Beyond the Hyperscalers: The Rise of the Neo-Cloud GPU Giants

$23B -> $180B: Neo-Clouds are taking over from the Big Tech hyperscalers

The global cloud market is undergoing a seismic decoupling. While traditional "Big Tech" clouds offer general-purpose compute, a new breed of Neo-Clouds—specialized, AI-native infrastructure providers—is exploding. This segment is projected to grow from ~$23B in 2025 to ~$180B by 2030, representing a massive 45% CAGR. Unlike the "training spikes" of 2024, the 2026 market is defined by persistent inference workloads, which now account for roughly 80% of all AI compute demand.

Key Component & Infrastructure Opportunities:

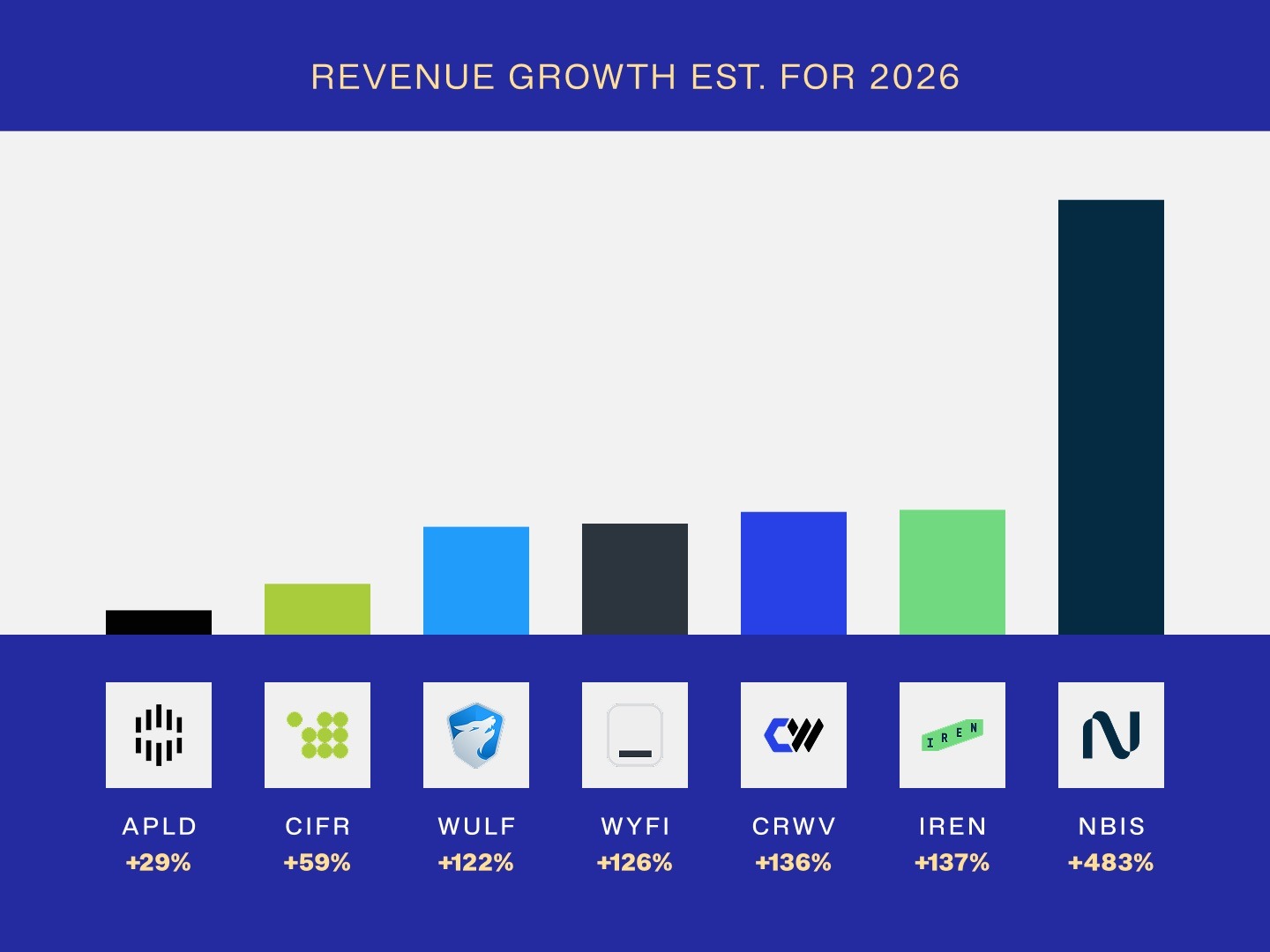

Specialized Compute & Orchestration: Neo-clouds like Nebius ($NBIS) and CoreWeave ($CRWV) are bypassing legacy virtualization. By using proprietary orchestration software, they claim to run GPU workloads at 60% lower cost than legacy clouds. This drives massive demand for Nvidia’s Blackwell and Rubin architectures.

The Power-to-Compute Pivot: Companies like Iris Energy ($IREN) and TeraWulf ($WULF) are weaponizing their energy assets. By converting BTC mining sites into AI data centers, they leverage 3GW+ of secured power. This creates a "brownfield" advantage, reducing capital intensity compared to building from scratch.

High-Density Interconnects: Specialized campuses, such as those run by WhiteFiber ($WYFI), are bundling owned fiber with AI-ready racks. This "Interconnect-as-a Service" model is essential as clusters scale toward 100k+ GPUs, where networking latency becomes the primary bottleneck.

Contracted Infrastructure Cash Flows: The business model is shifting toward "Take or-Pay" structures. Operators like Applied Digital ($APLD) are securing multi-billion dollar, long-term lease agreements (e.g., $11B+ at Polaris Forge), providing unprecedented visibility into 2027 and 2028 revenue.

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

How to Evaluate a PMS Fund Manager: 10 Due Diligence Questio...

Ionic Wealth Tax Team on 3 Aug 2026

Selecting a PMS manager demands scrutiny beyond trailing returns—covering active share, style drift, skin in the game, capacity limits, and tax-adjusted alpha. With SEBI's proposed MF-PMS...

BOJ Holds Rates At 1.0%, Future Policy Tightening Likely

Ionic Wealth Macro Desk on 3 Aug 2026

BOJ held rates at 1.0% (8:1 vote) while upgrading growth forecasts and flagging inflation above 2% in H2 FY26. Persistent yen weakness, not inflation, remains the stronger catalyst for fu...

Post-Vesting Holding Period: Tax Impact of Holding vs Sellin...

Ionic Wealth Tax Team on 31 Jul 2026

Holding foreign RSUs past vesting means navigating FIFO-based capital gains, Budget 2024's flat 12.5% LTCG rate, and DRIP-fractured holding periods. Executives must also track OPI/FEMA di...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved