How to optimise tax on gold ETFs

To optimize capital gains tax on gold ETFs, investors can strategically manage unit sales across different fund houses, leveraging cost basis to enhance investment flexibility.

Key Takeaways

- The tax department mandates the First-In-First-Out (FIFO) method for calculating capital gains on gold ETF sales, meaning older, potentially lower-cost units are considered sold first.

- By investing in gold ETFs from multiple Asset Management Companies (AMCs), investors gain the flexibility to choose which specific units to redeem, allowing for selection of higher-cost units to reduce taxable short-term gains.

- This multi-AMC strategy provides crucial flexibility for managing short-term versus long-term allocations and can be used to offset gains with losses during market corrections, especially in commodity and index ETFs.

Imagine this: You are managing a warehouse stacked with hundreds of biscuit boxes. A customer walks in asking for a few cartons. Which ones do you pull off the shelf?

The answer is straightforward. Pick those that have been lying in the warehouse for the longest time. It makes sense because packaged foods have expiry dates, so older stock should be cleared off the shelf first.

But what does this have to do with gold ETFs?

Well, the tax department follows the same first-in-first-out (FIFO) method while calculating capital gains tax on your investments.

At a time when the monthly inflow into gold ETFs surpassed that of equity mutual funds for the first time in January 2026, there isn’t a better time to understand how to make this work in your favor.

.png)

How it works

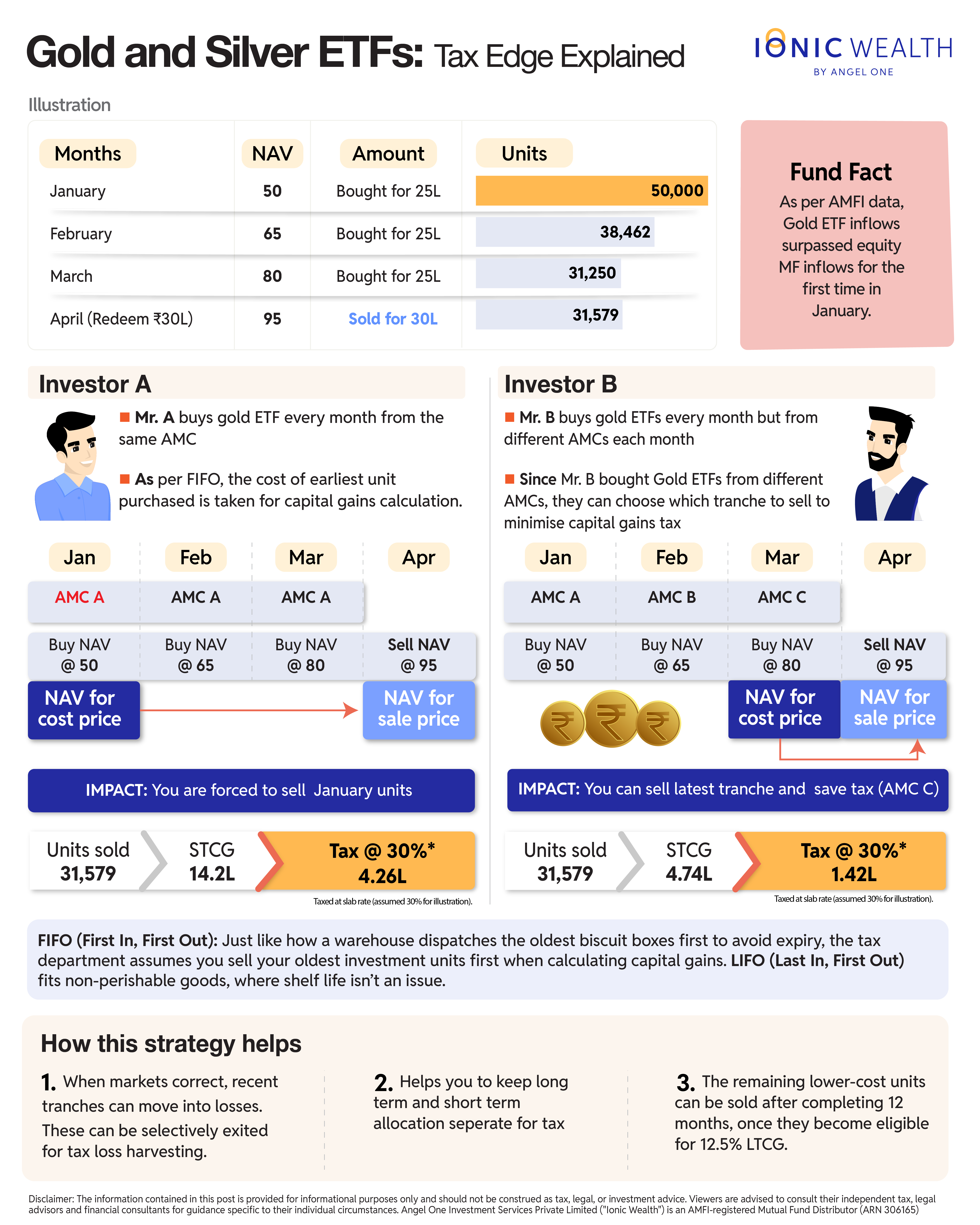

Take Mr A, who prefers buying gold ETFs rather than jewellery or bars. He buys Rs 25 lakh worth of gold ETFs every month from January to March and plans to withdraw around Rs 30 lakh in April to buy a car.

Let’s say the NAV of those gold ETFs was Rs 50 in January, Rs 65 in February, Rs 80 in March, and Rs 95 in April — the month when he sold them.

To know how many units Mr A received each month, you simply divide Rs 25 lakh by the NAV price at which those units were bought.

In January, he would have received 50,000 units; in February, 38,462 units; and in March, 31,250 units.

In April, the NAV was Rs 95, so Mr A would end up selling 31,579 units of the gold ETF at that price to receive Rs 30 lakh in hand.

But what will be the capital gains tax on those 31,579 units that were sold?

You see, Mr A bought those ETFs at Rs 50 in January, Rs 65 in February, and Rs 80 in March. While the selling NAV price is Rs 95, the units that are used for the purpose of calculating the acquisition cost will have a bearing on the capital gains tax.

Back to the biscuit warehouse example. Just like the warehouse manager, the taxman will follow the FIFO principle while calculating capital gains.

Recall the earlier example, where the first thing that comes in is also the first one to go out. In this case, the first tranche of gold ETFs bought at an NAV of Rs 50 in January will be considered as the cost price when the above ETFs are sold at an NAV of Rs 95.

The first 50,000 units sold will have an NAV cost of Rs 50, the next 38,462 units sold will have an NAV cost of Rs 65, and then 31,250 units will have an NAV cost of Rs 80.

In this case, Mr A wanted to sell gold ETFs worth Rs 30 lakh at an NAV of Rs 95, which translates to selling 31,579 units of the gold ETF. Since the taxman follows the FIFO method, those units will be considered as being sold from the lot bought at an NAV of Rs 50. This translates into capital gains of Rs 45 per unit (95–50).

In aggregate, Mr A will book Rs 14.2 lakh in short-term capital gains. Since short-term gains are taxed at the slab rate (assuming 30%), Mr A would have to pay Rs 4.26 lakh in capital gains tax.

But is there a better way to do this? After all, gold ETFs are not like biscuits that have an expiry date, and it should be possible to choose which units to sell first.

A better strategy

Let’s say Mr B did the same thing as Mr A — he bought Rs 25 lakh worth of gold ETFs for three months and sold Rs 30 lakh worth of gold ETFs in the fourth month. However, instead of buying ETFs from the same company, Mr B bought those ETFs from three separate AMCs in January, February, and March.

The only difference was that instead of buying ETFs from the same AMC, Mr B bought them from three separate AMCs across those three months.

But how does that help?

By doing this, Mr B can choose which AMC’s gold ETF he wants to redeem by looking at their NAV. Mr A did not have this option as he had purchased those gold ETFs from only one AMC.

Did you know: In the US, brokers allow investors to choose which securities they want to sell, thereby giving them more flexibility over how much tax they pay.

For instance, if Mr B chooses to sell the units bought in March, the cost price will be the Rs 80 NAV, i.e., Rs 15 profit per unit instead of Mr A’s Rs 45 profit for tax calculation. In this case, the gains will be Rs 4.74 lakh and taxed at 30% STCG, i.e., Rs 1.42 lakh.

What should you do?

You might be thinking that the units bought at a lower NAV will eventually need to be sold. Well, that’s right. However, the bucket strategy above isn’t just about short-term tax savings — it’s about giving investors flexibility.

This strategy can help investors when they are investing part of their portfolio for the long term and part for the short term in the same asset class. Also, sometimes there is a market correction when investors want to exit. If the selling price is lower than the NAV of recent purchases, those losses can be used to offset other capital gains.

This strategy works well with index funds and commodity products like gold and silver ETFs. In such products, different AMCs track the same underlying without much divergence.

That said, consult a tax expert before taking any action. Different rules apply to stocks and mutual funds.

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

How to Evaluate a PMS Fund Manager: 10 Due Diligence Questio...

Ionic Wealth Tax Team on 3 Aug 2026

Selecting a PMS manager demands scrutiny beyond trailing returns—covering active share, style drift, skin in the game, capacity limits, and tax-adjusted alpha. With SEBI's proposed MF-PMS...

BOJ Holds Rates At 1.0%, Future Policy Tightening Likely

Ionic Wealth Macro Desk on 3 Aug 2026

BOJ held rates at 1.0% (8:1 vote) while upgrading growth forecasts and flagging inflation above 2% in H2 FY26. Persistent yen weakness, not inflation, remains the stronger catalyst for fu...

Post-Vesting Holding Period: Tax Impact of Holding vs Sellin...

Ionic Wealth Tax Team on 31 Jul 2026

Holding foreign RSUs past vesting means navigating FIFO-based capital gains, Budget 2024's flat 12.5% LTCG rate, and DRIP-fractured holding periods. Executives must also track OPI/FEMA di...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved