China's Agent Inflection: Why Enterprise Deployment Is the New Cloud Frontier

From selling compute to selling intelligence: China's hyperscalers are no longer fighting on price

China's cloud market continues to compound — mainland infrastructure services spending reached $14.7 billion in Q4 2025, up 26% YoY, the third consecutive quarter above 20%, with another 26% gain projected for 2026. The just-reported March quarter results extend the trend at the high end: Alibaba Cloud's external revenue accelerated to +40% YoY, while Baidu's AI Cloud Infra surged +79% YoY, with its GPU Cloud business up +184%

AI remains the key driver, but the engine has shifted. Demand is moving decisively beyond raw model usage toward agent-based products that plug into real enterprise workflows. The emergence of OpenClaw in China has accelerated this transition, demonstrating how agents can be delivered in formats that map naturally to how businesses actually operate.

For the first time in years, China's hyperscalers have real pricing power. Alibaba hiked AI compute prices by 5–34%, Baidu raised AI cloud prices by 5–30%, Tencent added 5% between March and May 2026 — synchronized hikes that formally end the multi-year price-war cycle, as agent workloads consume capacity faster than the industry can build it. Additionally, the shift towards Model-as-a-Service — where API-call monetization, which carries structurally higher margins than commodity infrastructure, is driving cloud margin expansion.

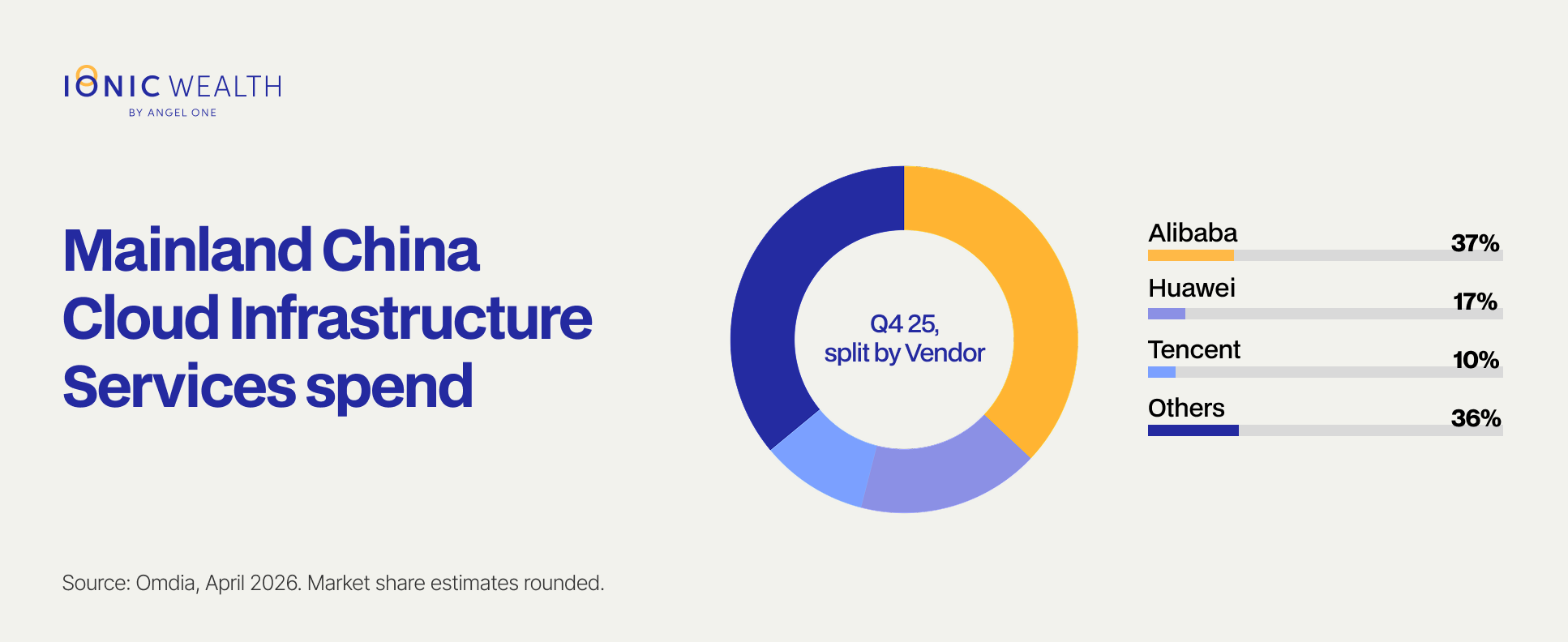

Each vendor owns a distinct slice. Tencent Cloud holds the consumer interface — chat-based agent gateways through WeChat and QQ, layered into its gaming and content ecosystems. Alibaba Cloud leads enterprise workflows with Wukong, its DingTalk-native answer to OpenClaw. Baidu is pushing its Ernie models, Qianfan MaaS, and Kunlun chips, while Huawei Cloud continues to win in vertical industry deployments

Ionic View

In our view, China's cloud market is exiting its model-experimentation, price-war phase and entering a structurally healthier growth-and-margin regime, driven by enterprise-scale agent deployment. The key beneficiaries are likely to be platforms with strong enterprise ecosystems, distribution advantages, and integrated deployment capabilities like Tencent and Alibaba. The price hikes suggest that the shift from 'selling compute to selling intelligence' could be structurally lifting cloud margins. These price increases are not driven by rising costs, but by sustained improvements in model performance, and the expanding API gross margins confirm that the market is transitioning from pure commoditization toward performance-based monetization.

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

How to Evaluate a PMS Fund Manager: 10 Due Diligence Questio...

Ionic Wealth Tax Team on 3 Aug 2026

Selecting a PMS manager demands scrutiny beyond trailing returns—covering active share, style drift, skin in the game, capacity limits, and tax-adjusted alpha. With SEBI's proposed MF-PMS...

BOJ Holds Rates At 1.0%, Future Policy Tightening Likely

Ionic Wealth Macro Desk on 3 Aug 2026

BOJ held rates at 1.0% (8:1 vote) while upgrading growth forecasts and flagging inflation above 2% in H2 FY26. Persistent yen weakness, not inflation, remains the stronger catalyst for fu...

Post-Vesting Holding Period: Tax Impact of Holding vs Sellin...

Ionic Wealth Tax Team on 31 Jul 2026

Holding foreign RSUs past vesting means navigating FIFO-based capital gains, Budget 2024's flat 12.5% LTCG rate, and DRIP-fractured holding periods. Executives must also track OPI/FEMA di...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved