Have Foreign ESOPs? Make sure you don't get penalised

High-net-worth individuals with foreign Employee Stock Option Plans (ESOPs) must ensure meticulous tax disclosure to avoid significant penalties under Indian law.

Key Takeaways

- Failure to disclose foreign assets, including ESOPs, can incur a Rs 10 lakh penalty under The Black Money Act, 2015, even if taxes were paid.

- Common errors include omitting disclosure of exercised shares (even if tax deducted), shares sold to pay tax, foreign dividends, and not claiming credit for foreign taxes paid via Form 67.

- Foreign asset reporting is complex—involving specific schedules (FA, FSI, TR), calendar year reporting for foreign assets versus financial year for Indian income, and varied ITR forms—necessitating consultation with qualified tax professionals.

.png&w=3840&q=75)

A few months ago, the income tax department sent out an advisory via email to employees of multinational companies.

They had stock options of the foreign entity, and the taxman’s message was clear: Don’t forget to disclose if you got any foreign assets, including stock options.

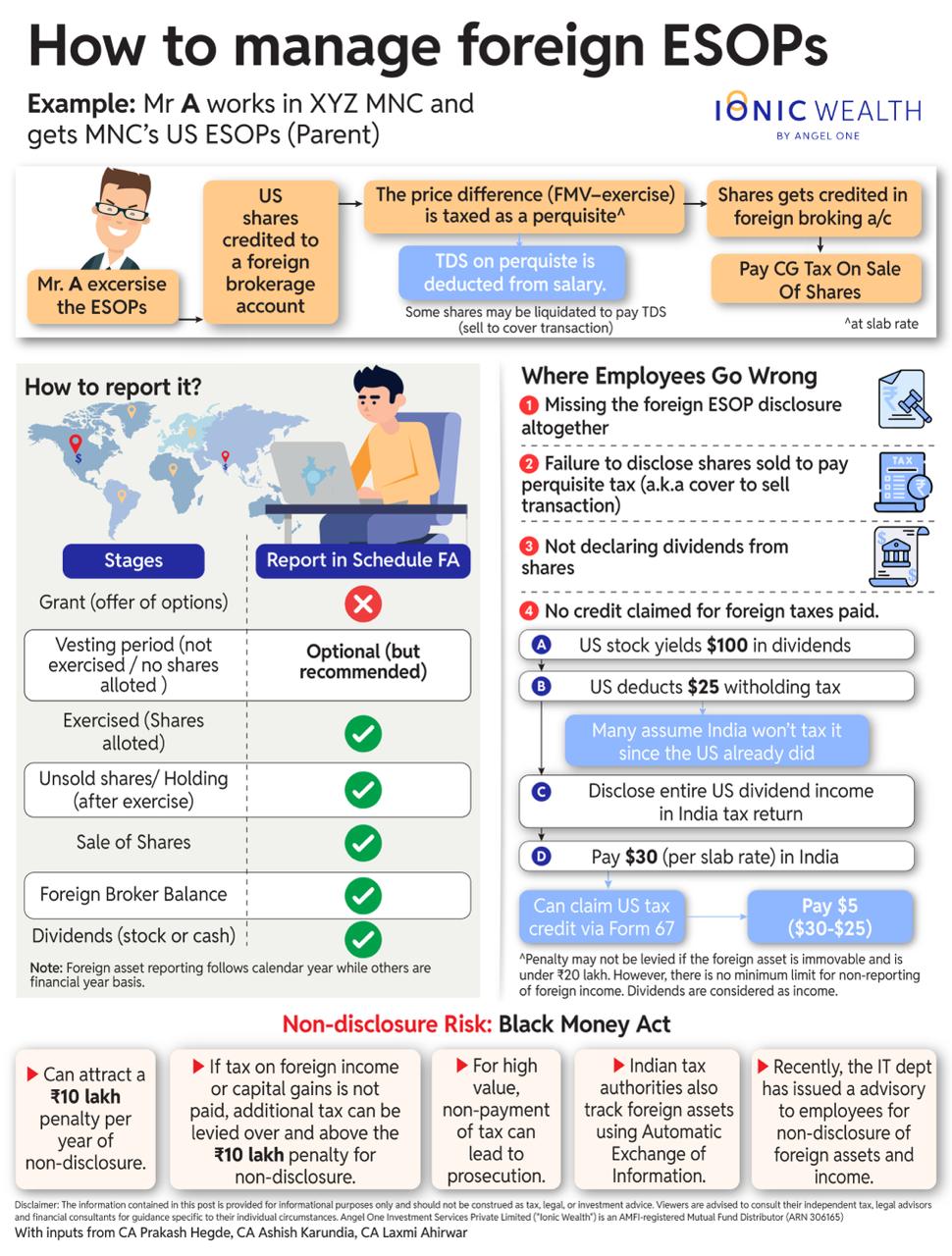

For starters, it is not uncommon for foreign companies that have a base in India to offer employee stock option plans (ESOPs). The tricky part comes when the underlying stock option is in a foreign entity.

There is a Rs 10 lakh penalty under The Black Money Act, 2015, if you fail to report foreign assets or income in your ITR.

Unlike listed Indian shares, foreign assets have strict disclosure requirements. Holding foreign shares requires voluntary disclosure in the Schedule Foreign Assets (Schedule FA) in the income tax filings.

Prakash Hegde, a chartered accountant based in Bangalore, said that if the taxpayer is found not to have paid tax from a foreign source at all, then a higher tax can be applied in addition to the Rs 10 lakh fine for non-disclosure.

“Note that even if tax was paid, disclosure is mandatory for foreign assets and income,” added Hegde.

For context, Indian authorities use various sources, including Automatic Exchange of Information (AEI) agreements with other countries, to find out assets that Indians hold abroad.

With India being an important commercial hub, many senior executives are now working in foreign companies and have foreign ESOPs. Hence, we have compiled a list of common mistakes that such people make.

The list was compiled with the help of 3 chartered accountants who have extensively worked with employees holding foreign ESOPs: Prakash Hegde, a Bengaluru-based CA; Ashish Karundia, CA firm Ashish Karundia & Co., and Laxmi Ahirwar, CA and Director, P. R. Bhuta & Co.

Missing foreign disclosure altogether

Many people fail to disclose that they have foreign shares altogether. On exercise of foreign ESOPs, the shares come to a foreign brokerage account created by the employer. Since the account was not opened by them, it’s no surprise that quite a lot of people skip reporting it in their ITR.

Tax was also deducted when the ESOPs were exercised. When the stock options are exercised, the difference between the exercise price and fair value at the time of exercise is taxed as a perquisite (like salary) at the slab rate.

CA Ashish Karundia said that the onus is on the company to deduct the tax on exercise, but the onus of reporting it is with the employees getting those shares.

He said that many people assume that since tax was already paid to Indian authorities, a separate disclosure is not required. However, paying tax does not mean they should not disclose those assets.

Not disclosing shares sold during exercise

As mentioned above, when ESOPs are exercised, perquisite tax is taken on the difference between the exercise price and the fair market value at the time of exercise. But this might be a huge amount, and the employee has yet to receive any cash in hand. So how does one pay this tax?

Many companies sell a part of the shares immediately after the shares are credited to the employer’s brokerage account. The employer transfers this amount from the foreign brokerage account to the Indian subsidiary, which in turn pays the amount as perquisite tax to the IT department on behalf of the employee.

So what’s the problem? Hegde said that many people report only the shares left in their account and often forget to report those shares that were sold to pay tax.

The risk is that the IT department can get the details of the shares sold overseas. But without disclosure of those foreign assets, the IT dept might think that this amount has escaped from capital gains taxation. In reality, since the shares are credited and sold on the exercise day itself, the difference between the cost price and the selling price would be minimal and thus result in minimal capital gains tax.

“They should disclose both the cost price and the selling price; this will make it clear. Otherwise, the IT dept might treat this income as escaping taxation,” added Hegde.

Not disclosing dividends

After the shares get credited to the account, some stocks might give out dividends. Many employees forget to report such dividends as income from a foreign source in their ITR. In the last budget, it was mentioned that if a foreign asset (other than immovable) was not disclosed and the value is below Rs 20 lakh, then a penalty may not be applied.

That said, there is no threshold defined for levying a penalty for non-disclosure of income. And dividends are part of income from foreign sources.

Not claiming credit for taxes paid in a foreign country

Some incomes are taxed both in India and abroad, but many don’t claim credit in India for the tax paid abroad. For instance, dividends from US stocks attract a 25% withholding tax. If you get $100 as dividends from US stocks, they will deduct $25 and pay out $75.

Even then, the entire $100 needs to be again declared for tax in India. If the person was under the 30% slab rate, then a $30 tax would be applicable in India. However, they can submit Form 67 in their ITR and get credit for the $25 already paid in the US.

“This also needs to be reported in Schedule FSI (Foreign source income), Schedule TR (Tax Relief) and Form 1042-S (issued by foreign broker and includes tax deducted). By doing this, they only have to pay $5 ($30-$25),” said Laxmi Lahiwar, CA and Director, P. R. Bhuta & Co.

“If the foreign country’s tax was more than India’s, then that extra amount is a deadweight loss,” added Ahiwar.

Ionic’s view: What should you do?

Hardik Mehta, tax lead at Ionic Wealth, recommends that high-net-worth individuals with foreign ESOPs familiarise themselves with the basics of foreign asset reporting in India. “It also helps to keep proper records of all transactions that happened with the foreign assets for future reference incase any dispute arises.”

However, he said that foreign asset disclosure is not an easy task and requires domain expertise. For instance, while income from India follows the financial year for tax purposes, foreign asset reporting is done based on the calendar year.

The proper way of reporting and which ITR forms to choose for reporting also varies for different foreign assets. Also, not just the buy and sell price, but the peak value of the foreign assets in the year might be required to be reported for certain foreign assets.

There can also be other complications. If the employee gets US shares via ESOPs but then passes away for any reason, then 40% estate tax might be applicable beyond $60,000.

We recommend consulting a qualified tax professional to avoid getting into trouble and to avoid heavy penalties under the Black Money Act. Consulting an investment advisor on whether to hold, sell or diversify the shares you got through the ESOPs is another part of the puzzle.

Also Read: How ESOPs works

Disclaimer

This material is for general information and guidance only. While efforts have been made to present accurate and useful information, it may not be complete or reflect the most current developments. Readers are advised to consult a qualified tax or legal advisor before relying on this information. Any examples or illustrations are purely for explanation, and any persons referenced are fictitious. We are not responsible for any decisions made based on this publication.

Angel One Investment Services Private Limited (“Ionic Wealth”) is an AMFI - Registered Mutual Fund Distributors with ARN – 306165 and a SEBI Registered Research Analyst with Reg. no. INH000020305. Mutual Funds are subject to market risk. Read all the scheme related documents carefully before investing.

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

How to Evaluate a PMS Fund Manager: 10 Due Diligence Questio...

Ionic Wealth Tax Team on 3 Aug 2026

Selecting a PMS manager demands scrutiny beyond trailing returns—covering active share, style drift, skin in the game, capacity limits, and tax-adjusted alpha. With SEBI's proposed MF-PMS...

BOJ Holds Rates At 1.0%, Future Policy Tightening Likely

Ionic Wealth Macro Desk on 3 Aug 2026

BOJ held rates at 1.0% (8:1 vote) while upgrading growth forecasts and flagging inflation above 2% in H2 FY26. Persistent yen weakness, not inflation, remains the stronger catalyst for fu...

Post-Vesting Holding Period: Tax Impact of Holding vs Sellin...

Ionic Wealth Tax Team on 31 Jul 2026

Holding foreign RSUs past vesting means navigating FIFO-based capital gains, Budget 2024's flat 12.5% LTCG rate, and DRIP-fractured holding periods. Executives must also track OPI/FEMA di...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved