LRS Limit Expiring? Here's How to Invest Before March 31st

With just a few days left in the financial year, investors looking to build a global portfolio may consider using their remaining Liberalised Remittance Scheme (LRS) limits before the clock resets on 1st April.

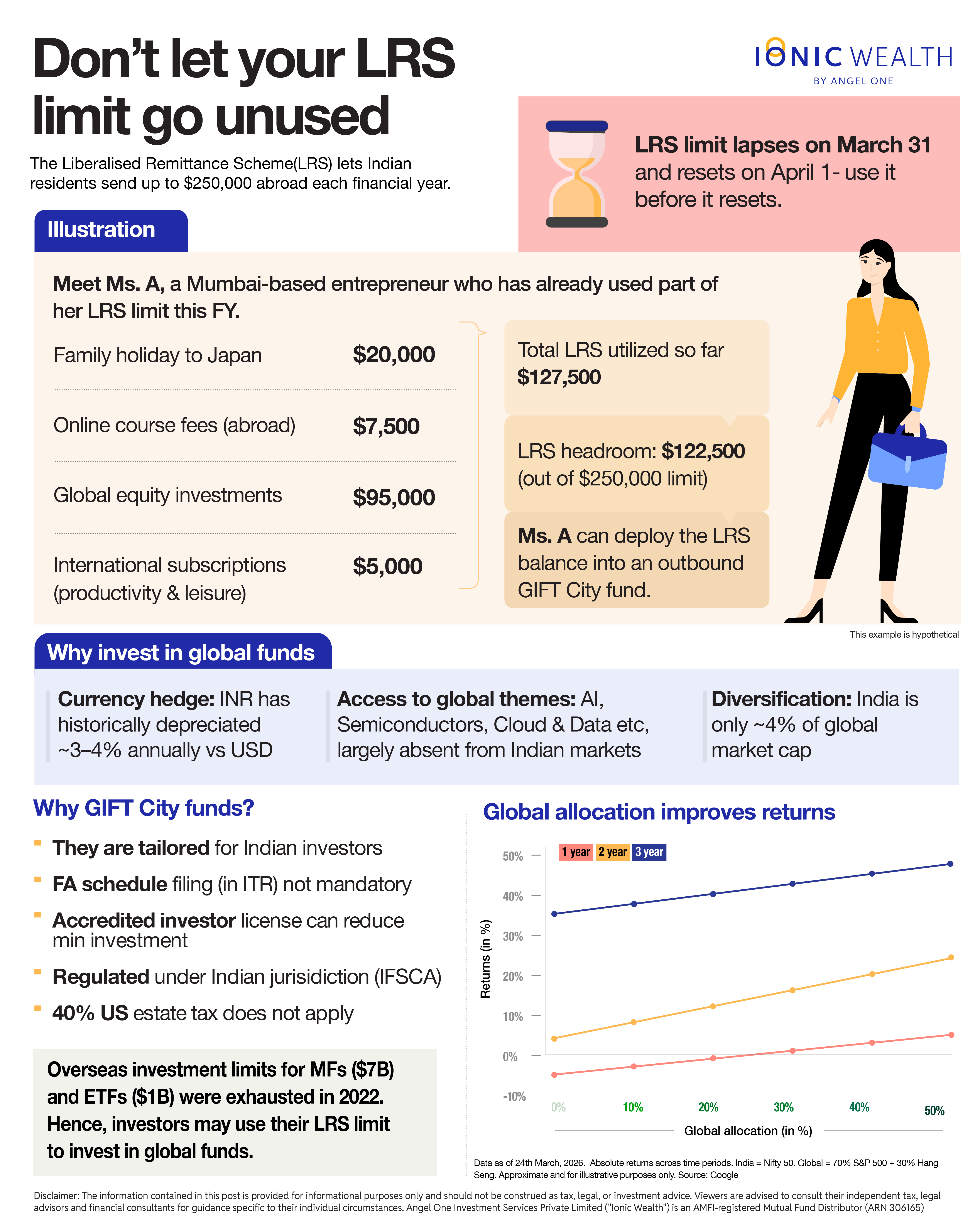

For the uninitiated, the Reserve Bank of India allows every Indian resident to send up to $250,000 abroad each year under the Liberalised Remittance Scheme.

Think of it as a yearly allowance: whatever you use is gone, and whatever you don’t use simply expires.

How Does the LRS Limit Work? A Simple Example

Meet Ms A*. She’s a Mumbai-based entrepreneur who’s had a busy year. Overseas investments, a foreign course, a family trip to Japan and whatnot. By now, she’s used up $127,500 of her $250,000 annual LRS limit.

That leaves her with $122,500 still on the table (vs $250,000 yearly LRS quota). Like a use-it-or-lose-it annual allowance.

The LRS limit resets on April 1st, and a fresh $250,000 becomes available for the new financial year.

Also Read: A Guide for Indians Investing Abroad

So, what do you do with the remaining LRS limit?

Burning through your LRS limit on a shopping spree abroad? That's one way to use it. But instead of spending just to exhaust the limit, a better approach is to invest and park it somewhere. Global funds or funds with overseas exposure are a good place to start.

For context, mutual funds were given an overall overseas investment cap of $7 billion back in 2008. By 2022, this industry-wide limit was hit, and many funds stopped accepting fresh inflows. ETFs had a sperate sub-limit of $1 billion which was also breached.

As a result, investors may look to routes like GIFT City or other global funds in different jurisdictions to invest abroad. Beyond mutual funds and ETFs, most overseas investment options require tapping into the LRS limit.

Why Invest Outside India Using Your LRS Limit

Currency risk: The rupee has historically depreciated about 3% annually against the dollar. So, your daughter’s US education gets costlier over time, even if fees stay the same in dollars. Holding dollar assets helps offset this.

Access to sectors: Many of the world’s leading sectors, such as AI, search, semiconductors, EVs, cloud, and data, are dominated by companies listed overseas. Meaningful exposure often requires investing in where these companies are listed.

Diversification: India accounts for roughly 4% of global market capitalisation. Yet, most Indian portfolios are heavily domestic, missing out on the other 96%.

Holding funds abroad: Once money is invested overseas, it can be reused without dipping into future LRS limits. For instance, if you invest via an outbound GIFT fund and later use it for US education, no fresh LRS utilisation is needed since the money is already abroad.

Ionic’s view: Why GIFT City Funds Are a Smart LRS Investment Option

Outbound GIFT funds, which invests outside India, are an interesting option if you still have LRS headroom and want global exposure. They are designed for Indian investors and regulated locally by the International Financial Services Centres Authority.

Unlike direct foreign investing through overseas brokers or funds, GIFT City retail and AIF investments do not require reporting under Schedule FA in the ITR. If you qualify for accreditation, minimum investment sizes can also come down.

Some GIFT retail outbound funds accept investments starting at $5,000. Investments above ₹10 lakh attract 10% TCS, but if you haven’t used this threshold yet, you could deploy up to ₹10 lakh before March 31st and another ₹10 lakh after, without triggering TCS. Remember, TCS is not an extra tax. It can be claimed back in your ITR or adjusted against TDS.

With the financial year drawing to a close, the window to make the most of your LRS limit is narrowing fast. Whether you're looking to build dollar reserves for future goals, gain exposure to global markets, or simply diversify beyond India's domestic equity universe, it may be worth evaluating whether global investing aligns with your financial plan and risk appetite.

GIFT City outbound funds offer a regulated and structured avenue for those seeking international exposure within a familiar regulatory framework.

That said, all investments carry risk, and global funds are subject to currency fluctuations, geopolitical factors, and market volatility in addition to standard market risks.

We recommend consulting your financial advisor or MFD before making any investment decisions. If global diversification is part of your long-term plan, reviewing your remaining LRS limit before March 31st, in consultation with your advisor, may be a timely and worthwhile exercise.

*Hypothetical example FAQs Does the LRS limit reset every year? → Yes, on April 1st.

What happens to unused LRS limit? → It expires and cannot be carried forward.

Can I invest my LRS limit in GIFT City funds? → Yes, GIFT City outbound funds are a regulated option.

Is TCS applicable on LRS investments? → Yes, above ₹10 lakh, but it can be claimed back in your ITR.

About LRS: RBI site

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

How to Evaluate a PMS Fund Manager: 10 Due Diligence Questio...

Ionic Wealth Tax Team on 3 Aug 2026

Selecting a PMS manager demands scrutiny beyond trailing returns—covering active share, style drift, skin in the game, capacity limits, and tax-adjusted alpha. With SEBI's proposed MF-PMS...

BOJ Holds Rates At 1.0%, Future Policy Tightening Likely

Ionic Wealth Macro Desk on 3 Aug 2026

BOJ held rates at 1.0% (8:1 vote) while upgrading growth forecasts and flagging inflation above 2% in H2 FY26. Persistent yen weakness, not inflation, remains the stronger catalyst for fu...

Post-Vesting Holding Period: Tax Impact of Holding vs Sellin...

Ionic Wealth Tax Team on 31 Jul 2026

Holding foreign RSUs past vesting means navigating FIFO-based capital gains, Budget 2024's flat 12.5% LTCG rate, and DRIP-fractured holding periods. Executives must also track OPI/FEMA di...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved