Why Some Investors Are Choosing SIFs Over AIFs, PMS and MFs

Specialised Investment Funds (SIFs) are gaining traction among investors as a tax-efficient and strategically flexible alternative to traditional Mutual Funds and Category III AIFs.

Key Takeaways

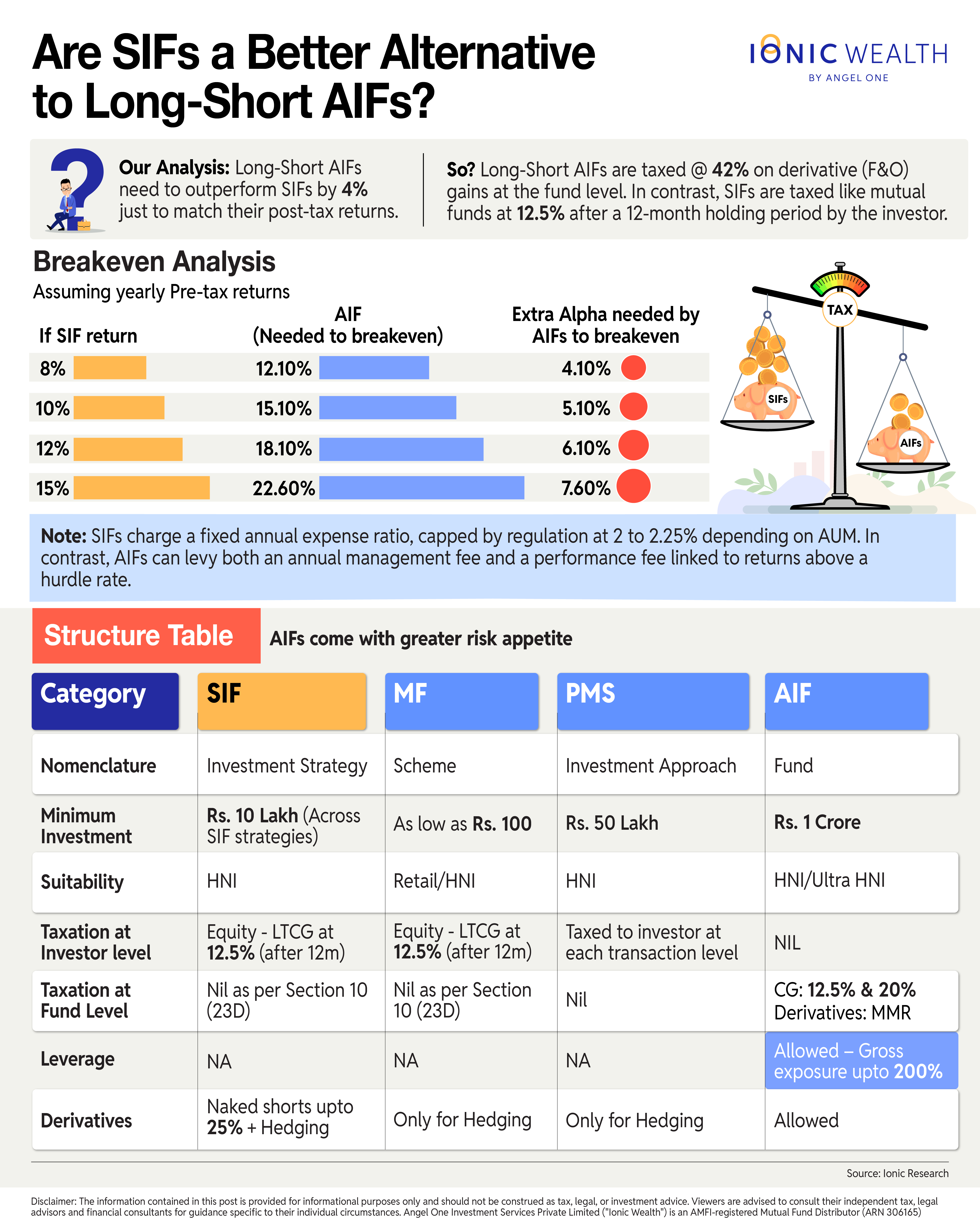

- SIFs offer a notable tax advantage over Category III AIFs; profits are taxed only at redemption, unlike AIFs' business income tax (up to 42%) on derivative trades, potentially requiring AIFs to generate 4% more alpha post-tax.

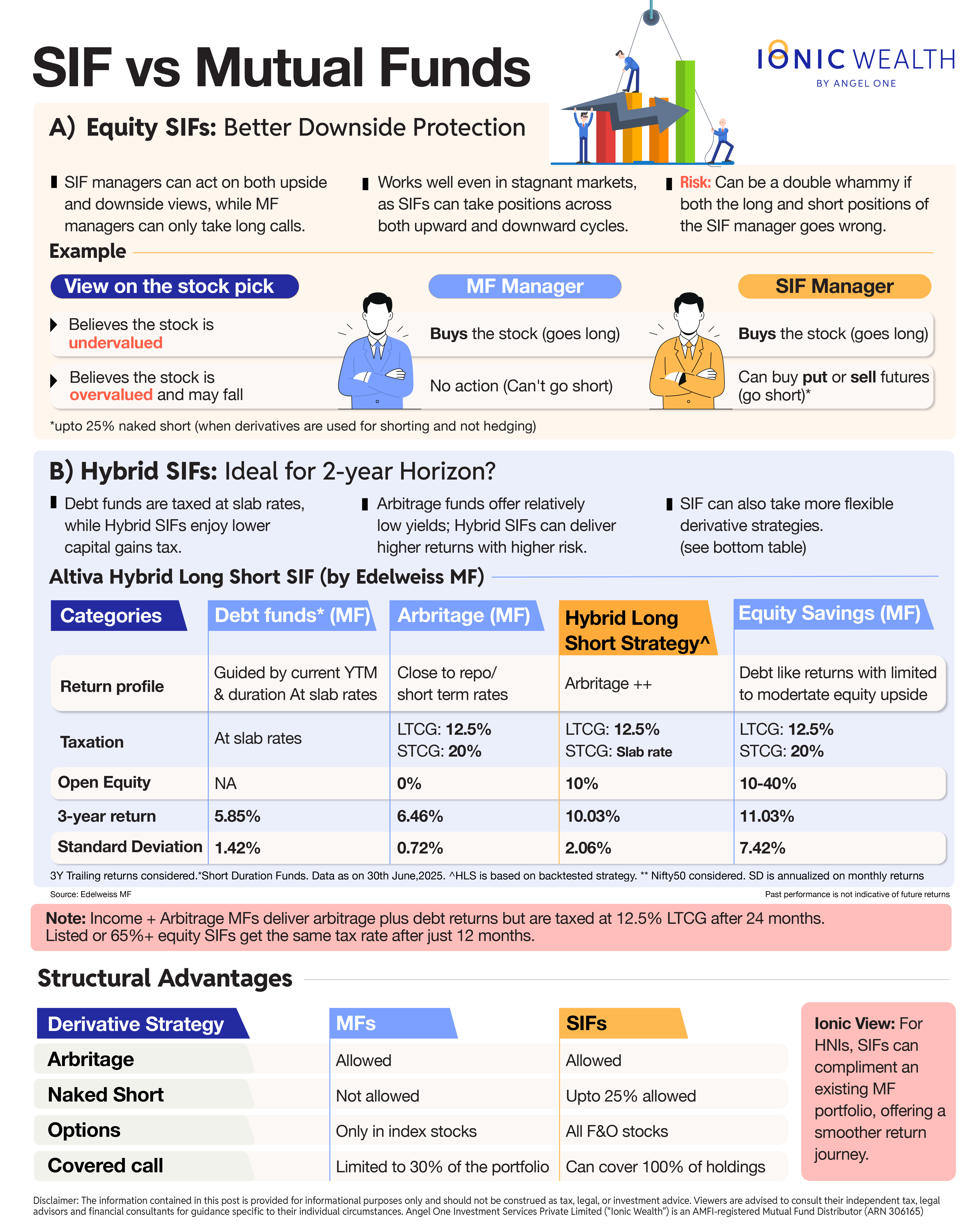

- They provide strategic diversification by allowing up to 25% naked short exposure, a feature unavailable in Mutual Funds, while maintaining clear, fixed expense ratios.

- With a lower minimum investment of Rs 10 lakh compared to AIFs/PMS, SIFs present an accessible option for HNWIs seeking expert-managed, tax-efficient strategies to complement existing portfolios.

.jpg&w=3840&q=75)

When Rahul* got a lump sum payout of a few lakh rupees, he chose to park it in Specialised Investment Funds (SIFs) instead of his usual choice, mutual funds.

Compared to mutual funds that have been around for decades, SIFs, as a concept, were only a few months old. Nevertheless, investing in them was not a difficult decision for him.

“With a full-time job, I didn’t want to get into F&O or derivatives myself. I knew what they meant but I did not want to do it myself,” said Rahul. "I decided to invest in SIFs because it’s managed by experts."

FUN FACT: The market regulator's data show that 93% of individual traders lost money in Futures and Options between FY22 and FY24.

Many high-net-worth individuals like Rahul*, who have a portfolio of at least one crore rupees, are choosing to allocate part of their portfolios to the newly launched Specialised Investment Funds.

How SIFs Stack Up Against Long-Short AIFs

Affluent Indian investors are finding a solution in SIFs that was missing in the MF, PMS and AIF space. Let us first understand how SIFs score over Category III AIFs on the taxation front.

When an AIF trades in derivatives (F&O), its profits are taxed as business income, and 42% tax is deducted by the fund on every such transaction. On the other hand, SIFs are taxed just like mutual funds when investors redeem their units. As a result, SIFs are not taxed on every transaction and are taxed at a lower rate at the time of redemption.

Due to this, purely from a tax implication perspective, our calculations show that a long-short AIF that actively uses derivatives needs to generate an alpha of around 4% to beat SIFs on a post-tax basis (assuming SIF delivers 8% CAGR pre-tax).

Data Focus: Assets managed by SIFs have more than doubled to Rs 4,892 crore in December 2025 from Rs 2,101 crore in October, as per AMFI data.

Secondly, SIF fees and expense ratios are easier to calculate compared to AIFs. AIFs are allowed to charge performance-based fees over and above a fixed annual fee. SIFs are more straightforward, with a fixed expense ratio (maximum 2–2.5% depending on the category). This gives investors more clarity on what they are paying and the post-tax and post-fee returns they are likely to earn.

Category III AIFs running long-short and absolute return strategies are likely to face competition from SIFs. These AIFs deploy various strategies that use derivatives and due to the structural tax advantage of SIFs, these AIF strategies will need to outperform SIFs by a wide margin to match their post-tax returns.

Fun fact: Minimum ticket sizes vary widely. Mutual funds can start from as low as Rs 100, while SIFs require Rs 10 lakh, PMS Rs 50 lakh and AIFs Rs 1 crore, though an AI licence can reduce the minimum for PMS, AIFs and SIFs.

How SIFs Complement Mutual Funds

Mutual funds are designed for the masses, and the regulator has placed strict restrictions on what they can and cannot do. This works well for most Indians, but HNIs may want to diversify beyond MFs and add different strategies to their portfolios.

Rahul* had full faith in his mutual fund manager’s stock-picking abilities, but the MF CIO could not take short positions within a mutual fund. So when the same manager launched an SIF, he decided to invest Rs 15 lakh initially.

SIFs can take up to 25% naked short exposure. While mutual fund schemes can use derivatives, they are allowed to do so only for hedging and cannot take naked short positions. Rahul said he is testing the waters for now and plans to invest more after tracking the performance of various SIF schemes.

Apart from the shorting feature that differentiates SIFs from traditional mutual funds, certain hybrid SIFs are positioning themselves as alternatives to pure debt mutual funds and arbitrage funds over a 2- to 3-year horizon.

Debt mutual funds are taxed at the slab rate, whereas hybrid SIFs are taxed at a lower capital gains rate. Such SIFs are taxed at 12.5% after 24 months. However, some hybrid funds are listed and hence taxed at 12.5% after 12 months.

Perspective: Arbitrage yields have also fallen lately, and many investors do not find current yields attractive.

We feel SIFs could be a good addition to an HNI's existing portfolio. Not only are SIFs more tax-efficient than Category III long-short AIFs and PMSes, but they are also available at a lower ticket size of Rs 10 lakh. SIFs can also take naked short positions that are otherwise not available in MFs. In that way, they offer the best of both worlds.

Having said this, we recommend taking the advice of a qualified professional to select the right kind of SIF scheme as per your risk appetite and goals.

*Rahul is a fictional character

Discover SIFs: Here

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

How to Evaluate a PMS Fund Manager: 10 Due Diligence Questio...

Ionic Wealth Tax Team on 3 Aug 2026

Selecting a PMS manager demands scrutiny beyond trailing returns—covering active share, style drift, skin in the game, capacity limits, and tax-adjusted alpha. With SEBI's proposed MF-PMS...

BOJ Holds Rates At 1.0%, Future Policy Tightening Likely

Ionic Wealth Macro Desk on 3 Aug 2026

BOJ held rates at 1.0% (8:1 vote) while upgrading growth forecasts and flagging inflation above 2% in H2 FY26. Persistent yen weakness, not inflation, remains the stronger catalyst for fu...

Post-Vesting Holding Period: Tax Impact of Holding vs Sellin...

Ionic Wealth Tax Team on 31 Jul 2026

Holding foreign RSUs past vesting means navigating FIFO-based capital gains, Budget 2024's flat 12.5% LTCG rate, and DRIP-fractured holding periods. Executives must also track OPI/FEMA di...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved