ESOP vs RSU: Key Differences in Taxation, Vesting & Wealth Potential

Key takeaways

• ESOPs give you the option to buy shares at a fixed price, while RSUs are a direct grant of shares at no cost to the employee.

• RSU holders can usually sell shares quickly on public exchanges if the company is listed, while ESOP holders in startups often hold paper wealth that cannot be sold until an IPO or buyback.

• It is advised to treat RSUs as a salary supplement to be diversified, while treating ESOPs (unlisted shares) as a high-risk "satellite" position in your financial plan.

Introduction

The equity compensation landscape in India has changed materially over the last decade. Startup employees hold ESOPs (Employee Stock Options) worth crores in unlisted companies.

Parallelly, software engineers at Alphabet, Microsoft, and Meta vest RSUs (Restricted Stock Units) every quarter in listed foreign shares subject to a different, and often misunderstood, tax treatment.

Fundamentally, ESOPs and RSUs are issued by a company to reward an individual or employee with its equity, but they are structurally distinct rewards.

If you sit at the intersection of both worlds, or are evaluating which employer's equity offer is more valuable, the distinction matters more than most employees appreciate.

Both are taxed in two stages in India, first as salary income (perquisite) and later as capital gains, but the timing and cash flow impact differ significantly.

Note: This guide assumes a reader in the highest tax bracket (income above ₹5 crore under the new tax regime, where the effective rate including surcharge and cess is approximately 39%). Effective rates will be lower for readers in lower income brackets.

What is the Fundamental Difference Between ESOPs and RSUs?

ESOPs are the equity engine of the Indian startup ecosystem. An ESOP gives you the option (but not the obligation) to buy company shares at a pre-determined price, known as the Exercise Price or Strike Price. If the company grows, that option becomes valuable.

An RSU is a company’s commitment to give you shares at a future date, provided certain conditions are met. They are comparable to the performance bonus portion of your salary, which is credited only if you meet your employer's performance criteria. They are predominantly issued by publicly listed multinationals.

They vest over time and convert directly into shares. No purchase is required. The table below captures the structural differences at a glance.

The 'underwater' risk unique to ESOPs is real and often underappreciated. If a company's valuation falls below your strike price, your options carry no intrinsic value. RSUs, which cost nothing to acquire, retain value as long as the stock is above zero: an asymmetric protection that matters in volatile markets.

How is ESOP Taxation Calculated in India?

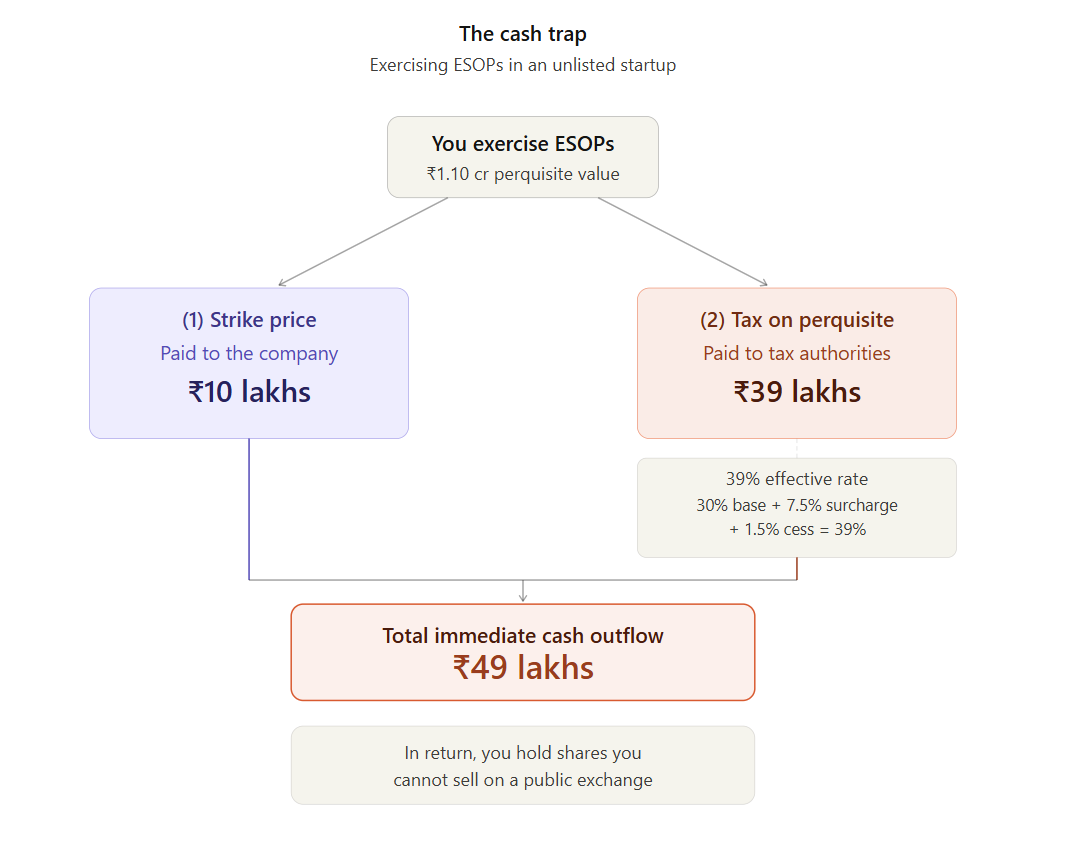

ESOP taxation in India follows a two-stage structure governed by by the Income Tax Act. A critical point (frequently misunderstood) is that the first tax event occurs at exercise, not at vesting.

Perquisite at Exercise: The taxable perquisite is calculated as: (Fair Market Value on Exercise Date – Strike Price) × Number of Shares Exercised. This amount is added to your gross salary and taxed at your applicable slab rate, with TDS deducted at source by the employer.

.png)

The numbers reveal something important: ESOPs offer leverage, but only if the stock appreciates above the strike price.

Employee A's gross asset of ₹20 lakh was acquired for ~₹13–14 lakh in real cash outlay — a respectable return, but one that required capital at risk and personal liquidity. Employee B achieved an asset of ₹12–14 lakh with no cash investment.

The ESOP scenario becomes dramatically more attractive if the stock triples or quadruples — the leverage amplifies returns.

It becomes deeply painful if the stock stagnates or falls, because the ~₹13–14 lakh is already gone, and the shares are worth less or nothing.

RSUs have a fundamentally different risk profile: hey function like a deferred cash bonus paid in stock. Even if the stock price falls before vesting, the RSUs still retain value, although your effective bonus will be smaller than initially expected. If the stock price rises before vesting, you benefit proportionally because the shares are valued at the higher FMV on the vesting date.

However, RSUs carry one underappreciated risk for top-bracket holders: the phantom tax problem. If the stock crashes after vesting, you have already paid roughly 39% perquisite tax on the higher vesting-date FMV in cash terms, even though the asset is now worth much less. A 70% post-vest decline on a ₹20 lakh vest leaves you holding shares worth ₹6 lakh after having paid ₹7.8 lakh in tax, a real economic loss that capital loss offsets only partially recover.

Shobhit Mathur, Co-Founder at Ionic Wealth says, “Equity compensation is often the largest driver of net worth for modern leaders, yet it remains the most mismanaged asset class. Getting equity is the easy part of compensation. Solving for the liquidity and tax friction that ESOPs and RSUs create is the real challenge. If you aren't planning for the tax outlay 24 months before a vest or exercise, you are going to get a shock when you have to execute it.”

What Are the Capital Gains Rates on ESOPs vs RSUs?

When you eventually sell shares acquired through either ESOPs or RSUs, the gains from the sale attract capital gains tax. The FMV on the perquisite date becomes your cost of acquisition for capital gains purposes.

Budget 2024 made material changes to these rates, effective 23 July 2024.

.png)

Note: The above rates are to be added with applicable surcharge and cess

Two reporting obligations that high-net-worth employees frequently underestimate carry serious consequences.

First, unlisted Indian shares must be explicitly disclosed in your ITR form, regardless of income level. If your total income exceeds ₹1 crore, Schedule AL (Asset and Liability) reporting also applies, requiring year-end disclosure of all assets and corresponding liabilities.

Second, and more critically for RSU holders (also applicable after exercising ESOPs) with foreign employer stock, Schedule FA (Foreign Assets) reporting is mandatory regardless of whether you sold any shares.

Failure to report foreign assets under the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015, attracts a minimum penalty of ₹10 lakh per year of non-disclosure, in addition to tax and interest.

Which is Better for Your Portfolio: ESOPs or RSUs?

The more useful question is not which instrument is better, but how each should sit within a broader portfolio. They serve structurally different functions.

RSUs are Liquid Equity. They vest on a schedule, produce a predictable post-tax cash flow in shares, and can be sold on the exchange within days.

They behave like a stock-denominated salary supplement. The rational strategy for most RSU holders is to sell vested shares regularly and redeploy into a diversified portfolio like mutual funds, bonds, real estate, or other equities, rather than accumulating concentrated positions in a single employer's stock.

The company already pays your salary; there is limited logic in having your savings concentrated in the same risk.

ESOPs are venture capital. They are illiquid, binary in nature, and should be treated as a satellite position, aka a high-risk, high-reward allocation, and not the core of a wealth plan.

The appropriate mental model is a private equity investment: underwrite the company's growth trajectory, plan for a multi-year liquidity horizon (IPO, secondary sale, or acquisition), and do not anchor your financial plan on ESOP proceeds until a liquidity event is visible.

For most employees, it also makes sense to exercise ESOPs in tranches, managing both cash outlay and tax exposure across multiple financial years where possible.

Frequently Asked Questions (FAQs)

Do I pay tax if my ESOPs vest but I don't exercise them?

No, unexercised ESOPs do not trigger any tax liability in India. Until you sign the exercise form and pay the strike price, your vested options are simply a right to buy, not a taxable asset.

What happens if my ESOP company’s valuation drops below my strike price?

Your options become "underwater," meaning it makes no financial sense to exercise them, and they will likely expire worthless. Since the cost to acquire the shares (the strike price) is higher than the shares' market value, exercising would result in an immediate financial loss.

Can I use the ₹1.25 Lakh LTCG exemption for my RSUs?

No, according to Section 112A of the IT Act 1962 or Section 198 of the IT Act 2025, the exemption applies only to Indian-listed equities for which Securities Transaction Tax (STT) is paid, not to foreign RSUs or unlisted ESOPs. Most RSUs come from foreign multinational parents (like Alphabet or Meta), which are classified as unlisted or foreign assets under Indian tax law. Consequently, your long-term capital gains will be taxed at the flat 12.5% rate without the benefit of the ₹1.25 lakh annual exemption threshold available for domestic stocks.

Is there double taxation on ESOPs?

No, not double taxation per se. But it is important to remember that there is a two staged taxation — perquisite and capital gains, but not on the same money. The system is designed to tax the "income" and "investment growth" portions separately. When you exercise, you pay tax on the gap between the strike price and the Fair Market Value (FMV). When you eventually sell, your "cost of acquisition" equals the FMV. Therefore, you only pay capital gains tax on the appreciation that happens after you already paid your perquisite tax.

Enjoying this article

Share it with the world!

WHAT'S

NEW

Collection of latest reads for you

Managing Concentration Risk: What to Do When Your Net Worth ...

Ionic Wealth Tax Team on 23 Jul 2026

Holding over 20% of net worth in a single stock creates outsized recovery risk — a 40% drawdown demands a 66.7% gain just to break even, and inflation plus opportunity cost widen that gap...

.png&w=3840&q=75)

ASML & TSMC: The AI Buildout is Getting Expensive

Ionic Global Research on 21 Jul 2026

ASML and TSMC both raised prices and 2026 guidance in the same week, even though neither company can fully keep up with the orders it already has. Ionic Wealth reads this as a sign the AI...

ESOP Taxation in India: Perquisite Tax, Capital Gains & Rela...

Ionic Wealth Tax Team on 20 Jul 2026

ESOP taxation in India triggers two separate events: perquisite tax at exercise (FMV minus strike price, taxed at slab rate) and capital gains tax at sale. Unlisted startup shares require...

Ionic Wealth Newsletter

Investment insights

made simple

Sign up for our newsletter about wealth, markets, and more.

AMFI Registered Mutual Fund Distributor

Angel One Wealth Limited (AOWL)

CIN AOWL - U66190MH2023PLC411784

Angel One Investment Services Private Limited (AOISPL)

ARN AOISPL - 306165

CIN AOISPL - U66190MH2024PTC426203

SEBI Registered Research Analyst Number- INH000020305

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Registered Office: 601, 6th Floor, Ackruti Star, Central Road, MIDC, Chakala, Andheri (East), Mumbai - 400 093

Copyright © 2025, Ionic Wealth | All rights reserved