RSU and ESOP Concentration Risk: Why a Single Stock Bet can Backfire

.png&w=3840&q=75)

There is a particular confidence that comes from watching your employer's stock appreciate. You hold a meaningful position via Restricted Stock Units (RSUs) or Employee Stock Ownership Plans (ESOPs), it grows into a significant share of your portfolio, and the performance justifies your conviction.

But that’s dangerous. Not the crash, but the confidence that comes during it.

When confidence becomes risk

When you see the company doing well, your belief in the product and the vision strengthens. And you start adding more. Slowly, without you noticing, it becomes 30, 40 or even 50% of your portfolio.

With ESOPs or RSUs as part of your compensation, it's even easier to slip into this position. Because equity grants don't feel like a stock bet. They feel earned. They feel like compensation, not concentration.

For starters, ESOPs give employees the right to buy company shares at a pre-determined price (exercise price) at a later date. If the share price rises above this level, the employee benefits from the upside. RSUs, on the other hand, are granted upon meeting specific milestones or vesting conditions, after which the shares are directly credited to the employee’s demat account—without any upfront payment.

But the data doesn’t care how the stock got into your portfolio and the markets aren’t always pretty.

What History Actually Shows

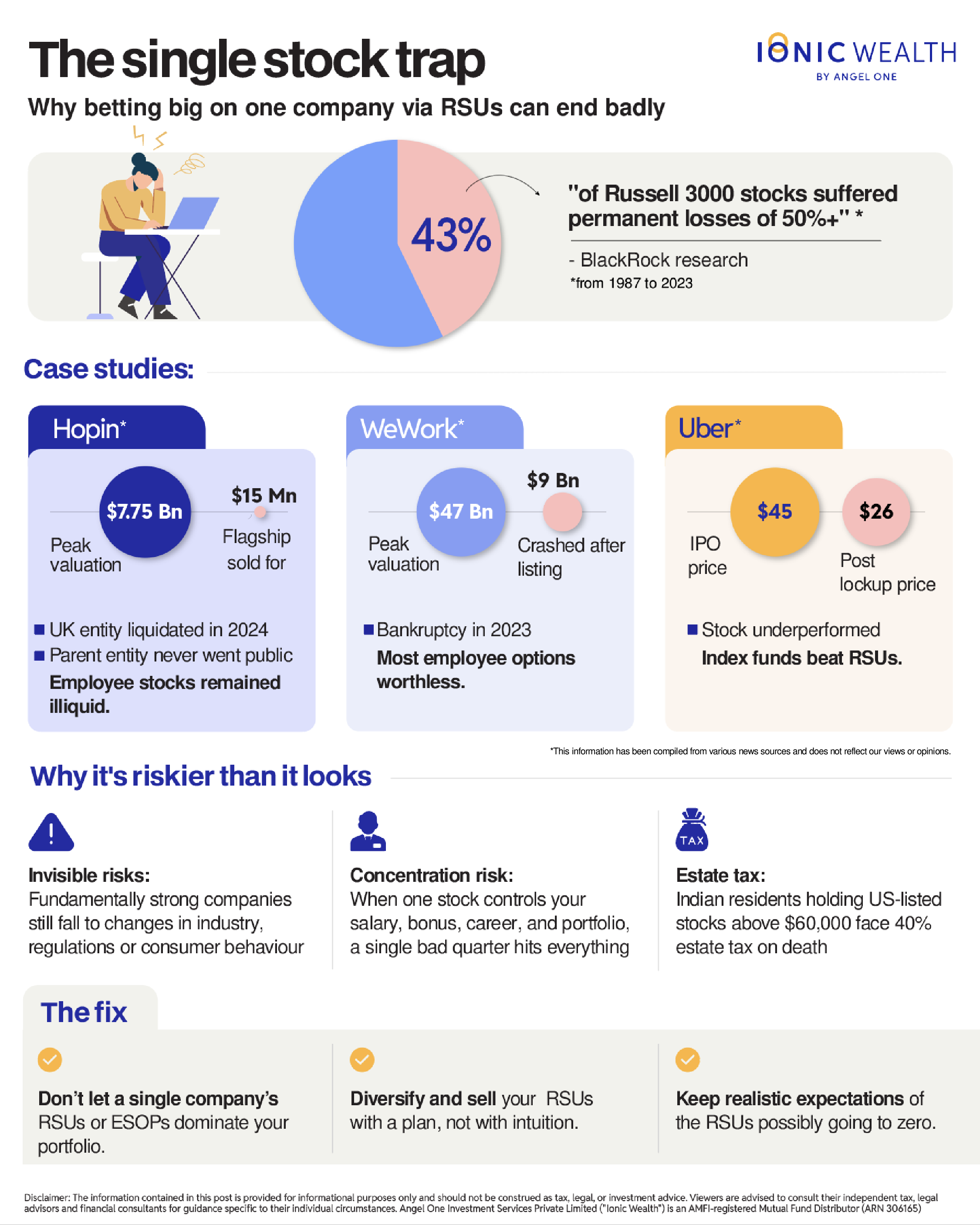

BlackRock's research, published in the Journal of Accountancy, analysed Russell 3000 stocks between 1987 and 2023. Two-thirds of individual stocks underperformed the broader index over their lifetimes. And 43% suffered a “catastrophic loss” — a decline of 50% or more from their peak, with no recovery. Not just a dip, a permanent destruction of value. Which means the lesser stocks you own, the higher is the risk of value destruction in your portfolio.

While there have been success stories of employees becoming millionaires thanks to ESOPs and RSUs, there are a lot of cases that argue against it.

Let’s look at Hopin*, a technology company that launched a virtual events platform in March 2020. At that time, Covid had shut down in-person gatherings, because of which Hopin grew at an astronomical pace. By August 2021, it had raised over $1 billion and hit a $7.75 billion valuation. Then the pandemic ended, and Hopin’s growth slowed. In August 2023, their flagship product was sold for $15 million. By February 2024, the company’s UK entity entered liquidation. The parent company restructured and never went public, so employees’ stocks stayed largely illiquid.

WeWork* - the co-working spaces startup is the more instructive case. WeWork was valued at USD 47 Bn in 2019. There are stories of WeWork employees who bought houses and took out loans to buy the company’s stock, because everyone believed that the IPO would make them rich. Then the S-1 filing went public, analysts tore it apart, and the IPO was shelved. The company eventually did go public via a merger with a Special Purpose Acquisition Company (SPAC) called BowX Acquisition Corp, but the valuation crashed to $9 billion. After a series of restructuring moves, the company filed for bankruptcy in November 2023, with a 98% drop in valuation. So while a tiny fraction of very early employees realized some modest gains, for the vast majority, WeWork equity became worthless.

And then there’s Uber* – the case that technically worked, but with a caveat. Uber went public at $45 per share in May 2019, well below the $120 billion valuation bankers had initially targeted. But by the time the six-month lockup period ended, the stock had dropped to about $26. It wasn’t exactly a wipeout, but employees who had spent years believing in their RSUs found that a simple index fund would have delivered more, with none of the lockups or tax complexity.

Why single stock exposure is riskier than most people think

The pattern across all three cases is consistent: exposure to a single stock - irrespective of the company's growth trajectory - introduces a category of risk that diversification eliminates..

Even fundamentally sound businesses are exposed to forces outside their control - regulatory changes, sectoral repricing, changes in consumer behaviour, or simply a macro environment that turns against their valuation multiple. The BlackRock data makes it clear – 43% of all Russell 3000 stocks suffered permanent catastrophic losses. These weren't all bad companies. Many were profitable, well-managed businesses that just ran into something nobody saw coming. There are things that companies themselves can’t control. Which is why over-exposure to any particular stock can become riskier than we realise.

And when when the stock you’re over-exposed to is also your employer, that risk compounds. Because your salary, your bonuses, your career growth and your investments are all tied to the performance of that one company. So if the stock drops because the company is struggling, there's a real chance that your job is at risk too. The stock, the paycheck, the future — they all move in the same direction, at the same time, for the same reasons. That's not just concentration. That's correlated concentration — and it's worse than any other kind.

Ionic View: What’s to fix

Holding your employer's stock is not the problem. The problem is holding it without a framework. Diversify well, and do it with a plan, not a feeling.

Start with a hard ceiling. Depending on your particular circumstances, identify the maximum exposure you should be taking to employer grants, for instance not more than 30% of your overall investment portfolio. Not as a target, but as a limit. If the stock price rises and your allocation crosses that threshold, that's not necessarily a win. It’s a sign to start reallocating.

Sell your RSUs on a schedule, not on conviction. The moment you start making hold or sell decisions based on how bullish you feel about the company, it stops being an investment and starts being a gamble. Identify fixed interval, quarterly or semi-annual, and liquidate a portion regardless of where the stock is trading. In public markets, this is straightforward. If you're in a private company, map out your exit windows in advance: the next buyback, any secondary sale opportunities, the eventual IPO or acquisition. Don't wait for the IPO to start thinking about this.

The difficult part about managing single-stock risk is that you might need to act against a position that’s working. Every instinct might tell you to hold, but the math will tell you to diversify.

And more often than not, the math is right.

***

A note from the Ionic team

Do you know someone who holds foreign ESOPs or RSUs? We're trying to better understand their experience — how they handle taxes, reporting, and the weight of having a large chunk of their portfolio in a single foreign stock.

If this sounds like someone in your network (or yourself), we'd appreciate you sharing this form with them.

It will take 45 seconds: Click to fill form

***

Have a look at our RSU page: Here

*This information has been compiled from various news sources and does not reflect our views or opinions.

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

Managing Concentration Risk: What to Do When Your Net Worth ...

Ionic Wealth Tax Team on 23 Jul 2026

Holding over 20% of net worth in a single stock creates outsized recovery risk — a 40% drawdown demands a 66.7% gain just to break even, and inflation plus opportunity cost widen that gap...

.png&w=3840&q=75)

ASML & TSMC: The AI Buildout is Getting Expensive

Ionic Global Research on 21 Jul 2026

ASML and TSMC both raised prices and 2026 guidance in the same week, even though neither company can fully keep up with the orders it already has. Ionic Wealth reads this as a sign the AI...

ESOP Taxation in India: Perquisite Tax, Capital Gains & Rela...

Ionic Wealth Tax Team on 20 Jul 2026

ESOP taxation in India triggers two separate events: perquisite tax at exercise (FMV minus strike price, taxed at slab rate) and capital gains tax at sale. Unlisted startup shares require...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved