Exit Planning for Founders: Maximising Value When Selling Your Business

Key Takeaways

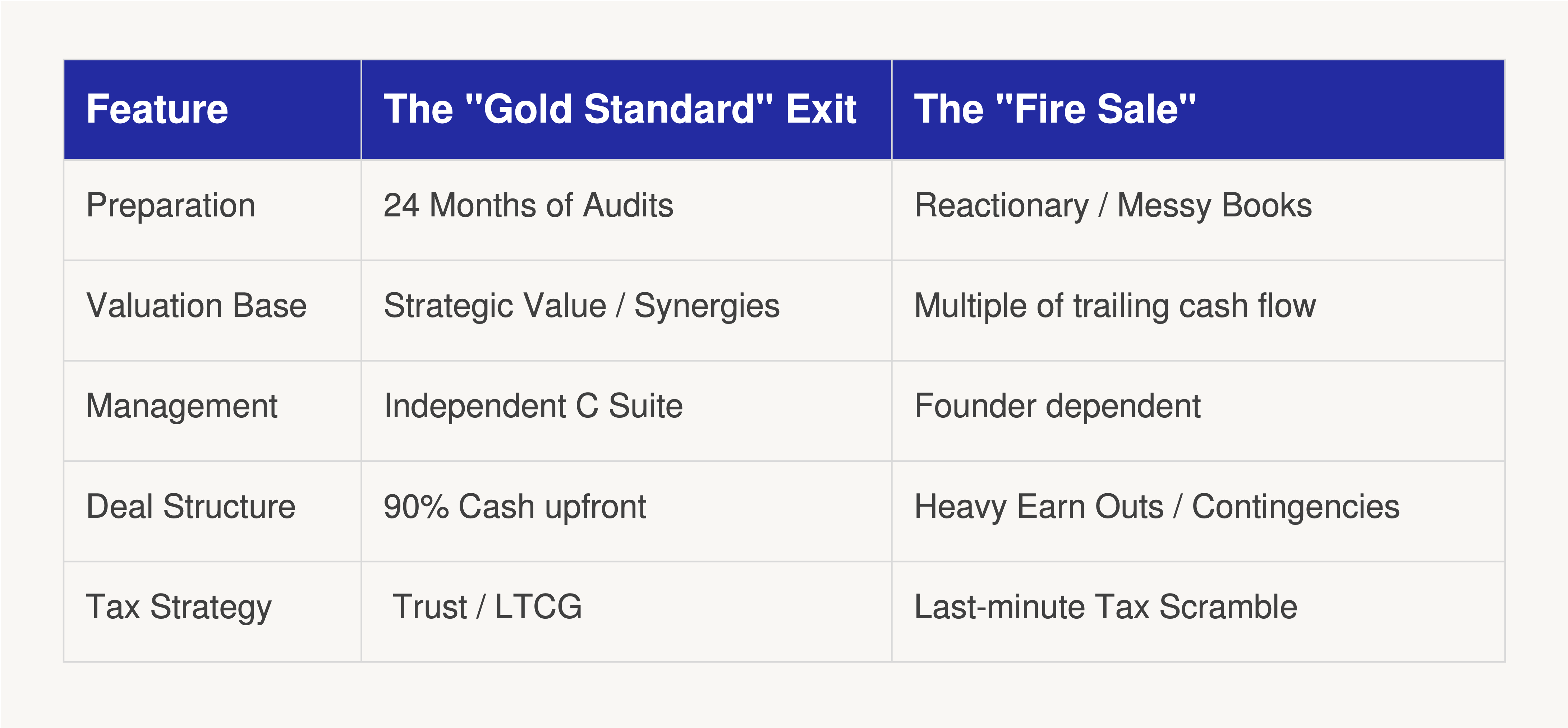

● Achieving a premium valuation requires transitioning from a founder-led operation to a liquid asset with an independent leadership team and clean, audited financials at least 18 to 24 months before an exit.

● Strategic buyers often pay higher multiples than financial buyers because they value synergies and proprietary assets over standalone cash flow, making business positioning critical to the final sale price.

● Serious deal risks, such as customer concentration and intellectual property gaps, must be resolved early to avoid "valuation haircuts" or price renegotiations during the rigorous due diligence phase.

● Maximising a post-tax windfall depends on choosing the right deal structure, such as a share sale to benefit from long-term capital gains tax rates or ensuring earn-outs are linked to revenue rather than net profit.

In the world of high-growth startups, you don't sell a business. A business gets bought.

But there is a massive valuation delta between a founder who is "ready to sell" and a company that is "built to be acquired."

The moment you pivot toward an exit, your mandate changes. You go from being the lead operator to becoming the architect of a liquid asset. In the 2026 market, the gap between a 5x and a 10x EBITDA multiple comes down to Exit Readiness.

Exit Readiness is not something you can manufacture in 30 days. It is an 18 to 24-month process that begins long before any buyer sends over a Letter of Intent.

Think of this as a liquidity event that deserves the same attention that you gave your seed round.

The playbook below is designed to help high-net-worth founders navigate valuation, tax-efficient structuring, and a rigorous due diligence process so that the final wire transfer actually reflects what you built.

Why Is Exit Readiness a 24 Month Project Rather Than a 30 Day Sprint?

Each number in your business will be stress tested by accountants, lawyers, and deal advisors. If your books are messy, your contracts are informal, or too much depends on you personally, buyers will use those factors to push the price down.

This is called a valuation haircut, which occurs far more often than founders expect.

Reducing the "Key Person" Dependency

Ask yourself honestly: What happens to your business if you take a month-long vacation with no phone?

If the answer is "things would start to fall apart," you do not have an asset. You have a job, and buyers do not pay 10x for a job.

A serious buyer wants to see a capable, independent leadership team that can run the business through a transition.

A strong Chief Operating Officer, a credible Chief Financial Officer, and a sales leader who owns client relationships are not just nice-to-haves. They are value multipliers. Building this team is one of the highest return investments you can make in the years before an exit.

The Financial "House Cleaning"

The accounting practices that reduce your tax bill often hide the true earning power of your business. Personal expenses on the books, informal vendor relationships, and inconsistent revenue recognition all raise red flags for buyers.

The shift required is from tax-optimisation accounting to investor-ready Global accounting practices. That means clean, audited financials help you hit the market value right.

For any meaningful deal, buyers will simply not proceed without this track record.

How Do I Optimise My Valuation Multiple Beyond Just EBITDA?

EBITDA tells a buyer what your business earns today. The multiple indicates how much they believe it will earn tomorrow.

That multiple is where the real negotiation happens, and it is shaped by factors well beyond your profit-and-loss statement.

Strategic vs. Financial Buyers

Not all buyers are equal. This matters enormously for your outcome.

A strategic buyer, typically a competitor or a company in an adjacent market, might pay 12x or more because of the synergies your business unlocks for them. Your customer base, your technology, or your distribution could be worth far more to them than the standalone cash flow alone.

A financial buyer, such as a Private Equity firm, is more disciplined. They are acquiring predictable cash flows and planning their own exit in five to seven years. Their offers typically cluster between 7x and 9x.

Understanding which type of buyer you are targeting changes how you position and package the business from the very beginning.

(Note: Number used are indicative generalizations; actual multiples vary significantly by sector, revenue quality, deal size, and growth profile. For more details on sector specific trends you can refer to these reports by Aventis Advisors or Kroll )

The "Moat" Metrics

In 2026, the metrics that sophisticated buyers scrutinise most go well beyond revenue and margin. The question that drives premium valuations is actually quite simple: How sticky are your customers? How difficult are you to copy?

Net Revenue Retention above 110% signals that existing customers spend more with you every year.

Proprietary data assets that competitors cannot easily replicate command meaningful premiums.

And the Cost of Replacement test, meaning how much it would cost a buyer to build what you have from scratch, often sets the floor for what your business is genuinely worth.

What Are the "Value Killers" Hidden in the Due Diligence Phase?

Due diligence is when most deals are shelved, or the price is renegotiated downward.

Intellectual Property and Legal Hygiene

One of the most common and costly surprises in due diligence involves intellectual property. Early employees who built core technology may never have signed formal IP assignment agreements.

Open-source code embedded in a proprietary product can create licensing liabilities that buyers treat as existential threats.

A thorough IP audit conducted 12 to 18 months before a sale can surface and resolve these issues well before they become deal breakers.

Customer Concentration Risk

If one client represents 30% or more of your total revenue, most serious buyers will flag it immediately, as it indicates customer concentration.

The concern is straightforward: what happens to the business if that single client leaves?

This kind of concentration often leads buyers to structure deals with escrow holdbacks or earn-out arrangements designed to protect against that downside.

Diversifying your revenue base early is one of the most direct ways to improve the eventual terms of your deal.

Share Sale vs. Asset Sale: Which Path Protects Your Post-Tax Windfall?

What you keep after tax matters more than the headline price.

This is a principle that comes up in nearly every conversation we have with founders at Ionic who are approaching a liquidity event. The structure of the deal is not a legal formality, but a financial decision worth crores.

The 12.5% LTCG Advantage in Share Sales

For most founders, a share sale is the preferred structure. When shares in a private company are held for more than 24 months, the resulting gain qualifies as a long-term capital gain, taxed at 12.5% under the rules in effect post 2024.

Compare that to the significantly higher rates that apply to short-term gains or ordinary business income, and the difference in actual money kept can be substantial.

Understanding "Slump Sales" and Asset Transfers

When a founder wants to sell a specific division or business unit rather than the entire company, the transaction is typically structured as a Slump Sale under Section 77 of the Income Tax Act, 2025. The tax treatment here differs from that of a share sale and is often less favourable.[NN2.1][NU2.2]

Understanding this distinction before structuring any deal is critical, and getting this wrong can cost you crores on a large transaction.

How Do I Structure an Earn Out Without Sacrificing My Sanity?

An earn-out is a common solution when a buyer and seller disagree on valuation. The buyer pays a base price upfront, with additional payments tied to the business hitting agreed targets after the sale closes.

Earn-outs can work well and could also become a source of prolonged frustration.

Defining "Achievable" Milestones

The most important rule: never link earn-outs to net profit.

New owners can use perfectly legal accounting decisions to reduce reported net profit, effectively making your milestone unreachable through no fault of your own.

Link earn-outs to revenue or gross margin instead. These are harder to manipulate and more directly within your control as the exiting founder.

Maintaining Operational Control

Negotiate for genuine operational autonomy during the earn-out period. If a new owner makes decisions that prevent you from hitting your targets, you need contractual protection.

A well-drafted agreement will include Reverse Clawback provisions that protect you if the buyer's own actions caused the shortfall.

The Anatomy of a Successful vs. Failed Exit

Conclusion

At Ionic, we view your exit not as the finish line, but as the starting gun for your next chapter of wealth creation. Transitioning from a successful operator to a sophisticated investor requires the same level of architectural precision you applied to building your company.

By optimizing for Exit Readiness today, through rigorous financial hygiene, leadership autonomy, and tax-efficient structuring you can ensure that the liquidity you unlock truly reflects a lifetime of ambition.

Once the wire transfer is complete, our role shifts to helping you deploy that capital into high-alpha avenues like Portfolio Management Services (PMS) and Alternative Investment Funds (AIF), ensuring your legacy continues to work as hard as you did.

Frequently Asked Questions

Should I hire an Investment Banker for a Rs 100 Crore exit?

Yes. Investment Bankers typically charge a success fee of one to three percent of the deal value. But a good banker creates competitive tension by running a structured process with multiple buyers simultaneously. That tension alone typically adds 20 to 30% to the final sale price, making the fee one of the best investments in the entire transaction.

What is a Non-Compete and how long is standard?

In India, a two- to three-year Non-Compete clause is typical. Make sure it is narrow in scope. A well-negotiated clause should still allow you to angel invest or sit on boards in sectors that do not directly compete with the business you just sold.

What is an Escrow, and why is my money sitting there?

Buyers typically hold 10 to 15% of the purchase price in an escrow account for 12 to 24 months. This covers any breaches of Representations and Warranties discovered after the sale closes. Think of it as a security deposit. You get it back once the buyer confirms there were no hidden issues beneath the surface.

Can I sell my business to my employees via an ESOP Trust?

Yes. An employee ownership trust exit is an emerging option in 2026, particularly for founders who care about preserving what they built beyond the financial outcome alone. It typically provides less immediate liquidity than a strategic sale, but it is a path worth exploring if legacy matters to you as much as the number does.

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

.png&w=3840&q=75)

US Fed Keeps Rates Unchanged, Reaffirms Focus on Price Stabi...

Ionic Wealth Macro Desk on 30 Jul 2026

The FOMC held rates at 3.50–3.75% in a 9:3 vote, with three members dissenting for a hike, as inflation stayed elevated (CPI 3.5%, PCE 4.1%) despite resilient growth and a 4.2% unemployme...

.png&w=3840&q=75)

AI Momentum Accelerated Cloud Growth and Capex

Ionic Global Research on 28 Jul 2026

Alphabet raised its 2026 capital spending guidance for the second time this year, even as free cash flow turned negative for the first time since its 2004 listing. The company tapped equi...

.png&w=3840&q=75)

ECB Rate Decision: Rates Unchanged, War Uncertainty Lingers

Ionic Wealth Macro Desk on 27 Jul 2026

The ECB held its three key rates steady in July, with the deposit rate at 2.25%, as Middle East conflict-driven energy volatility keeps inflation above the 2% target. Growth stays weak (0...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved