Are taxes quietly eating your ESOP gains?

ESOP gains are subject to a complex, multi-stage taxation process that can significantly reduce net returns and create unexpected liquidity challenges.

Key Takeaways

- ESOP benefits are taxed twice: first as a "perquisite" income when exercised (based on the difference between fair market value and exercise price), and then as capital gains upon subsequent sale.

- The perquisite tax demands an upfront payment on paper profits, requiring employees to have liquid cash even before monetizing their shares, which is particularly risky for unlisted companies.

- Proper planning is essential to navigate vesting periods, understand the tax implications of both listed and unlisted ESOPs, and ensure optimal financial outcomes.

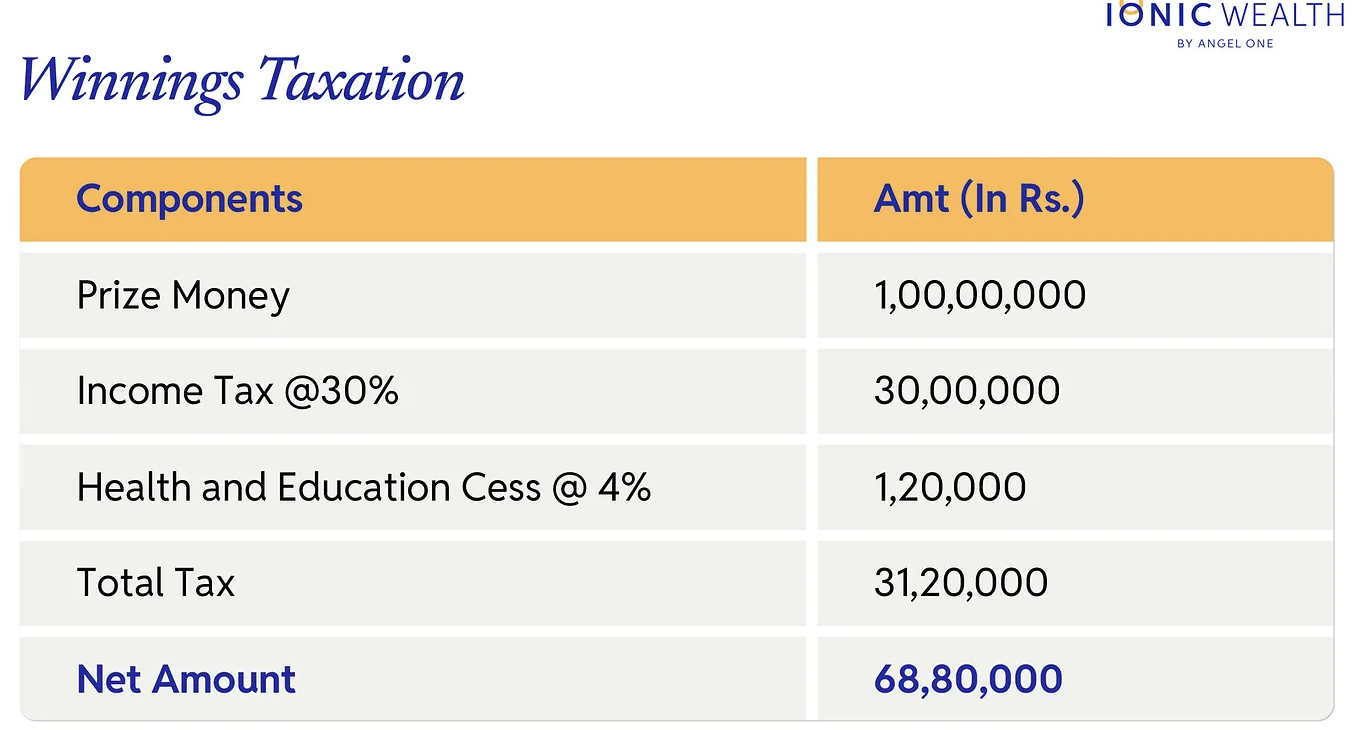

You participate in the ‘Kaun Banega Crorepati’ show and reach the final stage. One question away from hitting that one crore jackpot. Just imagine all the things you could do with one crore rupees.

In reality, the prize money comes with a Rs 32 lakh tax bill. You receive only Rs 68 lakhs after paying tax, far behind one crore. What a bummer. Right?

Something similar happens with employee stock ownership plans (ESOPs).

For starters, ESOPs gives employees the right to buy the shares of their employer at an exercise price, which is typically lower than the market price. They are offered as an added incentive to salaries.

If the shares perform well in the future, you could theoretically make tons of money. Remember, the company has given you a word that you can get the shares at a pre-determined exercise price after you meet certain pre-conditions.

If the shares are trading higher than the exercise price at future, you can exercise your rights and sell the same shares to others at a higher price and pocket the difference.

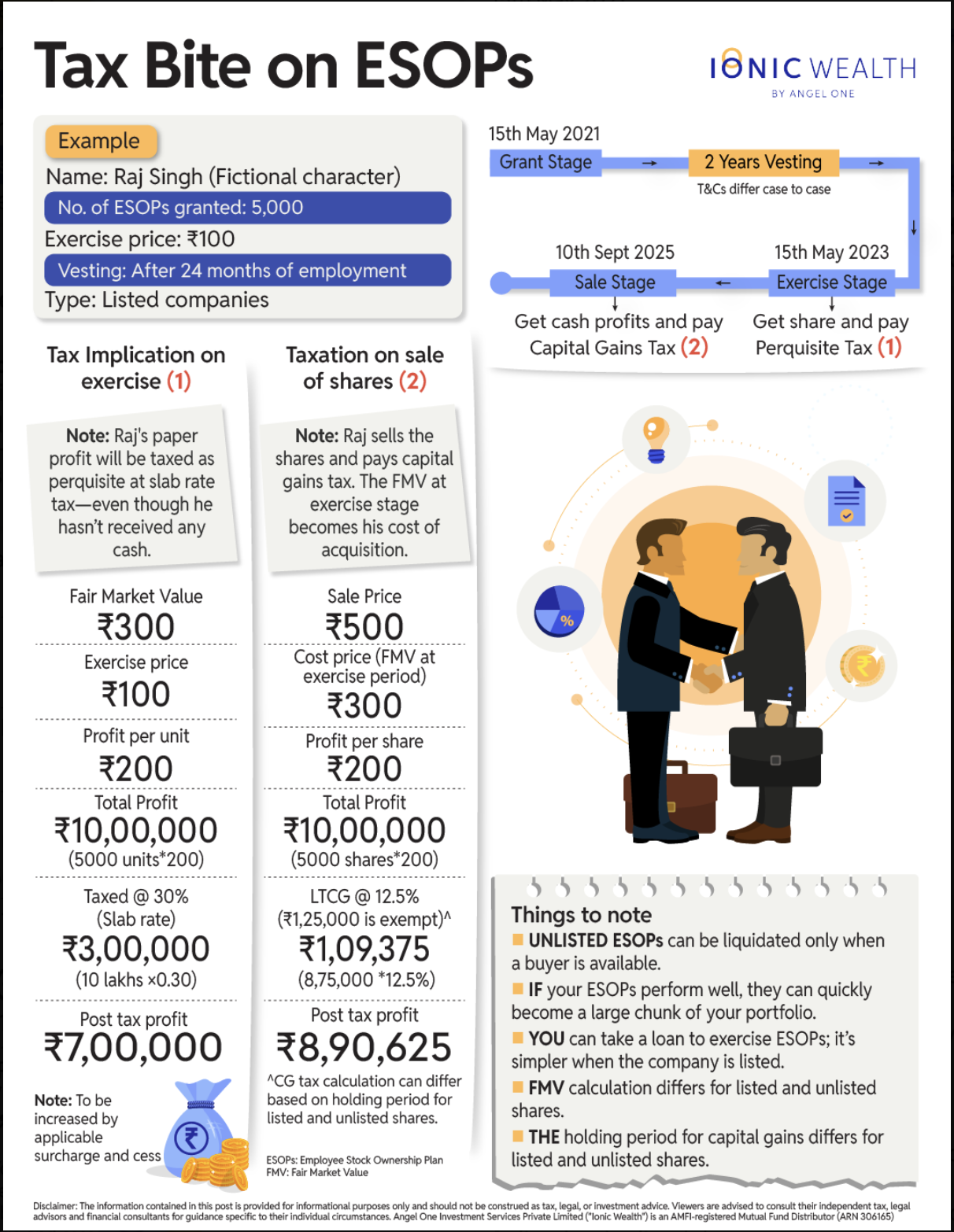

Example

Let’s say Raj was offered 5,000 shares in ESOPs at an exercise price of Rs 100, a slight discount to the current share price of Rs 120. However, he can’t just go ahead and exercise the ESOPs immediately.

There was a catch.

His employer told him that he had to work for at least 24 months to be able to exercise that option. This is called the ‘vesting period’.

It’s a win-win situation for both parties.

Raj can hypothetically make a lot of money if the startup becomes the next big thing. Meanwhile, the company gets to keep employees like Raj within their budget by offering the ESOPs.

Of course, there is a flipside.

If the fair value of the share falls below the exercise price during the exercise window, the stock option is basically worthless. Both parties lose.

But let’s assume things turned out well for Raj. After 24 months, the fair market value (FMV) of the share becomes Rs 300.

He can now tell his employer to give him 5,000 shares at Rs 100 and pocket the difference. For 5,000 shares, it means paying Rs 5 lakh to the employer and getting shares worth Rs 15 lakh.

Simple. Right? This is where taxes come to bite.

The Tax Effect

Firstly, Raj needs to put up an upfront amount if he wants to exercise those ESOPs. While five lakh seems reasonable in our example, employees sometimes have much larger ESOPs. Many like Raj might not have that much liquid cash to exercise the ESOPs.

Second and more importantly, the difference between the exercise price and the fair value of the shares at time of exercise is taxed as a perquisite using the applicable slab rate.

In our example, Raj paid Rs 5 lakh and got shares worth Rs 15 lakh. Even though he has not sold any of those shares, the government wants Raj to pay upfront tax at slab rate on the Rs 10 lakh paper profit.

It’s not the ideal scenario. If Raj falls under the 30% tax slab, he will have to pay Rs 3 lakh as tax to the government over and above the Rs 5 lakh exercise price. It will also include additional surcharge and cess.

And if the company is unlisted, you don’t really know for sure if Raj will be able to sell his shares in the unlisted market. Not the best situation to be in :)

Now, let’s say Raj paid the perquisite tax and now has the shares in his demat. And guess what? He also found a buyer for it. While this is good, he still needs to pay another tax in the form of capital gains before the money hits his bank account.

For instance, let’s say the share price is now trading at Rs 500 and the startup also got listed in the stock exchange and he was able to easily sell the shares. In this case, the taxman will consider the price at which the perquisite tax was paid as the cost price and calculate the capital gains tax.

In this example, Rs 200 (Rs 500-Rs 300) is the profit on each share. On 5,000 shares, the total profit becomes Rs 10 lakh and out of which Rs 1.1 lakh needs to be paid as capital gains tax. (see infographic).

Things to keep in mind

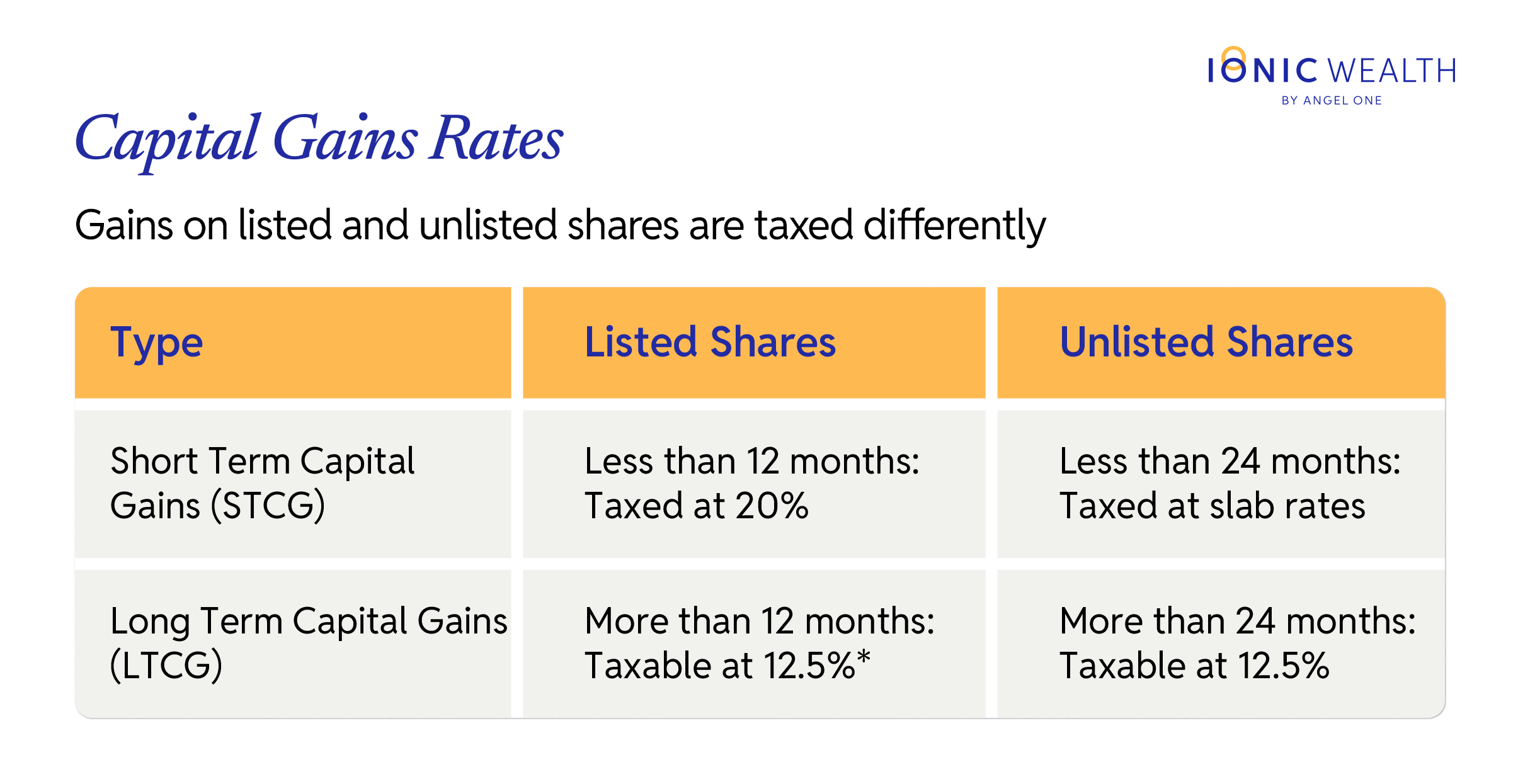

It’s important to know the details of your ESOP plan while negotiating salary package with your employer. While it is relatively easier to liquidate and sell the shares if the company is listed, it can become a challenge to find buyers if the shares are unlisted.

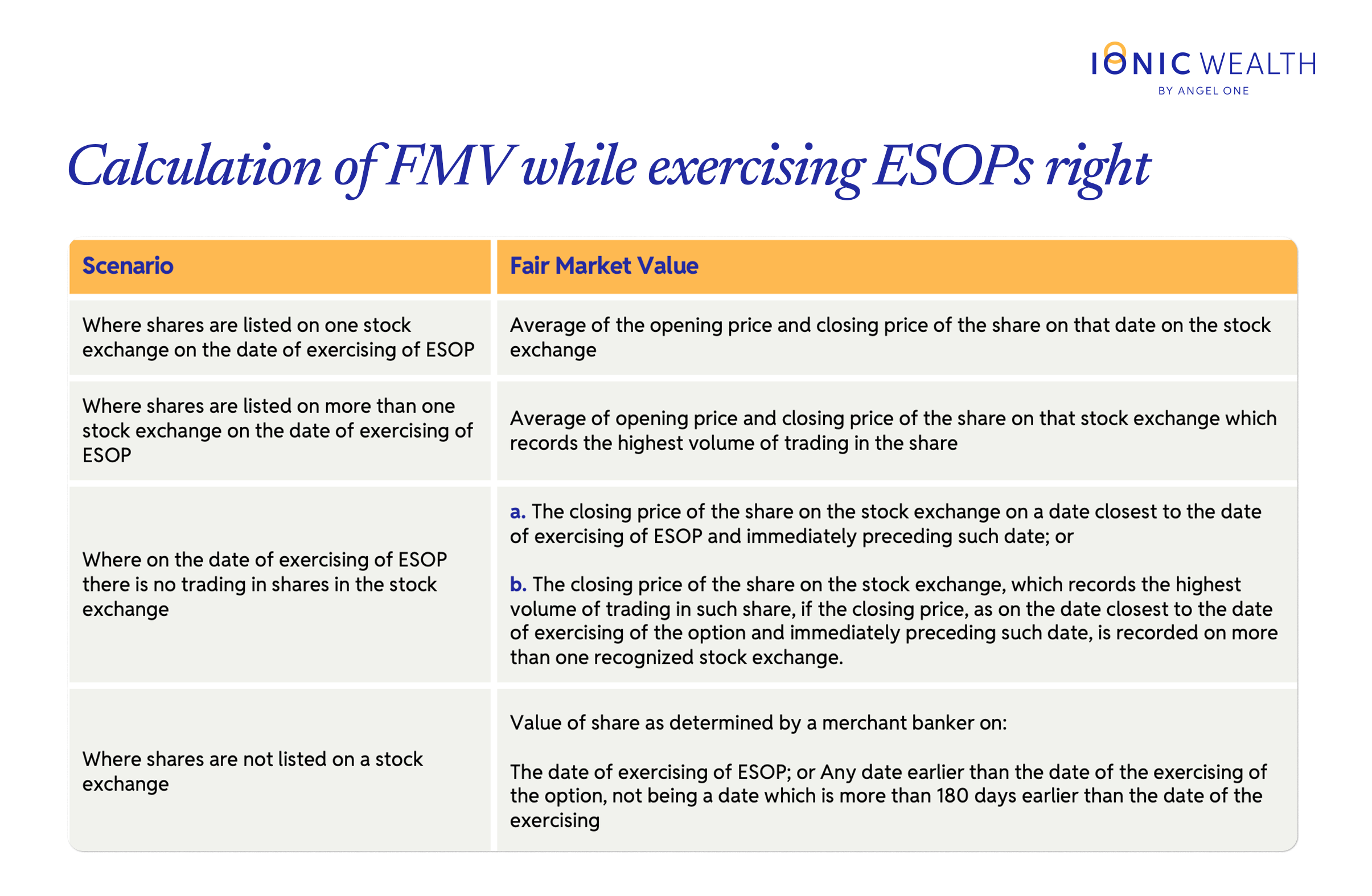

Not to mention, the calculation of the fair market value (FMV) for listed and unlisted shares vary

In many cases, the companies provide staggered vesting where a portion of the ESOPs becomes exercisable after each interval. For instance, 20% of the options may become valid after each 12 months of employment.

If you leave your job in the middle, the T&C might have a clause that restricts or reduces the time period in which you could exercise your options.

Proper planning is a must when it comes to ESOPs.

***

Heads-up. In the following weeks, we will discuss various ESOP strategies like how you can save taxes on ESOPs, what happens when you hold foreign ESOPs in your portfolio, how you can add ESOPs to your will in case you pass away and much more.

Don’t forget to subscribe to our newsletter to received updates on the latest posts.

***

With inputs from Hardik Mehta, Tax Lead at Ionic Wealth. Disclaimer

This material is for general information and guidance only. While efforts have been made to present accurate and useful information, it may not be complete or reflect the most current developments. Readers are advised to consult a qualified tax or legal advisor before relying on this information. Any examples or illustrations are purely for explanation, and any persons referenced are fictitious. We are not responsible for any decisions made based on this publication.

Angel One Investment Services Private Limited (“Ionic Wealth”) is an AMFI - Registered Mutual Fund Distributors with ARN – 306165 and a SEBI Registered Research Analyst with Reg. no. INH000020305. Mutual Funds are subject to market risk. Read all the scheme related documents carefully before investing.

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

How to Evaluate a PMS Fund Manager: 10 Due Diligence Questio...

Ionic Wealth Tax Team on 3 Aug 2026

Selecting a PMS manager demands scrutiny beyond trailing returns—covering active share, style drift, skin in the game, capacity limits, and tax-adjusted alpha. With SEBI's proposed MF-PMS...

BOJ Holds Rates At 1.0%, Future Policy Tightening Likely

Ionic Wealth Macro Desk on 3 Aug 2026

BOJ held rates at 1.0% (8:1 vote) while upgrading growth forecasts and flagging inflation above 2% in H2 FY26. Persistent yen weakness, not inflation, remains the stronger catalyst for fu...

Post-Vesting Holding Period: Tax Impact of Holding vs Sellin...

Ionic Wealth Tax Team on 31 Jul 2026

Holding foreign RSUs past vesting means navigating FIFO-based capital gains, Budget 2024's flat 12.5% LTCG rate, and DRIP-fractured holding periods. Executives must also track OPI/FEMA di...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved