NRI Mutual Fund Taxation: How the DTAA Can Legally Eliminate Your Capital Gains Tax

When you sell your mutual fund investments above their cost price, you have to part with a portion of your profits in the form of capital gains tax.

That pinch in your pocket hurts! It’s like getting the keys to your first home, only to realize that you have to cough up a significant amount in brokerage fees.

But there’s a catch. Non-resident Indians (NRIs) from countries like the United Arab Emirates, Mauritius, and Singapore, among other eligible nations, can avoid this capital gains tax.

Many non-residents don’t even know this option exists, let alone how powerful it can be.

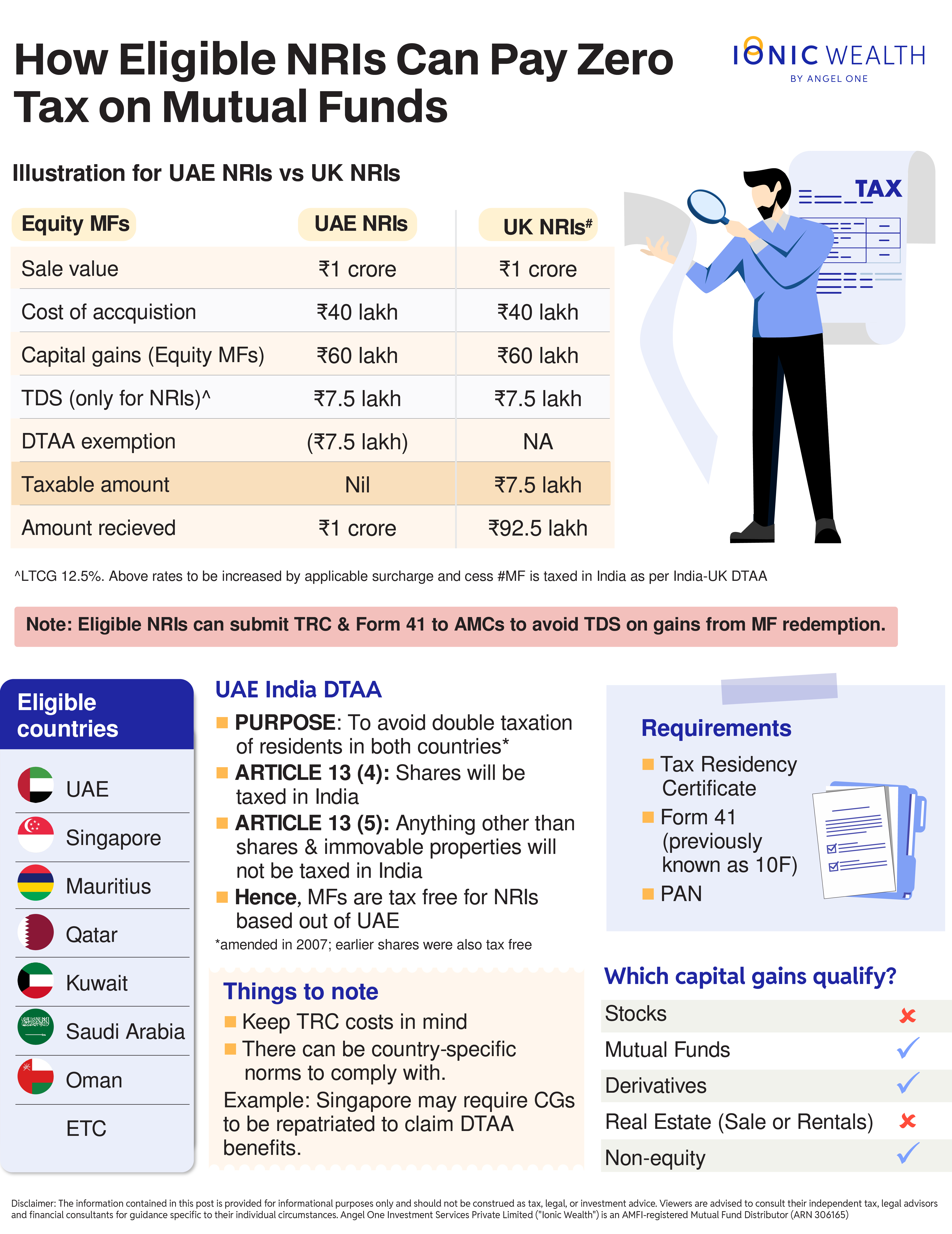

If your ₹40 lakh investment in mutual funds grows to ₹1 crore over five years, you will incur a capital gains tax of approximately ₹7.5 lakh. So, what you actually take home after tax is ₹92.5 lakh, not ₹1 crore. However, NRIs from certain countries can take home the full ₹1 crore.

How is it possible?

The Double Taxation Avoidance Agreement (DTAA) is a pact that India has signed with several countries to ensure that the same income is not taxed twice.

Without it, an NRI could face a dilemma: should the tax be paid in India or in the country of residence? DTAAs resolve this by clearly defining which country has the right to tax specific types of income.

When it comes to mutual funds, DTAAs with countries such as the UAE, Mauritius, and Singapore specify that taxation will occur in the country of residence. This creates an advantage—since these countries do not levy tax on mutual fund capital gains, such gains are effectively tax-free.

To be precise, mutual funds are not explicitly mentioned in the DTAA. For instance, Article 12(4) of the India–UAE DTAA states that gains from shares will be taxed in India. However, Article 13(5) states that income from assets other than shares and immovable property will not be taxed in India.

Since mutual funds are not classified as shares, they are taxed in the country of residence—UAE in this case. Recall that the UAE does not levy tax on personal income or capital gains.

Are there any case laws?

In the case of Saket Kanoi vs. DCIT, an NRI based in the UAE earned ₹1.34 crore by selling Indian mutual funds. However, the Assessing Officer argued that these gains should be taxed in India as shares under Article 13(4). The investor contested this, stating that mutual funds are not shares and should instead be taxed under Article 13(5), which assigns taxing rights to the UAE.

The ITAT ruled in favor of the assessee (the taxpayer). It clarified that mutual fund units are trust securities, not equity shares. Therefore, the provision allowing India to tax gains from shares did not apply. Instead, the UAE was granted the right to tax the gains—and since the UAE does not levy capital gains tax, these gains were effectively tax-free.

In another case, Anushka Sanjay Shah, an NRI based in Singapore, earned ₹1.35 crore in short-term capital gains from the sale of equity and debt mutual funds. Similar to the previous case, she claimed exemption under Article 13(5) of the India–Singapore DTAA. However, the Assessing Officer rejected her claim and treated the gains as shares under Article 13(4) of the DTAA.

The ITAT again ruled in favor of the taxpayer, stating that mutual funds are trusts and not companies under SEBI regulations. Since the term “shares” is not defined in the DTAA, and mutual fund units are not considered shares under the Companies Act, such gains cannot be taxed in India under Article 13(4).

Which countries actually benefit from this?

India has signed close to a hundred DTAAs with various countries. However, there is no exhaustive list of nations that enjoy mutual fund taxation benefits under these agreements, as each treaty contains specific clauses that must be examined on a case-by-case basis.

Based on our understanding, some eligible countries include the UAE, Singapore, Mauritius, Hong Kong, Qatar, Kuwait, Saudi Arabia, and Oman, among others.

We strongly recommend consulting a tax expert, as each country’s DTAA may have distinct provisions and interpretations.

For instance, Article 24(1) of the India–Singapore DTAA states that an NRI can avail tax benefits on the sale of mutual funds in India only when the proceeds are repatriated to Singapore. Since mutual fund capital gains are taxable in Singapore (and not India), the treaty requires the funds to be remitted to Singapore for taxation to apply there. That said, not all chartered accountants agree with the interpretation that repatriation is necessary for the gains to be considered tax-free.

How are capital gains from other asset classes taxed?

The DTAA provisions of certain countries that provide benefits for mutual fund gains do not extend to shares.

Investments in stocks made through Portfolio Management Services (PMS) also do not qualify for DTAA benefits, as the underlying assets are held in the investor’s own demat account and are treated as direct equity holdings. However, if a PMS invests in mutual funds as the underlying asset, eligible NRIs may still avail of DTAA benefits.

That said, gains derived from bonds and derivative instruments may also qualify for DTAA benefits, similar to mutual funds, as they can fall under comparable definitions within certain treaty provisions.

What do you need to claim DTAA benefits?

To claim DTAA benefits, an individual must satisfy two conditions. First, they must qualify as a tax resident of their home country. Second, they must establish tax residency in the foreign country by obtaining a Tax Residency Certificate (TRC).

Let’s understand this with the example of UAE-based NRIs. Among other requirements, an NRI must be physically present in the UAE for at least 183 days within a 12-month period to be eligible for a TRC from the UAE tax authorities. Additional documentation may also be required.

Form 41 (previously Form 10) must also be generated digitally through the Indian income tax portal. It is a mandatory self-declaration form that non-residents must submit to claim DTAA benefits. The form captures key information that tax authorities use for their records.

Eligible NRIs can claim DTAA benefits while filing their Income Tax Return (ITR). They need to navigate to the Schedule TR (Tax Relief) section, select the relevant article for capital gains, and provide details such as the tax paid in India, the amount of relief claimed (full, in this case), and the method of exemption. In some cases, asset management companies (AMCs) may also refrain from deducting TDS on mutual fund gains if the required documents are submitted in advance.

Ionic View: Things to note

For eligible NRIs, DTAA benefits that provide exemption on mutual fund capital gains can be a significant advantage. However, they should consult a qualified tax professional to correctly claim this relief. That said, investors should not aim to become NRIs of a particular country solely to avail of this tax benefit.

Another important factor to consider is the cost of obtaining a Tax Residency Certificate (TRC). Each country has its own procedures and associated costs, and it is crucial to understand these before pursuing the tax benefit.

Inbound GIFT City funds that invest in domestic mutual funds are also tax-free and do not attract TDS in India. This means that NRIs from countries such as the UAE, Singapore, and Mauritius can enjoy benefits similar to those available through direct mutual fund investments.

At its core, this highlights an important idea: where you live can matter as much as how you invest. For some NRIs, the DTAA can quietly become a meaningful advantage, reducing tax outgo over time. However, this is not a blanket rule—the benefit depends on fine print, proper documentation, and evolving regulations.

Used correctly, it can materially improve post-tax returns. The takeaway is simple: understand the treaty, get the paperwork right, and seek professional advice before taking action. Because in investing, it’s not just about what you earn, but what you get to keep.

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

How to Evaluate a PMS Fund Manager: 10 Due Diligence Questio...

Ionic Wealth Tax Team on 3 Aug 2026

Selecting a PMS manager demands scrutiny beyond trailing returns—covering active share, style drift, skin in the game, capacity limits, and tax-adjusted alpha. With SEBI's proposed MF-PMS...

BOJ Holds Rates At 1.0%, Future Policy Tightening Likely

Ionic Wealth Macro Desk on 3 Aug 2026

BOJ held rates at 1.0% (8:1 vote) while upgrading growth forecasts and flagging inflation above 2% in H2 FY26. Persistent yen weakness, not inflation, remains the stronger catalyst for fu...

Post-Vesting Holding Period: Tax Impact of Holding vs Sellin...

Ionic Wealth Tax Team on 31 Jul 2026

Holding foreign RSUs past vesting means navigating FIFO-based capital gains, Budget 2024's flat 12.5% LTCG rate, and DRIP-fractured holding periods. Executives must also track OPI/FEMA di...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved