A Guide for Indians Investing Abroad

Back in 2008, the RBI set a $7 billion cap on the amount the entire mutual fund industry could invest overseas. At the time, it seemed more than enough.

Indian investors rarely looked beyond domestic markets, and they had good reasons to look inward. After all, the Indian stock market delivered some of the best returns from 2003 to 2018.*

However, things started to change during the Covid pandemic. Global markets produced champions in industries that barely exist in India. From then on, investors slowly began warming up to the idea of investing globally.

At that time, mutual funds were the easiest and most seamless route for Indians to invest abroad. AMCs capitalised on this by launching many NFOs for international mutual funds and ETFs.

Fast forward to 2022, and the $7 billion limit that mutual funds as an industry could invest overseas was exhausted. ETFs had a separate overall industry limit of $1 billion, which was also exhausted.

Once the industry limit was breached, domestic mutual funds investing overseas could no longer accept fresh inflows. New money can come in only if room opens up through investor redemptions or a fall in the value of overseas holdings.

That is why many international mutual funds stopped accepting new inflows. You can still buy international ETFs, but there is a catch — many of them now trade at a premium to their underlying NAV.

In today’s article, we’ll break down the different ways Indians can invest globally and examine each route from multiple vantage points.

(P.S. We won’t cover direct stock investing here.)

Way to go global: LRS

Most of you may already be familiar with the RBI’s Liberalised Remittance Scheme. The central bank allows each individual to remit up to $250,000 abroad every financial year for various purposes.

Unlike the mutual fund industry’s $7 billion overseas investment cap, which has remained unchanged since 2008, the RBI has raised the individual LRS limit over the years.

It started at $25,000 in 2004, was raised to $100,000 in 2007, and eventually to $250,000 in 2015, where it stands today.

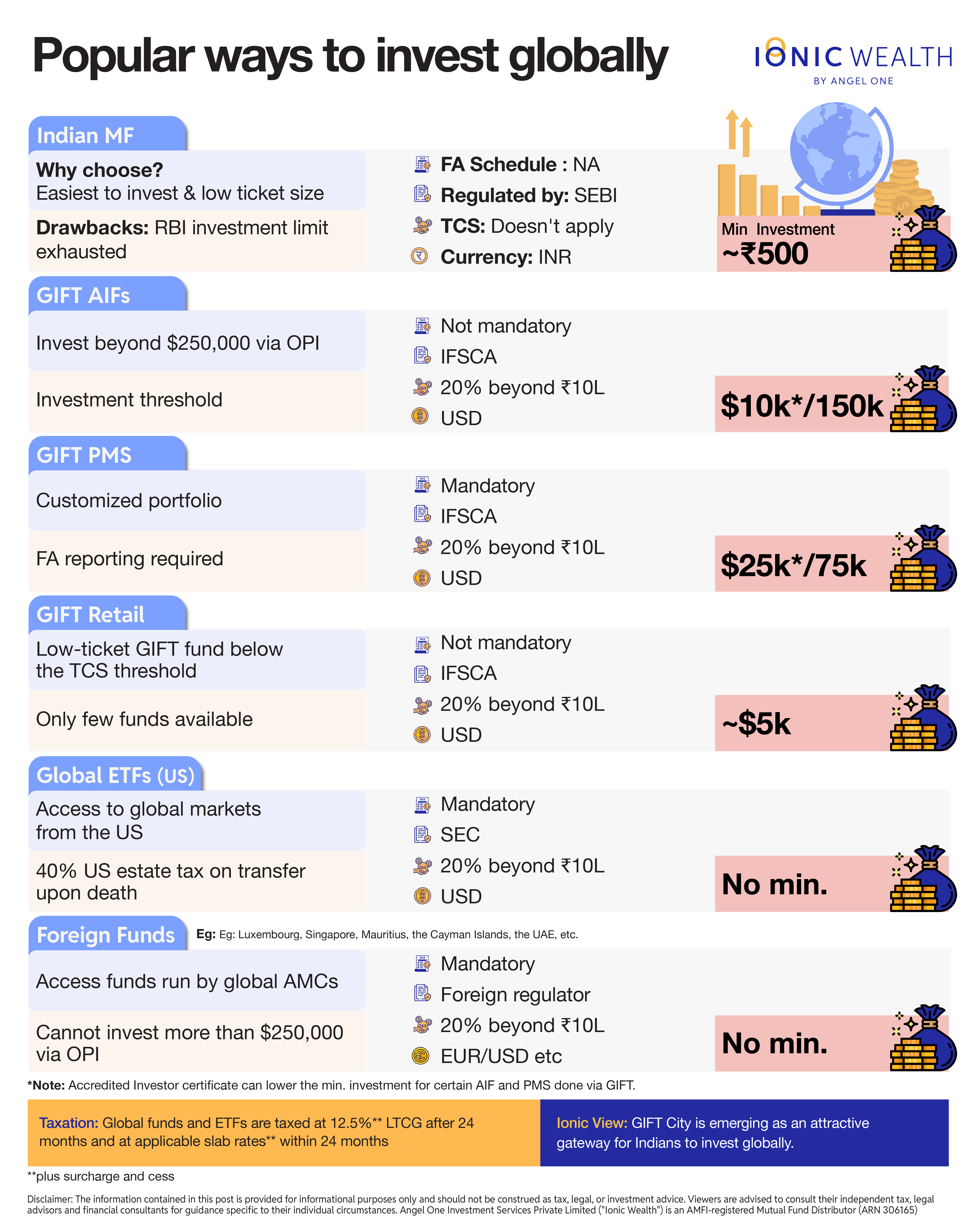

Apart from investing via domestic mutual funds, all other routes to global investment require individuals to use their LRS limits.

GIFT City: Think Global, Act Local

GIFT City was set up in 2015 to rival global financial hubs like Singapore and Dubai, with a special regulatory regime for cross-border finance.

GIFT City funds are becoming popular both as a way for Indians to invest abroad and as instruments through which NRIs and foreigners can invest in India.

While most funds channel foreign capital into India, outbound funds meant for Indians looking to invest abroad are seeing steady growth in numbers.

CAT-3 AIFs

The number of CAT-3 AIFs in GIFT City has surged to 135 as of March 2025, up from just 23 in June 2023. This includes both inbound and outbound funds.

Various funds have different strategies, and they can also diversify across different geographies as per its investment mandate.

Investors also don’t have to report their GIFT City funds in their income tax returns under Schedule Foreign Assets (FA), as GIFT City funds are domiciled in India. That said, it is advisable to still report them to be on the safer side.

For investors looking to invest more than $250,000 in a financial year, GIFT City AIFs are an interesting proposition. By routing investments through a company, LLP, or registered partnership, investors can allocate up to 50% of the entity’s net worth to a GIFT City fund via the Overseas Portfolio Investment route.

Notably, investments made through the OPI route can flow only through funds domiciled in GIFT City.

The minimum ticket size for such funds is typically $150,000. However, investors with an accredited investor certificate can start investing for as low as $10,000.

GIFT City PMS

Unlike AIFs, a portfolio management service (PMS) is not exactly a scheme but works more like an advisory service. The manager customises the portfolio based on the investor’s requirements.

The minimum ticket size is typically $75,000. Like AIFs, investors with an accredited investor certificate may be able to invest with a lower minimum.

The PMS structure also allows better utilisation of the LRS limit. When a CAT-3 AIF books profits on a foreign stock, the gains are recorded in a foreign currency. However, the tax has to be paid to Indian authorities in rupees, which may require converting some dollars back into rupees.

In a PMS structure, the underlying securities are held in the investor’s own broking account. This means that unless you buy a foreign security, you do not need to use up your LRS limit. When a foreign stock is sold and profits are booked, the investor can keep the gains in dollars while using rupees to pay the capital gains tax in India.

Note that since the underlying assets are held in the investor’s account, any foreign assets and income must be reported under Schedule FA while filing tax returns. Non-disclosure of foreign assets or income can lead to penalties under the Black Money Act.

Additionally, US-situated assets held directly by Indians can attract an estate tax of up to 40% on amounts above $60,000 in the event of the investor’s death. This risk does not arise with AIFs, since the securities are held at the fund level rather than in the investor’s individual name.

GIFT Retail Funds

The minimum ticket size of GIFT retail funds is much lower. The first two outbound retail funds from GIFT City had a minimum ticket size of $5,000.

The main unique selling proposition of such funds is their low-ticket size. If the investment amount and overall LRS remittance is lower than ₹10 lakh in a financial year, no TCS is applicable.

For context, TCS simply acts as an advance tax that can be adjusted while filing returns, although it temporarily locks up cash. TCS credit can also be used via an employer to offset against salary TDS.

However, apart from a handful of funds, there are not many retail funds to choose from at the moment. As low-ticket-size funds become more popular, there will hopefully be more launches in this category.

Non-GIFT City Routes

Apart from GIFT City, you can also open an overseas brokerage account or invest directly in funds abroad using your LRS limits.

Global ETFs (US)

If you want to invest in global markets, you don’t need to open a brokerage account in every country.

For instance, If you want to invest in Brazil, you don’t need to open a brokerage account there, you can simply open a US brokerage account. You can buy an ETF in the US that tracks the Ibovespa (BVSP), Brazil’s benchmark index.

The US is by far the most developed ETF market in the world. Bloomberg estimates suggest there were about 4,300 ETFs in the US as of August 2025. There are now more ETFs than individual stocks traded in the US.

While we have taken the US as an example, you can do the same with ETFs listed in other countries, provided you have a brokerage account that allows you to invest there.

Undertakings for Collective Investment in Transferable Securities (UCITs) is a popular fund structure based out of the EU. Many UCITs are traded on exchanges as ETFs and are therefore available at a low ticket size.

Note that if you are buying an asset situated in the US, such as an ETF, the estate tax for Indians can go up to 40% on US-situated assets above $60,000. If you have a large asset base in the US, this can become a major roadblock. This doesn’t apply to UCITs since they are domiciled outside the US.

Indian investors are also subject to a 25% withholding tax on dividends from US stocks and ETFs. So, if a stock or ETF pays a $10 dividend, $2.50 is withheld by the US. The dividend must still be reported in India and can be used to offset taxes payable in India.

Global Funds

Investors can also access global funds housed in popular jurisdictions such as Singapore, Mauritius, Ireland, Luxembourg, Dubai (DIFC), and Delaware (a state in the US), among others.

Like GIFT City funds, these global funds give investors exposure to global markets. However, the OPI route, through which investors can remit more than $250,000 in a financial year, is only available for GIFT City funds and not for funds based out of these countries.

Not all investors may have access to such funds, as distribution may be limited in India. Since these funds are not based in the US, the 40% estate tax will not apply.

Ionic View

Many investors are now actively seeking global exposure in their portfolios, and GIFT City funds are emerging as a popular choice for this purpose. Operating under the Indian regulatory framework, these funds are specifically designed for Indian investors, and they represent the only route through which investors can deploy more than $250,000 a year overseas via the Overseas Portfolio Investment (OPI) route.

Under the Liberalised Remittance Scheme (LRS), every individual gets an annual limit of $250,000 to remit abroad for various purposes. This limit resets on April 1st, so investors who haven’t fully utilized this year’s quota still have a short window to do so.

It's worth noting that LRS remittances made for investments attract a 20% Tax Collected at Source (TCS) on amounts exceeding ₹10 lakh in a financial year. Since the LRS limit resets on April 1st, investors who remit ₹10 lakh before March 31st and another ₹10 lakh after April 1st can utilize ₹20 lakh across two financial years, with each tranche staying within the TCS-free threshold.

Beyond the annual limit, GIFT City funds also help investors build a long-term dollar corpus outside India. For instance, one approach for parents planning to fund a child's overseas education could be to gradually accumulate dollars through these funds, with the proceeds potentially used toward future expenses. As with any investment decision, this is best evaluated in the context of one's overall financial plan and goals.

With inputs from Hardik Mehta, Lead-Tax at Ionic Wealth

*Past performance is not indicative of future results

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

Post-Vesting Holding Period: Tax Impact of Holding vs Sellin...

Ionic Wealth Tax Team on 31 Jul 2026

Holding foreign RSUs past vesting means navigating FIFO-based capital gains, Budget 2024's flat 12.5% LTCG rate, and DRIP-fractured holding periods. Executives must also track OPI/FEMA di...

.png&w=3840&q=75)

US Fed Keeps Rates Unchanged, Reaffirms Focus on Price Stabi...

Ionic Wealth Macro Desk on 30 Jul 2026

The FOMC held rates at 3.50–3.75% in a 9:3 vote, with three members dissenting for a hike, as inflation stayed elevated (CPI 3.5%, PCE 4.1%) despite resilient growth and a 4.2% unemployme...

.png&w=3840&q=75)

AI Momentum Accelerated Cloud Growth and Capex

Ionic Global Research on 28 Jul 2026

Alphabet raised its 2026 capital spending guidance for the second time this year, even as free cash flow turned negative for the first time since its 2004 listing. The company tapped equi...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved