Double Taxation on RSUs: How to Claim Relief Under DTAA

.png&w=3840&q=75)

Key Takeaways

• A Double Taxation Avoidance Agreement (DTAA) prevents Indian residents from being taxed twice on foreign income by allowing for tax exemptions or credits on foreign income including dividends and trailing tax liabilities from RSUs.

• Indian residents can reduce the standard US withholding tax on dividends from 30% to 25% by filing a Form W-8BEN with their foreign brokerage.

• To claim credit for taxes already paid abroad, you must file Form 67 on the Indian e-Filing portal on or before the end of relevant assessment year.

• Foreign income and taxes must be converted to INR using the SBI Telegraphic Transfer buying rate from the month preceding the payment to accurately calculate the Foreign Tax Credit.

The globalisation of business and investment has enabled individuals living and working in India to earn foreign income. Many Indian resident tech executives hold foreign Restricted Stock Units (RSUs) and face double taxation on cross-border dividend payments and trailing tax liabilities from international relocations.

A Double Taxation Avoidance Agreement (DTAA) prevents individuals from being taxed twice on the same income by two distinct national governments. It provides tax relief through:

• Exemption where income is taxed in only one country.

• Tax credit, where a credit is allowed for tax paid in one country.

If your foreign employer has deducted tax on RSU dividends, you can claim the Foreign Tax Credit (FTC) by filing Form 67 under Section 90 of the Income Tax Act. You must actively submit necessary forms and supporting documents to both parties - the foreign brokerage and the Indian Income Tax Department- or miss out on the credit.

Let’s understand the process to claim relief under DTAA.

How Does Double Taxation Actually Occur on Foreign Equity?

Taxation is determined by an individual’s residency status and the source of taxable income. When they are from different countries, double taxation might arises. The question of which national government should tax income can trigger cross-border tax conflicts in complex transactions.

In India, individuals classified as Resident and Ordinarily Resident (ROR) are taxed on worldwide income and are required to report their global assets. Thus, dividend income from foreign equity is taxable under the "Income from Other Sources" as global income in India.

For resident tech employees with vested foreign RSUs, double taxation typically occurs in two scenarios:

• First, when foreign governments withhold tax on dividends issued by the company's stock.

• Second, when the employee works in a foreign jurisdiction for a portion of the vesting period, relocates to India, and becomes an Indian resident. This leads to trailing tax liabilities as RSU income becomes taxable global income in India.

Which Major Countries Hold a DTAA With India for Equity Income?

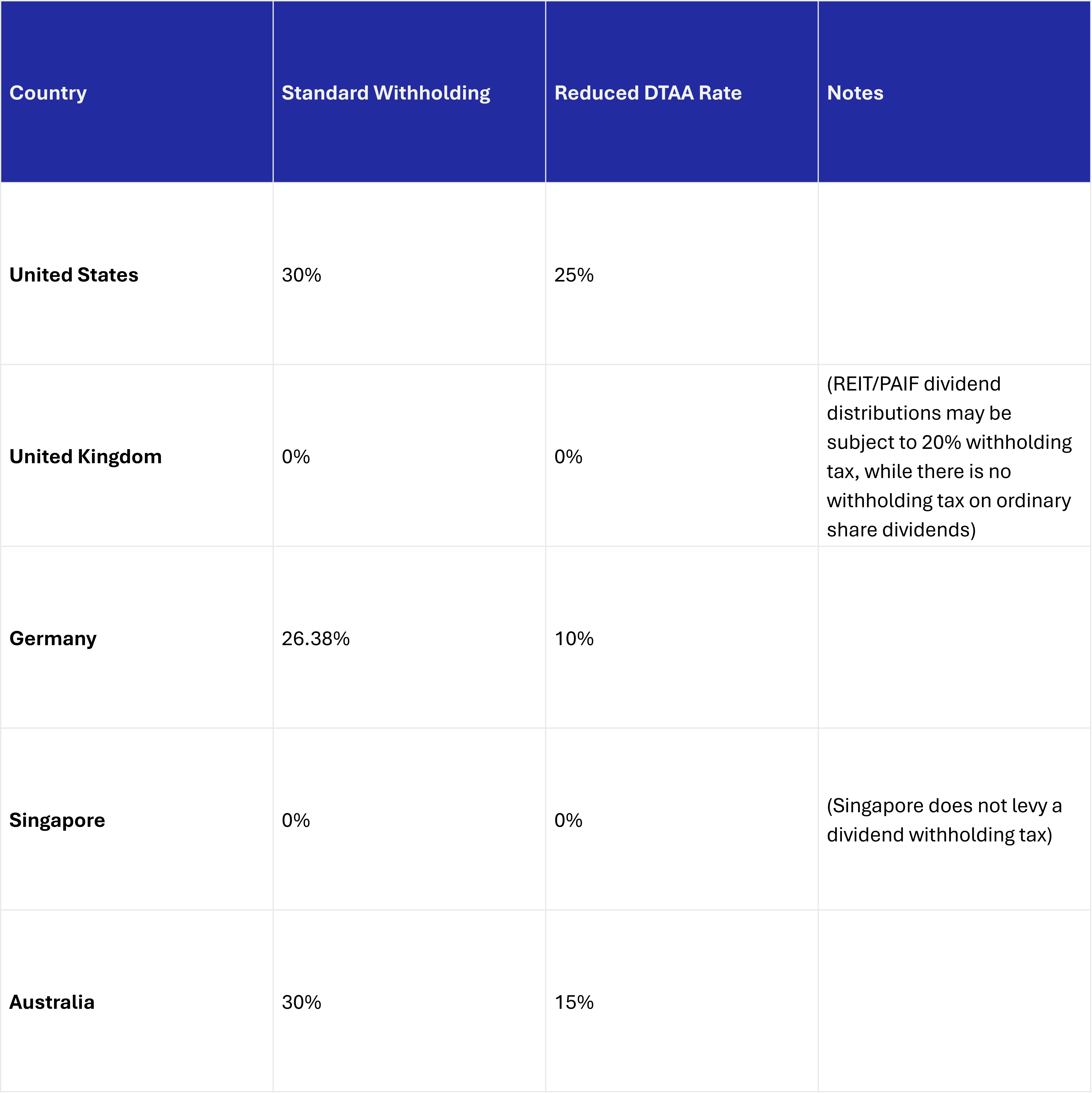

To ensure the same income is not taxed twice, India has signed a DTAA with 94 countries (Source: PWC report). One such agreement was signed between India and the United States on September 12, 1989, entered into force on December 18, 1990, with provisions generally effective from January 1, 1991. This treaty gives Indian residents earning a US income the benefit of a reduced tax rate for certain categories of income as agreed in the DTAA.

For instance, the US-sourced dividend income is subject to the standard 30% withholding tax. However, Article 10 of the India-US DTAA caps the US withholding rate at 25% for Indian residents.

DTAA Dividend Withholding Rates for Major Tech Hubs

To avail yourself of these reduced DTAA rates, you must proactively reach out to your foreign brokerage and prove your Indian tax residency. When you submit the necessary forms with correct documentation, the foreign brokerage will apply the lower treaty rate.

Why is the W-8BEN Form Critical for US Tech Employees?

If you are an Indian resident having RSUs of a US tech company, the W-8BEN Form is critical for you to claim a reduced DTAA rate. W8-BEN, in US Internal Revenue System (IRS) terms, is the “Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals)” The name W-8 BEN is a combination of the IRS category W-8 (which is an official form meant for non-US persons) and BEN (which is short for beneficiary)

The US Internal Revenue Service (IRS) will levy a default 30% withholding tax on all dividends paid to foreign persons. You can activate the India-US DTAA by filing a W-8BEN form with your foreign broker before the dividend is credited to your account.

Why submit the W-8BEN form to the broker?

Because your foreign broker is the one who deducts the withholding tax and remits it to the IRS on your behalf. When you submit the W-8BEN form, you inform the broker:

• Your tax residency and the specific article in the treaty (Article 10 for dividend income),

• The rate you claim (25%), and

• Your Indian PAN number is the Foreign Tax Identifying Number (FTIN).

The FTIN helps the IRS track all your cross-border income and support the Foreign Account Tax Compliance Act (FATCA).

Failure to file a valid W-8BEN will result in the maximum 30% withholding tax on your dividend income. If you want to recover the excess 5%, you may have to file a non-resident tax return with the US IRS, subject to applicable requirements.

Filing W-8BEN takes a few minutes and remains valid till the end of the third calendar year from the date you sign it. So, if you sign the form on April 30, 2026, it is valid until December 31, 2029. You can renew if your residency status hasn’t changed.

Filing W-8BEN is the work half done. The next step is to inform the Income Tax Department in India.

The complexity of global equity isn't in the vesting but in its reporting. A single missed Form 67 or a stale W-8BEN can turn a 25% tax benefit into a double-taxation trap. For the global executives, tax hygiene is as critical as portfolio performance.

How Do You File Form 67 to Claim the Foreign Tax Credit (FTC)?

As an Indian resident, you will have to disclose your foreign assets, including the vested RSUs and any foreign dividend income, under the Schedule FA (Foreign Assets) of your Income Tax Return (ITR).

As per Income Tax rules 128(9), you can claim Foreign Tax Credit by filing Form 67 on or before the end of the relevant Assessment Year (AY). This extended timeline applies whether you are filing your original ITR under Section 139(1) or a belated return under Section 139(4). You can file the form through the e-Filing portal.

While it is best practice to file early to ensure smooth processing, a delay in submitting Form 67 is legally viewed as a procedural lapse rather than a fatal error. Multiple judicial precedents, including rulings from the Madras High Court and various Income Tax Appellate Tribunal (ITAT) benches, have firmly established that a valid FTC claim cannot be automatically denied purely due to a late filing.

Real-World Example: Calculating the Exact Foreign Tax Credit

Let’s understand the Foreign Tax Credit with the help of an example.

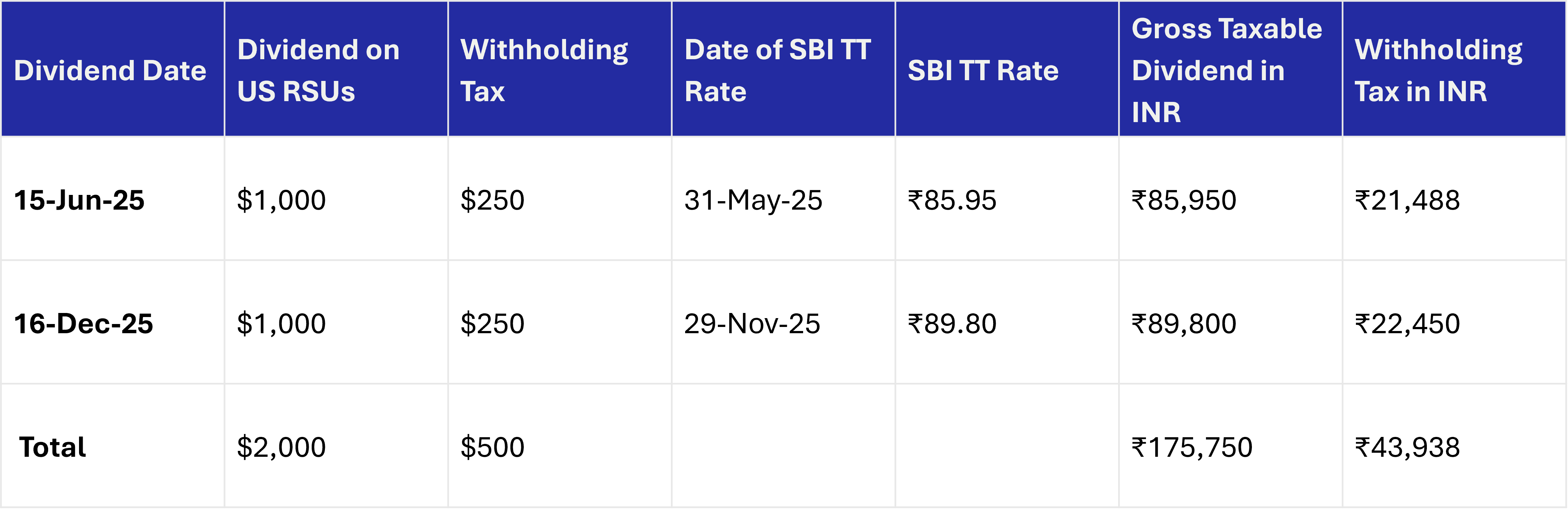

Anita is a tech employee who receives a $1,000 dividend on her vested RSUs in two instances on June 15 and December 16, 2025. She filed Form W-8BEN with her foreign brokerage in April 2025, so the broker withholds 25% ($250) on every dividend before crediting it. Since Anita is an Indian resident, she submits Form 67 and is now preparing to file her ITR in India.

First, Anita will convert her dividend income and the withholding tax into INR. She will use the SBI Telegraphic Transfer (TT) buying rate on the last day of the month preceding the month in which the dividend is paid. For the June 15, 2025, dividend, she will use the SBI TT rate of May 31, 2025.

Next, she will calculate the tax liability on the dividend income in India in INR. The $2,000 dividend, when converted into INR, came at ₹1,75,750. As she falls under 30% tax bracket plus 4% cess, her tax liability in India is ₹54,834.

In the final step, she will deduct the FTC of ₹43,938, which her broker has already paid to the US IRS on her behalf. (Since she filed Form 67 beforehand, she can claim this credit).

The FTC eliminated double taxation of the same dividend income, and Anita only has to pay the remaining ₹10,896 in tax to the Indian government.

Does the DTAA Protect Capital Gains When You Sell the RSUs?

You can claim FTC under the DTAA for dividend income, interest earned, and any other global income that falls under the “Income from Other Sources” category. However, capital gains are subject to different cross-border rules.

Generally, capital gains are taxed based on residency. If you are an Indian resident holding US shares, the US does not levy capital gains tax on non-resident aliens.

The capital gain is taxed in India based on your holding period (the difference between the vesting date and the sale date).

• 12.5% Long-Term Capital Gains for holding period above 24 months

• Short-Term Capital Gains rate as per the slab rate for holding period below 24 months

The DTAA mechanism for a capital gains FTC is rarely triggered for US equities because the US does not tax the sale.

Frequently Asked Questions (FAQs)

Can I carry forward an unutilized Foreign Tax Credit to the next financial year?

No, you cannot carry forward unabsorbed FTC; the credit must be utilized in the same financial year that the corresponding foreign income is offered to tax in India.

What happens if I miss the Form 67 deadline? ,

Failing to file Form 67 before the end of the relevant assessment year results in a denial of the Foreign Tax Credit, forcing you to pay the full Indian tax liability on the foreign income.

Do I need a Chartered Accountant certificate to file Form 67?

No, obtaining a formal CA certificate is not required to submit Form 67 on the income tax portal.

Are stock splits taxed under the DTAA agreements?

No, a stock split is a corporate action that multiplies your share count while dividing the cost basis, and it does not trigger a taxable event or DTAA applicability in either jurisdiction.

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

How to Evaluate a PMS Fund Manager: 10 Due Diligence Questio...

Ionic Wealth Tax Team on 3 Aug 2026

Selecting a PMS manager demands scrutiny beyond trailing returns—covering active share, style drift, skin in the game, capacity limits, and tax-adjusted alpha. With SEBI's proposed MF-PMS...

BOJ Holds Rates At 1.0%, Future Policy Tightening Likely

Ionic Wealth Macro Desk on 3 Aug 2026

BOJ held rates at 1.0% (8:1 vote) while upgrading growth forecasts and flagging inflation above 2% in H2 FY26. Persistent yen weakness, not inflation, remains the stronger catalyst for fu...

Post-Vesting Holding Period: Tax Impact of Holding vs Sellin...

Ionic Wealth Tax Team on 31 Jul 2026

Holding foreign RSUs past vesting means navigating FIFO-based capital gains, Budget 2024's flat 12.5% LTCG rate, and DRIP-fractured holding periods. Executives must also track OPI/FEMA di...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved