Startup ESOP Guide: Valuation, Exercise Window & Taxation

Key Takeaways

• The tax liability for ESOPs is triggered at the moment of exercise based on the Fair Market Value (FMV) certified by a merchant banker, not when the shares are eventually sold or listed.

• Departing employees often face a severe liquidity trap, as they must pay both the strike price and the perquisite tax upfront for shares that cannot yet be sold.

• Tax deferral benefits are available for employees of DPIIT-recognized startups, allowing them to postpone perquisite tax payments until a sale, resignation, or a specific four-year limit.

• Secondary sales of shares held for more than 24 months qualify for long-term capital gains, and standard capital gains rules under Section 198 of the Income Tax Act 2025 apply.

Most startup employees treat employee stock options (ESOPs) like a lottery ticket.

The general idea is to hold stock options until the company goes public or is acquired, and then cash out. However, the reality is far more complicated than that.

The tax clock starts ticking the moment you exercise your options, not when you sell or when the company lists.

And if you hold equity in an unlisted startup, you face a uniquely painful problem: you owe tax on shares you cannot sell on any public exchange.

This guide breaks down how ESOP taxation works for startups in India. It covers valuation rules, exercise windows, liquidity events, and the planning strategies that help you avoid costly surprises.

What Determines the Valuation of My Unlisted Startup ESOPs?

With a listed company, you check the stock exchange for the latest price. With a private startup, no such price exists. So, how does the government determine the value of your shares for tax purposes?

For a private startup, no such public price exists, so the valuation for tax purposes follows a strictly regulated process.

The Income Tax Act, 2025 provides a specific framework for this under Section 16(2)(vi). It mandates that companies obtain a Fair Market Value (FMV) certificate exclusively from a SEBI-registered Category I Merchant Banker. This certificate is often provided by the same investment bank that advised the company during its most recent funding round.

The merchant banker determines the FMV using a blend of sophisticated methodologies:

• Discounted Free Cash Flow (DCF): Projections of the company’s future earning potential.

• Comparable Company Multiples: Benchmarking against similar firms in the industry.

• Recent Transaction Prices: Factoring in the price per share from the latest Series round.

That certificate is valid for exactly 180 days. If you exercise options during that window, your perquisite tax is calculated using the FMV from that certificate. If you exercise after the 180 days has expired, the company needs a fresh valuation. The timing of your decision can therefore make a real difference to what you owe.

It is also worth noting that under Section 392 of ITA 2025, the employer is still responsible for deducting TDS at the employee's applicable slab rate at the time of exercise, unless the startup is eligible for the deferral under Section 108 of ITA 2025.

How Does the 90-Day Exercise Window Trap Departing Employees?

Leaving a startup is already stressful. The Employee Stock Option Plan (ESOP) clock makes it considerably worse.

While the duration of the exercise period following a resignation is governed strictly by your specific ESOP plan document and is not a legally fixed timeframe. Most ESOP plans give departing employees 90 days from their last working day to exercise vested options. After that window closes, those options are gone forever.

This creates a serious cash flow problem. At the moment of leaving, you must come up with two separate payments at the same time.

First, you pay the company the strike price to actually buy the shares. Second, because the exercise triggers a perquisite tax, your employer will deduct tax deducted at source (TDS) from your final paycheck or severance. In a high-value grant, that combined cash outflow can run into lakhs.

The most painful part is that you are buying shares in a company you have just left, shares you cannot sell on a public exchange. You are paying real cash for an asset with no immediate liquidity, under a tight deadline, at a potentially high tax cost.

Many departing employees simply walk away from vested equity because they cannot arrange the funds in time.

(Note: Several prominent Indian startups, including Flipkart, Razorpay, and Swiggy, have moved away from this restrictive window, offering extended periods or even "lifetime" exercise rights for vested options. It is always a good practice to check the ESOP offer document to see what the exercise window that is applicable for you in case of resignation)

What Are the Tax Implications of Selling ESOPs in a Company-Sponsored Liquidity Event?

For most startup employees, a company-run buyback or secondary sale is the only realistic way to turn ESOPs into actual cash. But the tax treatment depends heavily on how the transaction is structured under the Income Tax Act, 2025.

If the company conducts a formal buyback of shares of the employees, the net proceeds are treated as capital gains.

Further, if the company arranges a secondary transfer directly to a new private equity investor, standard capital gains rules under Section 198 of the Income Tax Act 2025 apply. You are essentially selling shares to a third party rather than the issuing company itself.

So if you have held the shares for more than 24 months since your exercise date, you pay long-term capital gains tax at a flat 12.5%. Under 24 months, short-term gains are taxed at your regular income tax slab rate.

How Does a Down Round Affect My Vested ESOPs?

Not every funding round goes upward. Startups sometimes raise money at a lower valuation than their previous round. This is called a down round, and it directly impacts the value of your options.

Soon after a down round, the merchant banker issues a new FMV certificate at the lower price. If that new FMV falls below your original strike price, your options become what the industry calls "underwater."

What does underwater mean in plain terms? You would spend more cash buying the shares than those shares are currently worth. Exercising in that situation is financially irrational.

The only scenario where it might make sense is if you have a very high conviction that the company will recover significantly before your options expire or before you plan to leave.

During market downturns, several well-known startups saw down rounds that left early employees with vested options worth far less than their strike price. Recognizing this early gives you time to plan rather than react under pressure.

Real-World Example: Calculating the Tax Hit on a Series B Exercise

Consider an early employee who decides to exercise 2,000 vested options just after their company's Series B round closes.

The strike price is ₹100 per share. The merchant banker has certified a Fair Market Value of ₹1,100 per share on the exercise date.

Here is how the math breaks down:

The perquisite value per share is ₹1,000. That is simply the FMV minus the strike price. Across 2,000 shares, the total perquisite value is ₹20,00,000.

The employee writes a cheque to the company for ₹2,00,000 to cover the strike price. But that is actually the smaller payment.

The ₹20,00,000 perquisite value gets added to their annual salary for that financial year. Their employer deducts TDS accordingly. This often means a significant reduction in net salary in the month of exercise.

The employee now holds shares worth ₹22,00,000 on paper. But they have paid ₹2,00,000 in upfront cash and taken a large TDS hit on that month's salary.

The liquidity mismatch is real and frequently catches employees off guard the first time they exercise a high-value grant.

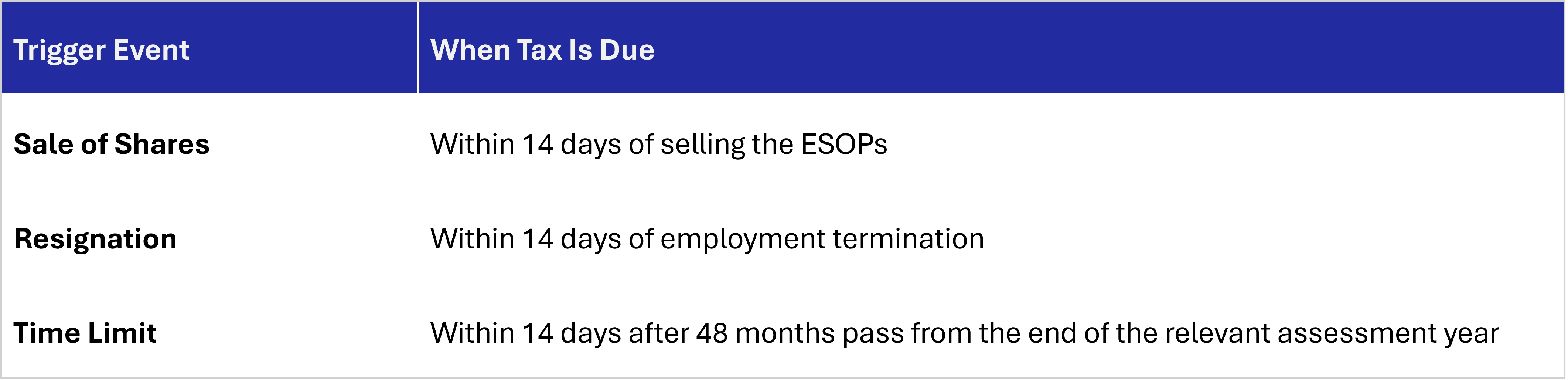

Can I Defer the Perquisite Tax if I Work for a DPIIT-Recognized Startup?

The government recognized this liquidity problem and created a specific relief for eligible startups.

If your employer holds an active recognition from the Department for Promotion of Industry and Internal Trade (DPIIT) and an IMB certification under Section 108 of Income Tax Act 2025, you do not have to pay perquisite tax at the time of exercise.

You can defer it, and the tax is payable only when one of three trigger events occurs.

This is a meaningful benefit.

Instead of paying tax on shares you cannot sell, you wait until you actually have liquidity from a sale or until you leave the company.

Check whether your employer holds current DPIIT recognition before exercising.

The recognition lapses and must be renewed, so an outdated certificate does not qualify you for the deferral.

Can I Use a Cashless Exercise for Unlisted Indian Startup Equity?

In the United States, many startup employees use cashless payment methods. They buy shares and immediately sell a portion to a broker to cover the strike price and taxes, which means that no upfront cash required.

It does not work the same way in India for unlisted startups.

A cashless exercise requires a buyer standing by to purchase the shares immediately. In a public market, a broker fills that role. In a private company, there is no such market.

For most Indian startup employees, a cashless exercise only becomes available during a structured liquidity event organized by the company itself. Think of a secondary sale or an acquisition. Outside of those windows, you need actual cash to exercise.

This is a common misconception, borrowed from the way US public-market equity compensation works. It is worth understanding clearly before you plan your exercise strategy.

Conclusion

The difference between a successful exit and a costly mistake often comes down to timing and tax planning. Before you sign an exercise notice, ensure you have a clear understanding of the current FMV, your available liquidity for tax payments, and the specific exit routes offered by your employer. By treating your equity with the same rigor as your salary, you can ensure that when the "lottery" finally hits, you aren't left with a tax bill you can't afford to pay.

FAQs

Can I negotiate the 90-day exercise window when I resign?

You can request an extended exercise window during your exit discussions, but the company board must formally approve the amendment to your specific grant agreement.

Are unvested ESOPs paid out if the startup gets acquired?

Acquirers typically cancel unvested options or convert them into the acquiring company's equity structure, depending entirely on the merger agreement terms.

Do I pay tax on ESOPs granted by a foreign parent company?

Yes, Indian residents pay perquisite tax and capital gains tax on foreign ESOPs, and you must report these assets in Schedule FA of your income tax return.

Can I offset my ESOP perquisite tax with capital losses?

You cannot offset perquisite tax with capital losses because the Income Tax Department classifies perquisite value as standard salary income.

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

How to Evaluate a PMS Fund Manager: 10 Due Diligence Questio...

Ionic Wealth Tax Team on 3 Aug 2026

Selecting a PMS manager demands scrutiny beyond trailing returns—covering active share, style drift, skin in the game, capacity limits, and tax-adjusted alpha. With SEBI's proposed MF-PMS...

BOJ Holds Rates At 1.0%, Future Policy Tightening Likely

Ionic Wealth Macro Desk on 3 Aug 2026

BOJ held rates at 1.0% (8:1 vote) while upgrading growth forecasts and flagging inflation above 2% in H2 FY26. Persistent yen weakness, not inflation, remains the stronger catalyst for fu...

Post-Vesting Holding Period: Tax Impact of Holding vs Sellin...

Ionic Wealth Tax Team on 31 Jul 2026

Holding foreign RSUs past vesting means navigating FIFO-based capital gains, Budget 2024's flat 12.5% LTCG rate, and DRIP-fractured holding periods. Executives must also track OPI/FEMA di...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved