent yen weakness, not inflation, remains the stronger catalyst for fu...

Post-Vesting Holding Period: Tax Impact of Holding vs Sellin...

Ionic Wealth Tax Team on 31 Jul 2026

Holding foreign RSUs past vesting means navigating FIFO-based capital gains, Budget 2024's flat 12.5% LTCG rate, and DRIP-fractured holding periods. Executives must also track OPI/FEMA di...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved